Download

1 / 33

330 likes | 436 Views

Inflation, Unemployment, & Stabilization Policies 20-30% of AP Exam. Section 6. Unit Outline. A . Fiscal and monetary policies 1 . Demand-side effects 2 . Supply-side effects 3 . Policy mix 4 . Government deficits and debt B . The Phillips curve 1 . Short-run and long-run Phillips curves

E N D

Inflation, Unemployment, & Stabilization Policies20-30% of AP Exam Section 6

Unit Outline • A . Fiscal and monetary policies • 1 . Demand-side effects • 2 . Supply-side effects • 3 . Policy mix • 4 . Government deficits and debt • B . The Phillips curve • 1 . Short-run and long-run Phillips curves • 2 . Demand-pull versus cost-push inflation • 3 . Role of expectations

Fiscal Policy, Deficit, & Public Debt Module 30

Reminder: Fiscal Policy • Government decisions about tax rates and spending levels. • Two types: • Expansionary – Grows the economy/increases deficit • Decrease Taxes • Increase Spending • Increase transfers • Contractionary– Slows the economy/reduces deficit • Increase Taxes • Decrease Spending • Decrease Transfers

The Budget Balance • The budget balance is the difference between the government’s tax revenue and its spending, both on goods and services and on government transfers, in a given year. • A budget surplus is a positive budget balance and a budget deficit is a negative budget balance. • the budget balance (or savings by the government) is defined by: • SGovernment = T - G – TR • T is the value of tax revenues • G is government purchases of goods and services • TR is the value of government transfers.

Fiscal Policy and the Budget Balance: • Expansionary Policies reduce the budget balance for the year • Contractionary Policies increase the budget balance for the year

Example 1: Recessionary Gap • Expansionary fiscal policy is in order. • 3 options: • Cut taxes. • Increase transfers. • Increase government spending. • These three policies should increase AD and reverse the recession, but will cause the budget balance to decrease. This means either a smaller surplus or a bigger deficit.

Example 2: Inflationary Gap • Contractionary fiscal policy is in order. 3 options: • Increase taxes. • Decrease transfers. • Decrease government spending. • These three policies should decrease AD and reverse the inflation, but will cause the budget balance to increase. This means either a bigger surplus or a smaller deficit.

Keep in mind: • Changes in the budget balance don’t always perfectly reflect changes to fiscal policy. • Just because the balance is decreasing does not mean an expansionary policy is being implemented • Two important reasons why it is more complicated. • Two different changes in fiscal policy that have equal-size effects on the budget balance may have quite unequal effects on the economy. • Example: If government spending increases by $1000, it will have a larger impact on real GDP than a tax decrease of $1000. The budget balance would change by $1000 in each case, but the impacts would be different. • Often, changes in the budget balance are themselves the result, not the cause, of fluctuations in the economy.

Other Problems with Fiscal Policy 1. Problems of Timing • Recognition Lag- Congress must react to economic indicators before it’s too late • Administrative Lag- Congress takes time to pass legislation • Operational Lag- Spending/planning takes time to organize and execute (changing taxing is quicker)

Other Problems with Fiscal Policy 2. Politically Motivated Policies • Politicians may use economically inappropriate policies to get reelected. • Ex: A senator promises more public works programs when there is already an inflationary gap.

Other Problems with Fiscal Policy 3. Crowding-Out Effect • If the government spends more money, and needs to increase borrowing, it will lead to increased interest rates • This may “crowd out” business and individuals and decrease investment spending which will in turn reduce economic growth

Monetary Policy and Interest Rates Module 31

Reminder: Monetary Policy • Actions taken by the Federal Reserve (or a central bank) to control the supply of money • Two types: • Expansionary – Lowers interest rates/grows the economy/increases inflation • OMO: Buy bonds • Lower Reserve Requirement • Lower Discount Rate • Contractionary– Increases interest rates/slows the economy/reduces inflation • OMO: Sell Bonds • Increase Reserve Requirement • Increase Discount Rate

Monetary Policy • Main tool of stabilization policy in practice • Like Fiscal Policy, there are lags BUT Central Banks are able to act more quickly then the government in implementing changes.

