Download

1 / 20

200 likes | 215 Views

This text explores the tax treatment of a stock redemption transaction, whether it is treated as an exchange or a dividend under Section 301. It covers various rules and options, such as attribution rules, substantially disproportionate redemption, complete termination, and partial liquidation.

E N D

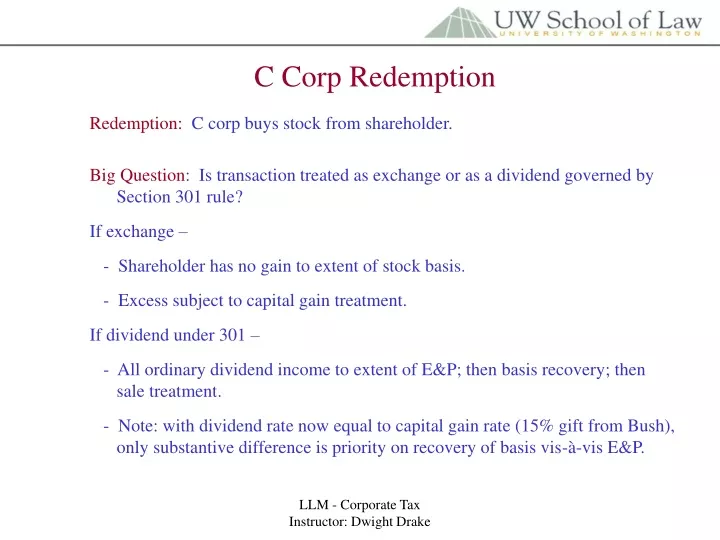

C Corp Redemption Redemption: C corp buys stock from shareholder. Big Question: Is transaction treated as exchange or as a dividend governed by Section 301 rule? If exchange – - Shareholder has no gain to extent of stock basis. - Excess subject to capital gain treatment. If dividend under 301 – - All ordinary dividend income to extent of E&P; then basis recovery; then sale treatment. - Note: with dividend rate now equal to capital gain rate (15% gift from Bush), only substantive difference is priority on recovery of basis vis-à-vis E&P. LLM - Corporate Tax Instructor: Dwight Drake

Four Options Under 302(b) (b)(1) - Not essentially equivalent to a dividend (b)(2) - Substantially disproportionate (b)(3) - Complete termination of shareholders interest (b)(4) - Partial liquidation LLM - Corporate Tax Instructor: Dwight Drake

318 Attribution Rules Family Attribution - Parents, spouse, children, grandchildren. No sibling, in-law or grandparent attribution. Entity from attribution - Proportional attribution to owner or beneficiary for stock owned by partnership, estate or trust. Corporate proportionate attribution (based on FMV of stock) to shareholder who owns, directly or via attribution, 50% or more of stock value. Entity to attribution - Stock owned by partners or beneficiaries attributed to partnership, estate or trust. Attribution to corp only for stock held by 50% or more shareholder. Option attribution - All stock subject to option deemed owned by the holder of option. Chain attribution – generally Ok (child to parent to corp), but no double family attribution (child to parent to grandparent). LLM - Corporate Tax Instructor: Dwight Drake

302(b)(2) – Substantially Disproportionate Three mechanical requirements: 1. After redemption, shareholder owns less than 50% of total combined voting power. 2. After redemption, percent of voting stock less than 80% of percentage of voting before redemption. 3. After redemption, percent of all common (voting and non-voting) less than 80% of percentage before redemption. Note: - Full attribution rules apply. - Multiple transactions part of common plan are aggregated. Rev. Rule 85-14. LLM - Corporate Tax Instructor: Dwight Drake

302(b)(3) – Complete Termination Requirement: Shareholder is finished – takes a permanent hike. Only remaining interest can be creditor – nothing else. The Big Break: No family attribution. Makes it possible to transition corp stock to next generation. Special rules: - 10 year forward rule: Selling shareholder not acquire any stock for 10 years, except by bequest or inheritance. - 10 year back rule: Last 10 years, selling shareholder acquired stock from 318 relative or 318 relative acquired stock from selling shareholder. Not apply if tax avoidance not principal purpose. LLM - Corporate Tax Instructor: Dwight Drake

