Download

1 / 22

220 likes | 370 Views

Introduction Terminology Valuation-Simple Valuation-Actual Sensitivity. What is a financial option? It is the right , but not the obligation, to buy (in the case of a call option ) or sell (in the case of a put option) a stock at a certain price through a certain time.

E N D

IntroductionTerminology Valuation-Simple Valuation-Actual SensitivityIntroductionTerminology Valuation-Simple Valuation-Actual Sensitivity What is a financial option? It is the right, but not the obligation, to buy (in the case of a call option) or sell (in the case of a put option) a stock at a certain price through a certain time.

IntroductionTerminologyValuation-Simple Valuation-Actual SensitivityIntroductionTerminologyValuation-Simple Valuation-Actual Sensitivity Exercise price is the price at which the option owner may buy the stock. Such buying is referred to as exercising the option. Expiration date is the date when the option expires. The option owner’s right to buy the stock at the exercise price expires on this date. European options can only be exercised on expiration date. American options can be exercised any time through the expiration date. Employee stock options are usually American call options.

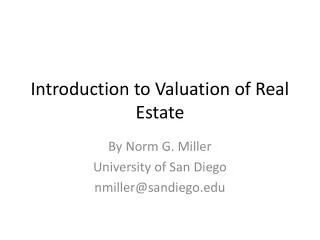

Introduction TerminologyValuation-SimpleValuation-Actual Sensitivity Value of a call option at expiration is a function of the stock price and the exercise price. Example: Option values on expiration date given an exercise price of $85. Stock price 60 70 80 90 100 110 Option value 0 0 0 5 15 25 At any stock price less than $85, the option is worthless. If the option owner was interested in buying the stock, she could purchase the stock more cheaply from her broker!

Call option value on expiration date given an $85 exercise price. Introduction TerminologyValuation-SimpleValuation-Actual Sensitivity Call option value $20 85 105 Share Price

Introduction TerminologyValuation-SimpleValuation-Actual Sensitivity Intrinsic value is the value an option would have if it were exercised immediately. Hence, an option may have different intrinsic values at different points in time. For a call option, its intrinsic value is the maximum of zero and ST - X, where ST is the stock price at time T, and X is the exercise price. Fair option value is the present value of the option’s intrinsic value.

Introduction TerminologyValuation-SimpleValuation-Actual Sensitivity Assume the share price of a particular stock one year from now will be $105. What is the fair option value of an option on this stock with an exercise price of $85, expiring a year from now? Intrinsic value = 105 – 85 = $20. Fair option value is the present value of the option’s intrinsic value. Assume a discount rate of 5%. Fair option value = 20 / (1+.05) = $19.05.

Introduction TerminologyValuation-SimpleValuation-Actual Sensitivity If future stock price is uncertain… Assume there is an equal (20%) probability that a year from now the stock price would be $75, $85, $95, $105, or $115. What is the fair option value of an option on this stock with an exercise price of $85, expiring a year from now? Fair option value = Sum of probability weighted PV = 5.71 + 3.81 + 1.90 + 0 + 0 = $11.42

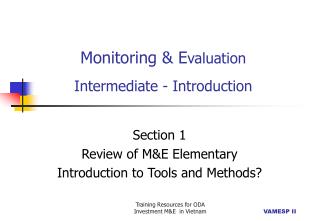

Introduction TerminologyValuation-SimpleValuation-Actual Sensitivity Upper and Lower Bounds for Option Prices Notation S: Current stock price ST: Stock price at time T T: Time to expiration for the option X: Exercise price r: Risk-free rate through time T c: Value of European call option to buy one share C: Value of American call option to buy one share Upper Bounds The stock price is an upper bound to the option price. Else, an arbitrageur can make a riskless profit by buying the stock and selling the call option. c < S C < S

Introduction TerminologyValuation-SimpleValuation-Actual Sensitivity Lower Bounds for Call Options on Non-dividend Paying Stocks c > S – Xe-rT C > S – Xe-rT c = C Consider two portfolios: Portfolio A: One European call option (c) plus cash equal to Xe-rT. Portfolio B: One share (S). Value of portfolio A at T: Cash if invested in the risk-free interest rate grows to X. If ST > X, call is exercised and portfolio is worth ST. If ST < X, call expires worthless, and portfolio is worth X. Value of portfolio B at T: ST. Hence, portfolio A is always worth as much as, and is sometimes worth more than, portfolio B at time T. Hence, c + Xe-rT > S, or, c > S – Xe-rT

Introduction TerminologyValuation-SimpleValuation-Actual Sensitivity Lower Bounds for Call Options on Non-dividend Paying Stocks Early exercise: It is never optimal to exercise an American call option on a non-dividend paying stock early. Consider an American call option on a non-dividend paying stock with a month to expiration. S=$100. X=$85. The option is deep in the money and the option owner may be tempted to exercise it immediately. However, if the option owner wishes to hold the stock for more than one month, this is not the best strategy. The better strategy is to keep the option and exercise it at the end of the month. Two advantages: First, the exercise price is paid one month later. Second, there is some chance (however remote) that the stock price will be below $85 at the end of month. In this case the option owner would be glad to not have exercised the option. What if the option owner wishes to hold the stock for less than one month?

