Download

1 / 14

170 likes | 204 Views

Discover the latest trends and statistics in cyber liability insurance. Learn about the top reasons for purchasing coverage, recent claims reported, allocation of claim costs, and key insights into K-12 cyber incidents. Find out how cyber liability policies provide crucial protection and transfer risks through insurance.

E N D

Recent Statistics • 40% More buyers today than 2011 of Stand Alone Coverage • 10% More buyers since 2017. Largest gain ever recorded • Top Reasons for Buying Coverage: • Expenses & Fines related to a breach • Liability Costs • Reputation of Your Organization • Top Claims Reported in 2018: • Hacking remains #1 • Ransomware • Phishing Attacks

Recent Statistics • Claims almost Doubled from 2017 to 2018 • Claims have Grown 4x since 2016 • 2018 Allocation of Cyber Claim Costs: • IT Forensics 51% • Breach Coach 30% • Notification Costs 12% • Incidents Grew 38% Overall from 2017 to 2018 • Financial Fraud Up 89 from 2017 to 2018 • Ransomware Demands Skyrocketing in $$$ Size

2018 K-12 Statistics/Trends • More than Half were carried out or caused by “Insiders” (Staff or Students) • 23% were a result of a loss of control of Vendors or Partners. Highlights the Need to Strengthen “Contractual Requirements” of Those you are Doing Business with. • Another 23% Carried out by “Unknown Actors”. External to School Community. • 60% of Breaches included Student Data • 46% Included Data about Current or Former Staff Members • Most Concerning was many Attacks were targeted at School Business Officials including largest ever @ $2mm!!!

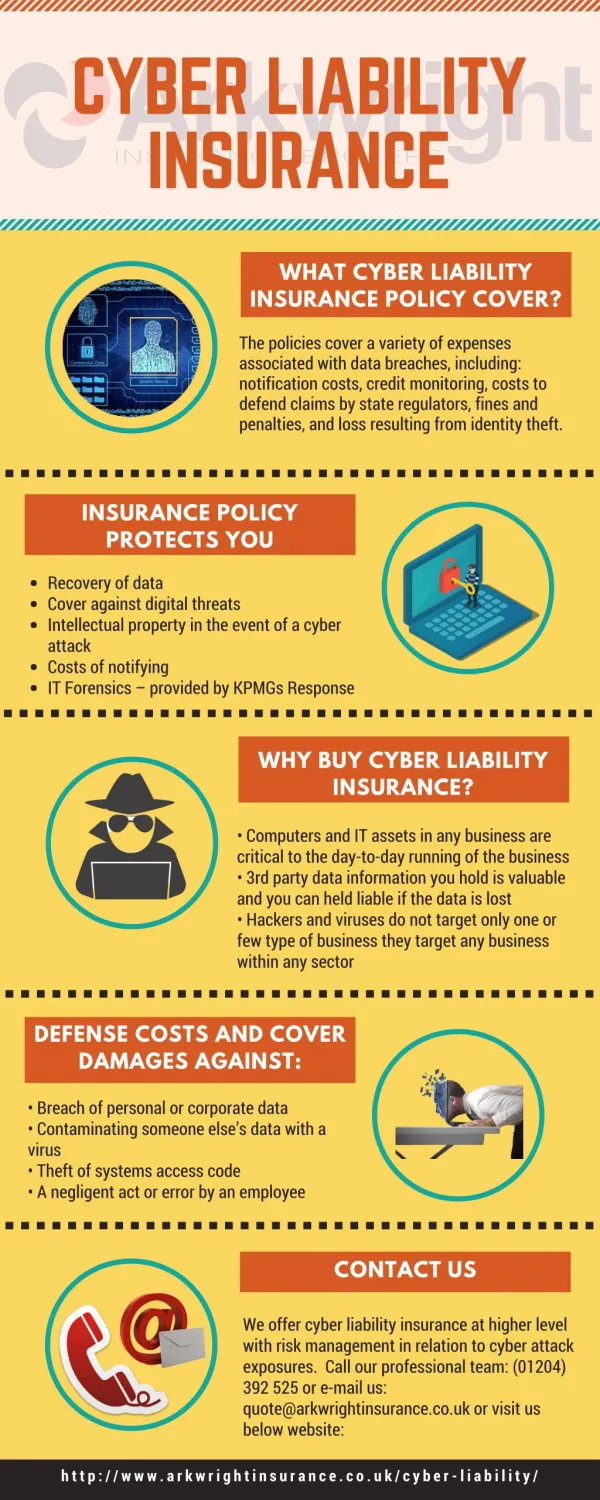

Transfer of Risk Through Insurance Traditional Property and Casualty Policies • Provide protection for bodily injury and property damage from physical perils Fidelity or Crime Policy • Provides protection against the theft of money, securities and tangible property Cyber Liability Policy • Provides protection for network security, privacy and the theft or release of confidential information – both personal and business

Property & Casualty Insurance Not developed to cover cyber exposures • Language did not specifically address the exposures • Pricing did not contemplate the risk • Early avenues of possible coverage have been closed Emerging expansion of cover under property policies • Some expansion to address business interruption

Fidelity or Crime Insurance Typically Includes • Computer Fraud • Funds Transfer Fraud • Forgery Often inadequate to address today’s exposures • Nuances in policy language and varying interpretations leave gaps in coverage Look to add affirmative coverage • Social Engineering – Fraudulent Transfer Coverage

Cyber Liability Insurance Addresses Network Security and Privacy Liability Incidents • First Party Costs – the costs an organization faces when dealing with a breach incident • Third Party Liability – the costs an organization faces for their liability to others as a result of a breach incident

First Party Costs Typical Breach Event Costs Include • Legal guidance • Forensics investigation • Crisis management / public relations • Breach notification costs • Credit monitoring Other Business Costs Include • Business interruption • Data restoration • Extortion • Cyber crime – social engineering • Consequential reputational loss

Third Party Costs Civil Lawsuits • Consumer class action • Corporate or financial institution suits • Credit card brands • PCI fines, penalties and assessments Regulatory Actions • State AG investigations • FTC investigations • Health and human services – i.e. HIPAA • Foreign privacy entities – GDPR

Access to Key Resources At the time of loss • Forensics firm – who, what, where, when • Attorney for various state compliance requirements • Including contractual indemnification obligations • Public Relations expense – brand protection • Credit monitoring, notification assistance • ID restoration services • Licensed investigator/fraud specialist Pre-breach loss mitigation services • Access to free and discounted services

IT security, policies and procedures don’t always work! Cyber insurance fills gaps in “traditional” insurance Acts as a financial backstop to the organization Assists the organization with continuity planning Helps to establish relationships with key vendors Demonstrates an organizational commitment to network security and privacy Insurance as a Last Line of Defense