Problem 213 -1 Wham Corp. 10 Shares 30 Shares 20 Shares 25 Shares 15 Shares GF AdoptedSon Daughter GM Estate Mom 50% 5 Share option 50% Cousin GF constructive ownership: 25 personal + 20 mother direct + 25 from grandchildren + 15 from estate via mother = 85. Daughter constructive ownership: 15 personal + 20 mother direct + 5 mother via option + 15 estate via mother = 55. GM Estate constructive ownership: 30 direct + 70 mother (including 20 mother, 25 GF and 25 kids) = 100. LLM Corporate Tax Instructor: Dwight Drake

Problem 213 -2(a) Y Corp X Corp Partnership. 100% Shares 100% 25 % 25 % 25 % 25% D C B A W Married (a) A ownership of X Corp: 25 shares via partnership. W ownership of X Corp: 25 shares via A spouse and partnership. W’s mother: 0 because no in-law attribution. LLM Corporate Tax Instructor: Dwight Drake

Problem 213 -2(b)(c) Y Corp X Corp Partnership. 100% Shares 100% 25 % 25 % 25 % 25% D C B A W Married (b) Y corp ownership of X Corp: 25 shares via A to W and W to Y corp (50% or more shareholder). If W owned 10% of Y, no attribution to Y because 50% or more test not satisfied. (c) Y shares owned by Partnership: All 100 via W to A to Partnership. B,C & D partners: No Y shares. No sideways attribution – from partner to partnership to other partners. X Corp ownership of Y: All 100 shares via partnership ownership. LLM Corporate Tax Instructor: Dwight Drake

Problem 217-1(a) Redeem 75 Preferred Alice Y Corp. Cathy 80 Common, 100 NV Preferred 20 Common, 100 NV Preferred (a) 1/15 – T redeems 75 of A’s preferred shares. No hope under 302(b)(2) because only nonvoting redeemed. Reg. 1.302-3(a). LLM Corporate Tax Instructor: Dwight Drake

Problem 217-1(b) Alice Y Corp. Cathy Redeem 75 Preferred, 60 Common 80 Common, 100 NV Preferred 20 Common, 100 NV Preferred (b) Y also redeems 60 of A’s common shares. No hope under (b)(2) because A owns 50% of voting common after redemption – 20 out of 40 shares. Must own less than 50% voting per 302(b)(2)(B). LLM Corporate Tax Instructor: Dwight Drake

Problem 217-1(c) Alice Y Corp. Cathy Redeem 75 Preferred, 70 Common 80 Common, 100 NV Preferred 20 Common, 100 NV Preferred (c) Y redeems 70 of A’s common shares. 302(b)(2) satisfied. Less than 50% voting after (33%); percentage voting and common after (33%) less than 80% of percentage voting and common before (80%). Preferred stock redemption gets “piggybacked” and qualifies under 302(b)(2) per Reg. 1.302-3(a). LLM Corporate Tax Instructor: Dwight Drake

Problem 217-1(d) On 1/15 Alice Y Corp. On 12/1 Cathy Redeem 75 Preferred, 70 Common Redeem 10 Common 80 Common, 100 NV Preferred 20 Common, 100 NV Preferred d) On 12/1, 10 shares of C’s common stock redeemed. Issue is whether they are linked. If not, A’s redemption qualifies under (b)(2) per above. If they are linked, A owns 50% of common after (10 of 20) and thus would not qualify. Note, the 80% “substantially disproportionate” tests are satisfied, not the 50% test. Is 302(b)(2)(D) applicable where only issue is 50% test? Technically “No”. Standard step-transaction principles would be applied. Big question: Were events linked and planned together? LLM Corporate Tax Instructor: Dwight Drake

Problem 217-2 Redeems 30 voting common Don Z Corp. Jerry 60 V Common, 100 NV Common 40 V Common, 100 NV Common Issue is 302(b)(2). - D voting interest goes from 60% to 42.8% - thus overall 50% voting test and voting 80% test satisfied. - D total percentage common before was 53.3% (160/300) and is 48.1% after. Flunk overall 80% test. Thus, not qualify under 302(b)(2). - Note: Likely would qualify under 302(b)(1) by virtue of loss of control. LLM Corporate Tax Instructor: Dwight Drake

