Download

1 / 41

480 likes | 1.28k Views

Job Order and Process Costing. Chapter 17. Cost Accounting Systems. Gather information to determine the production cost per unit Help managers: set selling prices that will lead to profits compute cost of goods sold for the income statement

E N D

Job Order and Process Costing Chapter 17

Cost Accounting Systems • Gather information to determine the production cost per unit • Help managers: • set selling prices that will lead to profits • compute cost of goods sold for the income statement • compute the cost of inventory for the balance sheet • Assign these costs to the company’s product or service using: • Job order costing • Process costing

Job Order vs. Process Costing Job Order Costing Process Costing For companies that produce identical units through a series of processes Coca-Cola Surfboards Medical equipment Used by large producers of similar goods Accumulates cost of each process needed to complete the product Assigns costs to products • For manufactured batches of unique products or specialized services • Accounting firms • Music studios • Building contractors • Health-care providers • Accumulates cost per batch or job • More prevalent with service-based companies and with ERP systems

Job Order vs. Process Costing • Cost tracing is used to assign directly traceable costs • Direct materials • Direct labor • Cost allocation • Assigns indirect costs to the product • Overhead costs • Less precise technique

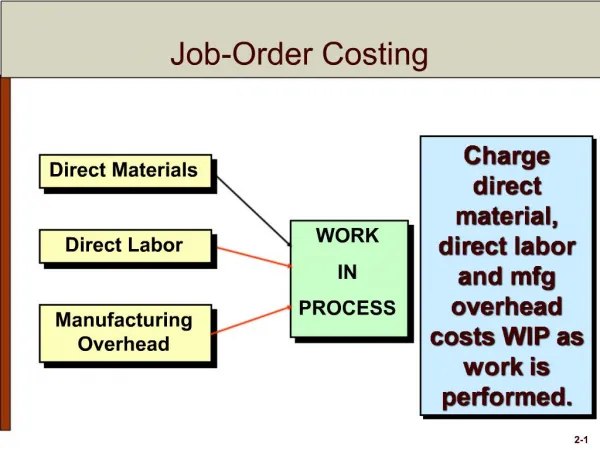

Flow of Costs(job order costing) Job 293 Direct materials Work in process Finished goods Job 293 Direct labor Materials $793 Labor 944 Overhead 472 Cost of goods sold Overhead

Purchasing Materials • Purchasing for cash or on account • Debit materials inventory • Asset account • Subsidiary ledger • Direct materials • Indirect materials Materials inventory 70,000

Using Materials • Direct materials debited to Work in process • Indirect materials debited to Manufacturing overhead • Inventory is credited for materials removed Manufacturing overhead Work in process Materials inventory

Used to request the transfer of materials to Work in process Assigns the cost of the direct material to a job (Job 16) Shows the company cost of the material requested Materials Requisition

Labor Manufacturing overhead • Debit Work in process inventory (for direct labor) • Debit Manufacturing overhead (for indirect labor) • Credit Wages payable Work in process Wages payable

Assigning Manufacturing Overhead to Jobs • Actual overhead costs are accumulated in the Manufacturing overhead account • Overhead costs are essential to production • Must be assigned to determine full cost • Two step process • Step 1 – Calculate overhead allocation rate • Step 2 – Rate is multiplied by the actual quantity of allocation base used on the job • Formula:

Predetermined Manufacturing Overhead Rate • Most accurate allocation when total overhead cost is known • A predetermined rate is calculated before the period begins using estimates • Use this rate to allocate estimated overhead cost to jobs • Rate is based upon two factors: • Total estimated manufacturing overhead costs for the period • Total estimated quantity of the manufacturing overhead allocation base

Predetermined Manufacturing Overhead Rate • Identify an allocation base • Direct labor hours (labor-intensive production) • Direct labor cost (labor-intensive production) • Machine hours (machine-intensive production)

Allocate Overhead Costs to Jobs • How to allocate overhead cost to jobs • Compute the predetermined manufacturing overhead rate • The application rate is multiplied by the actual quantity of allocation base used on the job • If the rate is based on direct labor hours • Rate is multiplied by the direct labor hours used on each job Predetermined manufacturing Actual quantity of the overhead rate (from Step 1) allocation base used by each job x

Assignment of Overhead to Jobs • Overhead is allocated to jobs in process • The journal entry includes: • At the end of the period, when a balance exists • If allocated amount is less than actual overhead—underallocated • If allocated amount is more than actual overhead—overallocated

S17-7: Accounting for overhead Teak Outdoor Furniture manufactures wood patio furniture. The company reports the following costs for June 2012: Wood . . . . . . . . . . . . . . . . . . . . . . . . $ 250,000 Nails, glue, and stain . . . . . . . . . . . . 26,000 Depreciation on saws . . . . . . . . . . . . 5,500 Indirect manufacturing labor . . . . . . 38,000 Depreciation on delivery truck . . . . . 2,300 Assembly-line workers’ wages . . . . . 57,000 1. What is the balance in the Manufacturing overhead account before overhead is applied to jobs?