Introduction TerminologyValuation-SimpleValuation-Actual Sensitivity Lower Bounds for Call Options on Non-dividend Paying Stocks Early exercise: It is never optimal to exercise an American call option on a non-dividend paying stock early. What if the option owner wishes to hold the stock for less than one month? In this case the option owner is better off selling the option than owning it. The option will be bought by another investor who wants to own the stock. Such investors must exist, otherwise, the current stock price would not be $100. The price obtained for the option would be greater than its intrinsic value of $15, since the exercise price does not have to be paid for a month. Hence, C=c, and C > S – Xe-rT

Upper and Lower Bounds for Option Prices Introduction TerminologyValuation-SimpleValuation-Actual Sensitivity C=S Call option value (C) $20 85 105 Share Price (S)

Introduction TerminologyValuation-SimpleValuation-Actual Sensitivity A realistic model for future stock prices The stock price at expiration is the key to valuing an European option, But… It is impossible to exactly predict future stock prices. However, we have models that give us a realistic probability distribution of future stock prices. The Geometric Brownian Motion is one widely-used model of the probability distribution of future stock prices. If future stock prices follow the Geometric Brownian Motion, then future stock returns will be normally distributed. The well-known Black-Scholes option pricing model assumes that future stock prices follow the Geometric Brownian Motion.

Introduction TerminologyValuation-SimpleValuation-Actual Sensitivity Black-Scholes Call Option Valuation Co = SoN(d1) - Xe-rTN(d2) where, d1 = [ln(So/X) + (r + 2/2)T] / (T1/2) d2 = d1 + (T1/2) where, Co = Current call option value. So = Current stock price. N(d) = probability that a random draw from a normal distribution will be less than d.

Introduction TerminologyValuation-SimpleValuation-Actual Sensitivity Black-Scholes Call Option Valuation Co = SoN(d1) - Xe-rTN(d2) where, d1 = [ln(So/X) + (r + 2/2)T] / (T1/2) d2 = d1 + (T1/2) where (continued), X = Exercise price. e = 2.71828, the base of the natural log. r = Risk-free interest rate (annualizes continuously compounded with the same maturity as the option). T = time to maturity of the option in years ln = Natural log function Standard deviation of annualized continuously compounded rate of return on the stock

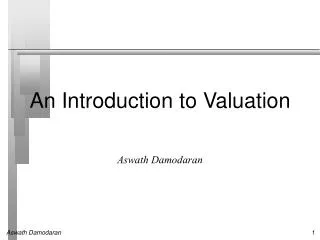

Introduction TerminologyValuation-SimpleValuation-Actual Sensitivity Black-Scholes Call Option Valuation Co = SoN(d1) - Xe-rTN(d2) where, d1 = [ln(So/X) + (r + 2/2)T] / (T1/2) d2 = d1 + (T1/2) What is the price of a call option on stock when its share price was $143.50? when, X= $11.98. Assumptions: 2 = 70%, T=0.08 years, r=5% Using the above Black-Scholes valuation equation, Value of call option = $131.57 How does the call option value change with the assumptions: 2 ,T, r ?

Sensitivity of Black-Scholes Option Value to Variance of stock returns Introduction TerminologyValuation-Simple Valuation-ActualSensitivity

Sensitivity of Black-Scholes Option Value to Variance stock returns 131.605 131.6 131.595 131.59 Black-Scholes Option Value ($) 131.585 131.58 131.575 131.57 131.565 0 1 2 3 4 5 Variance of stock returns Introduction TerminologyValuation-Simple Valuation-ActualSensitivity

Sensitivity of Black-Scholes Option Value to Time to Maturity (in years) Introduction TerminologyValuation-Simple Valuation-ActualSensitivity

Introduction TerminologyValuation-Simple Valuation-ActualSensitivity

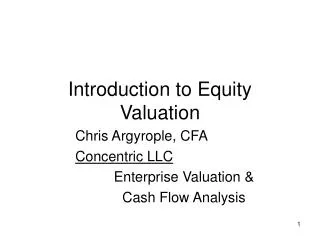

Sensitivity of Black-Scholes Option Value to Risk-free Rate Introduction TerminologyValuation-Simple Valuation-ActualSensitivity

Introduction TerminologyValuation-Simple Valuation-ActualSensitivity