Problem 235-1(a),(b),(c) J Father Redeems 50 Common 100 Common A Daughter R Corp. C Gran Son 50 Common 25 Common (a) R redeems A’s 50 shares. Qualifies under 302(b)(3) with waiver of family attribution under 302(c)(2). Must timely file agreement per 302(c)(2)(A)(iii). (b) Same, but A fails to file agreement. Per Reg. 1.302-4(a)(2), A will get reasonable extension if (1) reasonable cause for not filing, and (2) request filed within reasonable time. Statute of limitations extended one year after notification. (c) Same, but price paid to A dependant on R’s profits. No 302(b)(3) because no waiver of family attribution. Profits interest is forbidden interest – more than just a creditor. Reg. 1.302-4(d). Amount or certainty can’t be contingent on profits. LLM Corporate Tax Instructor: Dwight Drake

Problem 235-1(d) thru (f) J Father Redeems 50 Common 100 Common A Daughter R Corp. C Gran Son 50 Common 25 Common (d) R redeems 20 A’s shares year 1, 30 shares year 2. Year 2 redemption qualifies under (b)(3). Year 1 qualifies only if it part of “firm and fixed” plan to redeem all. Need not be in writing or binding to be “firm and fixed”. (e) Same, but A remains director. No hope under (b)(3) because no waiver of family attribution. A holds interest more than a creditor. 302(c)(2)(A)(i). Even as inactive director, probably cooked in 9th circuit. (f) Same, but two years later R forms sub that employs A. No hope under (b)(3). Can have no interest for ten years and this extends to activity of subsidiary. Reg. 1.302-4(c). LLM Corporate Tax Instructor: Dwight Drake

Problem 235-1(g) J Father Redeems 50 Common 100 Common A Daughter R Corp. C Gran Son 50 Common 25 Common (g) Same, but C dies in two years and leaves stock to A. 302(b)(3) and waiver of family attribution still good per parenthetical exception in 302(c)(2)(A)(ii). LLM Corporate Tax Instructor: Dwight Drake

Problem 235-2(a) Redeems 120 for 20 year note Betty & Bill B&B Corp. 150 common + building lease Gift 30 Common Junior Son (a) Will redemption qualify under 302(b)(3)? - 20 year note term outside IRS ruling standard (15 year). Some courts have allowed as long as 20 yrs, but risky. Better to keep at 15 yrs. Creditor covenants and security permitted. Rev. Rule 59-119. - Continued rental and option permitted if not dependant on profits and terms are arms-length terms. Rev. Rule 77-467. - Child 30 share gift not violate 302(c)(2)(B)(ii) unless principal purpose tax avoidance. Since Son worked for company and is targeted successor, should have no problem here. Rev. Rule 77-293. LLM Corporate Tax Instructor: Dwight Drake

Problem 235-2(b) Redeems 120 for 20 year note Betty & Bill B&B Corp. 150 common + building lease Gift 30 Common Junior Son (b) Same, but Betty establishes consulting firm after leaving and firm is hired by B&B Corp. Per Lynch case and Rev. Rule 70-104, consulting deal would kill 302(b)(3). Some limited authority to contrary where accounting services provided as independent contractor. Very risky. Dead in 9th cir. LLM Corporate Tax Instructor: Dwight Drake

Problem 235-3(a),(b) J Son Redeems 20 Common 50 Common Father Estate C Corp. 20 Common M Daughter 30 Common B Mom C redeems 20 shares owned by Estate. 302(b)(3) works if both Estate and B satisfy waiver of family attribution requirements and sign required agreement. 302(c)(2)(C). Same, but B residuary beneficiary of Estate and J and M each receive specific legacies. No hope for waiver of family attribution for estate per 302(c)(2)(C) if redemption with estate. Best to distribute legacies to J and M, then redeem from Estate. LLM Corporate Tax Instructor: Dwight Drake

Problem 235-3(c),(d),(e). J Son Redeems 20 Common 50 Common Father Estate C Corp. 20 Common M Daughter 30 Common B Mom • (c) Same, but J and M are residuary beneficiaries of Estate. No hope under 302(b)(3), as J and M’s stock attributed to Estate. • 20 shares left to QTIP, income to B for life, then to third child N. C redeems shares. 302(b)(3) permitted if B and trust join waiver agreement. Note, K as sibling not deemed “related” under 318(a)(1). • Same as (d), but N acquires stock of C three years after redemption. Violates 10 year look-back rule of 302(c)(2)(A(ii) because N’s stock attributed to trust under 318(a)(3)(A). Only family attribution waived under 302(c)(2), not entity attribution. LLM Corporate Tax Instructor: Dwight Drake