Download

1 / 11

140 likes | 615 Views

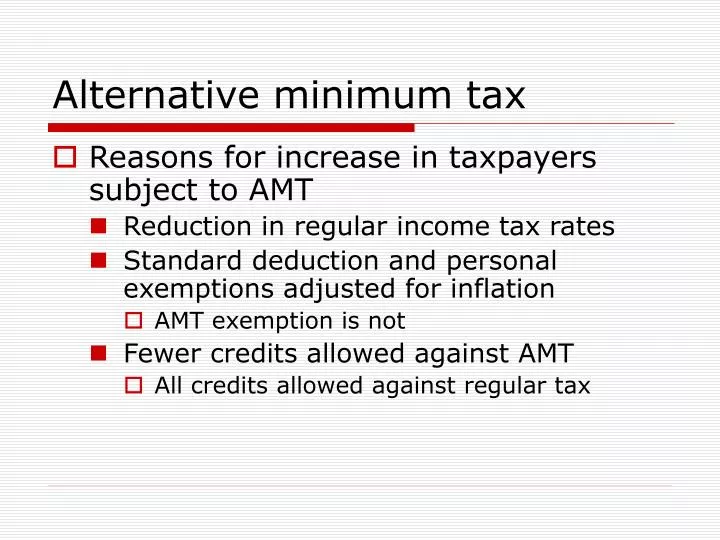

Alternative minimum tax. Reasons for increase in taxpayers subject to AMT Reduction in regular income tax rates Standard deduction and personal exemptions adjusted for inflation AMT exemption is not Fewer credits allowed against AMT All credits allowed against regular tax. What causes AMT.

E N D

Alternative minimum tax • Reasons for increase in taxpayers subject to AMT • Reduction in regular income tax rates • Standard deduction and personal exemptions adjusted for inflation • AMT exemption is not • Fewer credits allowed against AMT • All credits allowed against regular tax

What causes AMT • Following not deductible for AMT • State income taxes • Property taxes • Home equity loan interest not used for home improvements • What is deductible for AMT • Charitable contributions • Mortgage interest other than above exception

What causes AMT • Credits allowed against regular tax • Child tax credit • Education credit • Dependent care credit • Adoption credit • Residential energy credit • Credits against AMT • Child tax credit • Adoption credit

Preferences • Incentive stock options (ISOs) • Income tax implications ( regular, AMT, basis) • Upon grant • Option price must be equal to stock price (110% of stock price for > 10% owner) • FMV stock thru option exercise must be < $100,000 per year • Expiration: 10 years from date of grant • Typically a portion vests each year (maybe 20% each year) • Can only be transferred on death of employee

Preferences • Incentive stock options (ISOs) • Upon exercise • Basis is equal to option price • Difference between option price and the value of stock on date of exercise is an AMT preference item • Exercising option before stock price increases reduces preference item but does subject employee to risk associated with ownership of the stock • AMT basis is equal to stock price on date of exercise; not option price • Higher basis for AMT if price has increased

Preferences • Incentive stock options (ISOs) • Holding period requirements • Long-term capital gains (15% maximum rate) if: • Stock sold more than two years after option was granted • Stock sold more than one year after option was exercised

Preferences • Incentive stock options (ISOs) • Disqualifying dispositions • if: • Stock sold less than two years after option was granted • Stock sold less than one year after option was exercised • Bargain element (stock price on date of exercise and the option price) is compensation income taxed at ordinary rates • Difference between sales price and exercise price is taxed at capital gains rates • If stock price falls after exercise, then have a capital loss subject to $3,000 annual limitation

AMT Planning Techniques • Incentive stock options (ISOs) • Stagger exercises so ISO preference is below amount which would create AMT • Then when sell stock, which creates a negative AMT adjustment, exercise more options • If stock price falls after exercise sell stock • Disqualifying disposition • No AMT issue as AMT and regular tax gain will be same

AMT Planning Techniques • NQSO • No limits on granting NQSOs • At exercise, • FMV stock – exercise price = • Additional salary for employee • Subject to payroll taxes • Deductible salary for employer • Employee exchange shares of company to pay exercise cost

AMT Planning Techniques • Move income into AMT year • Until regular tax = AMT • If regular tax rate normally > 28% and AMT due to preference such as ISO • Reduce 401(k) contributions, for example

AMT Planning Techniques • Move deductions into non AMT year • Unfortunately, difficult to not pay: • State income taxes • Property taxes