S17-8: Allocating overhead Job 303 includes direct materials costs of $500 and direct labor costs of $430. Requirement 1. If the manufacturing overhead allocation rate is 80% of direct labor cost, what is the total cost assigned to Job 303?

S17-9: Comparing actual to allocated overhead Seattle Enterprises produces LCD touch screen products. The company reports the following information at December 31, 2012: 1. What is the actual manufacturing overhead of Seattle Enterprises? 2. What is the allocated manufacturing overhead? 3. Is manufacturing overhead underallocated or overallocated? By how much? $ 51,900 $53,900 Overallocated $ 2,000

Completion and Sale of FinishedGoods • To complete the process, we must: • Account for the completion and sale of finished goods • Adjust manufacturing overhead at the end of the period

Accounting for the Completion and Sale of Finished Goods • Remember the flow of costs—a job goes from: • work in process • to finished goods • to cost of goods sold • Journal entry: • Work in process to Finished goods • Finished goods to Cost of goods sold

Accounting for Finished Goods Cost Flows • T-account example of cost flows

Adjusting Manufacturing Overhead • Overhead is allocated to jobs in process • At the end of the period, when a balance exists • If allocated amount is less than actual overhead—underallocated • If allocated amount is more than actual overhead—overallocated • An adjustment is made to close out the account • Adjustment should increase (decrease) Cost of goods sold

Adjusting Manufacturing Overhead • To close Manufacturing overhead • If underallocated: • Debit Cost of goods sold • Credit Manufacturing overhead • Increases Cost of goods sold for unallocated amount • If overallocated: • Debit Manufacturing overhead • Credit Cost of goods sold • Decreases Cost of goods sold for overallocated amount

E17-18: Allocating manufacturing overhead Selected cost data for Antique Print, Co. are as follows: Estimated manufacturing overhead cost for the year . . . . . $ 115,000 Estimated direct labor cost for the year . . . . . . . . . . . . . . . 71,875 Actual manufacturing overhead cost for the year . . . . . . . . 119,000 Actual direct labor cost for the year . . . . . . . . . . . . . . . . . . 73,000 • Compute the predetermined manufacturing overhead rate per direct labor dollar. 2. Prepare the journal entry to allocate overhead cost for the year. $ 115,000 71,875 The predetermined manufacturing overhead rate per direct labor dollar is 160%.

E17-18 : Allocating manufacturing overhead Selected cost data for Antique Print, Co., are as follows: Estimated manufacturing overhead cost for the year . . . . . $ 115,000 Estimated direct labor cost for the year . . . . . . . . . . . . . . . 71,875 Actual manufacturing overhead cost for the year . . . . . . . . 119,000 Actual direct labor cost for the year . . . . . . . . . . . . . . . . . . 73,000 3. Use a T-account to determine the amount of underallocated or overallocated manufacturing overhead. 4. Prepare the journal entry to close the balance of the Manufacturing overhead account. Underallocated by $ 2,200

Process Costing • Used where large quantities of similar products are produced • Two methods: • Weighted-average * • FIFO • Costs accumulated in each manufacturing process • Company then assigns these costs to products passing through that process • Sum of the costs applied to units produced to determine costs per unit

Process Costing: Building Blocks • Two cost categories: • Direct materials • Conversion costs • Direct labor and manufacturing overhead combined • Costs incurred to convert materials into finished products • Equivalent units • Allow measurement of partially finished goods • Express production in terms of fully completed units • Materials may have different percentage completed than conversion costs

Process Costing: Building Blocks • Equivalent units • Direct materials often added at a specific pointor different points in the process • Compute separate equivalent units • Direct materials • Conversion cost

Step 1: Summarize the flow of physical units Step 2: Compute output in terms of equivalent units Step 1- Units to account for: Number of units in process plus the number of units started Step 2- Units accounted for: Number of units completed and transferred out plus number of partially completed units

Step 3: Compute Cost per Equivalent Unit • Cost of direct materials is divided by the equivalent units • For conversion costs, direct labor and overhead costs are added together and divided by the equivalent units for conversion costs

Step 4: Assign Costs • For the 40,000 units transferred out, multiply them by both the materials and labor cost per unit • Ending inventory needs to be split between materials and conversion • Materials cost uses the 10,000 equivalent units multiplied by the material unit costs • For conversion, use 2,500 equivalent units multiplied by $1.60

Journal Entries • Journal entries to record July costs placed into production • The entry to transfer the cost of the 40,000 completed puzzles

Work in Process: Dept. 1 Account • This costing system continues for each remaining department • Total cost from previous department is transferred to the next department • Process continues