Target Federal Funds Rate • Fed Funds Rate – Interest rate banks charge other banks for loans (based on Discount Rate) • Every 6 weeks, when the FOMC meets, a Target FFR is set. • This target rate is reached through Open Market Operations carried out at the New York branch. • This alters the supply of money and allows the FED to drive rates up or down.

Monetary Policy and Aggregate Demand • Expansionary Policy • Lower interest rates = higher investment spending • Higher investment spending = higher GDP • Higher GDP = more consumer spending

Monetary Policy and Aggregate Demand • Contractionary Policy • Higher interest rates = lower investment spending • Lower investment spending = lower GDP • ….

Monetary Policy in Practice • Central Banks tend to engage in expansionary policies when real GDP is below potential output (recessionary gap) and contractionary policies when real GDP exceeds potential (inflationary gap)

Taylor Rule • Rule proposed in 1993 by Stanford economist John Taylor • Federal Funds Rate = 1 + (1.5x inflation) + (0.5 X output gap) • This rule is the best way of predicting the Federal Reserve’s behavior when it comes to setting the discount rate

Inflation Targeting • Used by some central banks outside the US • Central Banks set a target for inflation, and implement a monetary policy to hit that target. • Two Advantages • The public knows the objective of the bank for the year • The central bank’s effectiveness can be judged by how close they are to hitting their target yearly • Disadvantage • Some argue this is too restrictive and reduces flexibility to act in a crisis.

Monetary Policy in the Long Run • In the short-run an increase in the money supply will reduce interest rates, increases investment spending, and increases consumer spending • Output and prices increase as AD shifts right • As a result of the expansionary monetary policy, output is now ABOVE potential • This will cause nominal wages to rise, and the SRAS curve to shift to the left • THE LONG RUN EFFECT OF AN INCREASE IN THE MONEY SUPPLY IS JUST AN INCREASE IN PRICE LEVELS

Monetary Nutrality • monetary neutrality: changes in the money supply have no real effects on the economy. • In the long run, the only effect of an increase in the money supply is to raise the aggregate price level by an equal percentage. • If MS grows by 50%, prices will grow by 50% • If MS decreases by 25%, prices will drop 25% • Economists argue that money is neutral in the long run.

Monetary Policy and Interest Rates (long run) • A change in the money supply lowers interest rates in the short run • However, as price levels rise, the demand for money increases • This shifts the MD curve to the right, bring interest rates back to where they began

Inflation Module 33

Inflation: Reminders • Hyperinflation • Extremely high inflation. Usually caused by a government printing out too much fiat money • Cost-push inflation • Inflation caused by a negative supply shock • AKA Stagflation • Demand-Pull inflation • Inflation caused by increased demand in the economy

Output Gap and Unemployment • Remember: • YP = Potential Output (Assumes economy is at full employment) • Short Run eq left of YP = Recessionary Gap • Unemployment is high, inflation is low • Short Run eq right of YP = Inflationary gap • Unemployment is low, inflation high

The Phillips Curve Module 34

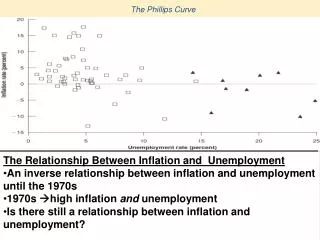

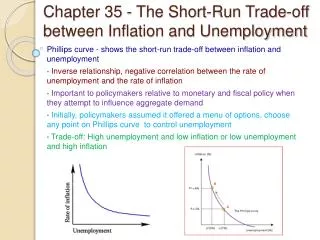

The Phillips Curve • In the short run there is a negative relationship between unemployment and inflation. • First theorized by economist Alban Phillips

Supply Shocks and the Phillips Curve • Reminder: Supply Shocks • Sudden changes in SRAS • Supply Shocks can cause the SRPC to shift • Positive, shifts down • Negative, shifts up

Expected inflation and the Phillips Curve • Increase in expected inflation shifts the SRPC up

Long Run Phillips Curve • In the long run, employment is not impacted by inflation. • Therefore the Long-run Phillips Curve is vertical at the Natural Rate of Unemployment