Download

1 / 10

290 likes | 1.17k Views

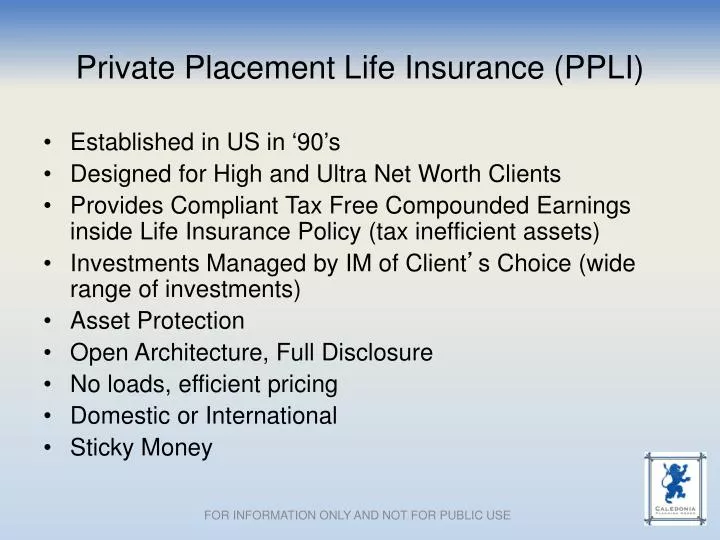

Private Placement Life Insurance (PPLI). Established in US in ‘ 90 ’ s Designed for High and Ultra Net Worth Clients Provides Compliant Tax Free Compounded Earnings inside Life Insurance Policy (tax inefficient assets) Investments Managed by IM of Client ’ s Choice (wide range of investments)

E N D

Private Placement Life Insurance (PPLI) • Established in US in ‘90’s • Designed for High and Ultra Net Worth Clients • Provides Compliant Tax Free Compounded Earnings inside Life Insurance Policy (tax inefficient assets) • Investments Managed by IM of Client’s Choice (wide range of investments) • Asset Protection • Open Architecture, Full Disclosure • No loads, efficient pricing • Domestic or International • Sticky Money FOR INFORMATION ONLY AND NOT FOR PUBLIC USE

Introduction to Insurance and PPLI TYPE OF INSURANCE NEED TEMPORARY PERMANENT • Temporary Protection • No Cash Value • Non-Renewable at Older Ages • Availability & Capacity Constraints • Permanent Protection • Non-Transparent Pricing • Premium & Death Benefit Flexibility • Cash Value (Tax Deferral) • Potential Rate of Return • Permanent Protection • Insurer Manages Assets • 3-4% Guaranteed ROR • Capacity • Premium & Death Benefit Flexibility • Market Generated Returns • Permanent Protection • No Guaranteed ROR • Moderately Competitive Pricing • Availability & Capacity Constraints • Premium & Death Benefit Flexibility • Permanent Protection • High Investment Flexibility • No Guaranteed ROR • Highly Competitive Pricing (transparent) • Significant Capacity • Premium & Death Benefit Flexibility TERM INSURANCE UNIVERSAL LIFE VARIABLE UNIVERSAL LIFE PRIVATE PLACEMENT LIFE WHOLE LIFE FOR INFORMATION ONLY AND NOT FOR PUBLIC USE

Typical Domestic versus International Pricing *BOY, Pricing may reflect expenses in first year or amortized in attempt to enhance early year CSV’s FOR INFORMATION ONLY AND NOT FOR PUBLIC USE

U.S. vs. Canadian PPLI • Major Differences: • Diversification rules IRC 817(h) • Investor Control Rev. Rul. 2003-91 • Insurance Dedicated Funds (IDF) • Definition of Life Insurance 7702(a) vs MTAR • None applicable in Canada FOR INFORMATION ONLY AND NOT FOR PUBLIC USE

Why Joint/Dual Compliant • IRS: Long Reach of Uncle Sam • Definition of Life Insurance 7702(a) vs MTAR, Exemption Test Section 306 • FATCA FOR INFORMATION ONLY AND NOT FOR PUBLIC USE

Fact Pattern • Male 55, non-smoker, standard risk • Premium $520,000 for 4 years • Interest rate 6% • US citizen living in Canada

Summary • First of its kind • Compliant on both sides • No investor control or diversification requirements • No DAC tax • No State or Provincial premium taxes FOR INFORMATION ONLY AND NOT FOR PUBLIC USE