Download

1 / 26

260 likes | 409 Views

Explore the significance of econometrics, from methodology to specialized regression models, simultaneous equations, time series analysis, and qualitative choice models. Learn how econometrics combines economics, mathematics, and statistics to analyze economic phenomena with references and illustrations.

E N D

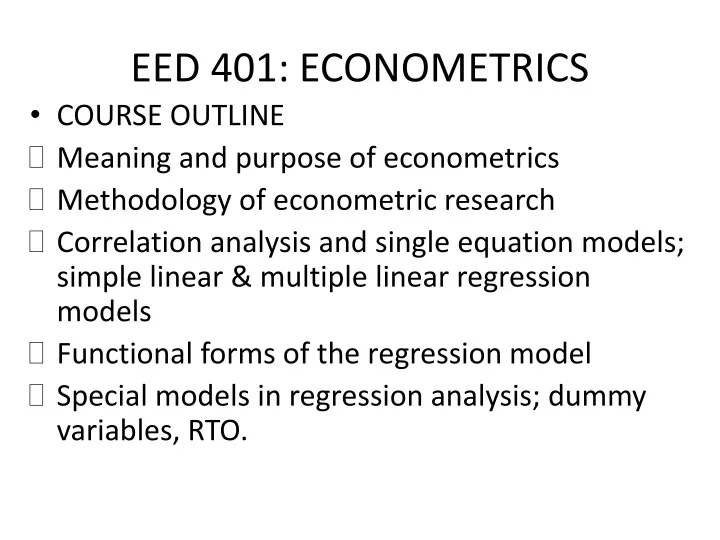

EED 401: ECONOMETRICS • COURSE OUTLINE • Meaning and purpose of econometrics • Methodology of econometric research • Correlation analysis and single equation models; simple linear & multiple linear regression models • Functional forms of the regression model • Special models in regression analysis; dummy variables, RTO.

COURSE OUTLINE CONT’D • Problems of single equation models; autocorrelation, heteroscedasticity, multicolinearity, errors in variables • Simultaneous equation models and estimation • Qualitative choice models • Time series analysis

SOME REFRENCES • A. KOUTSOYIANNIS (2003). THEORY OF ECONOMETRICS. 2ND EDITION. PELGRAVE • JEFFREY M. WOOLDRIDGE. INTRODUCTORY ECONOMICS- A MODERN APPROACH • DAMODAR N. GUJIRATI. BASIC ECONOMETRICS. FOURTH EDITION. • ETC, ETC.

WHAT IS ECONOMETRICS? • The word ‘econometrics’ is derived from two Greek words, oikovoμia (economy), and μetpov(measure) • Definition: the social science in which the tools of economic theory, mathematics and statistical inference are applied to the analysis of economic phenomena (Arthur Goldburger, 1964).

WHAT IS ECONOMETRICS? CONT’D • Thus, econometrics is an amalgam of economics, mathematics and statistics • The uniqueness of econometrics lies in the inclusion of a random element in models ILLUSTRATION (economic model of crime) • Based on economic reasoning (theory) time spent on criminal activity by an individual will depend on, hourly ‘criminal wage’ ( ),

WHAT IS ECONOMETRICS? CONT’D • Hourly wage in legal employment, • Income other than from crime or employment, • Probability of getting caught, • Probability of being convicted if caught, • Expected sentence if convicted, • Age,

WHAT IS ECONOMETRICS? CONT’D • The above depicts an exact relationship ie the time spent on crime is completely dependent on 7 factors • This is stated mathematically as: • Or

WHAT IS ECONOMETRICS? CONT’D • This still leaves us with a deterministic relationship • But there are other factors that influence crime apart from the 7. eg. health, vengeance, religion, etc. • Econometrics introduces a random factor (stochastic term) which takes care of these ‘other’ factors

Econometric representation of the crime model CONT’D. • U is the random factor encapsulating all other random factors that affect time spent on crime • PROCEDURE FOR TESTING ECONOMIC THEORY

Reading assignment • Establish the superiority of econometrics to mathematical economics and statistics

Branches of econometrics • Two main branches: -Theoretical econometrics –dev’t. of appropriate methods for the measurement of economic relationships -Applied econometrics: application of econometrics to specific fields of economic theory ( demand, supply, investment, production) for the analysis of economic phenomena and forecasting economic behaviour

Purpose of econometrics • Policy-making: Provide numerical values for the parameters of economic relationships (elasticities, propensities, marginal values) for decision making • Analysis: Empirical verification of economic laws/theories • Forecasting: determining future values of economic magnitudes based on numerical estimates

METHODOLOGY OF ECONOMETRIC RESEARCH Generally, econometric research involves 4 stages: 1. Formulation of the maintained hypothesis: ie. The specification of the model 2.Testing of maintained hypothesis: estimation of the model by appropriate econometric method 3. Evaluation of estimates: decide on the basis of certain criteria whether the estimates are satisfactory & reliable.

METHODOLOGY OF ECONOMETRIC RESEARCH CONT’D. 4. Testing the forecasting validity of the model 1&3 are the most important for any econometric research. Require strong knowledge in the functioning of economic systems 2&4 are technical & require a deep understanding of econometrics

Formulation of the maintained hypothesis • It involves determining • Dependent and explanatory variables • The a priori theoretical expectations about the signs & the size of the parameters of the function to form the basis for the evaluation of the model • The mathematical form of the model: single vs. simultaneous equation; linear vs. nonlinear functional forms

Reasons for incorrect specification of economic models • Looseness/ imperfection of statements in economic theories • Limitation of our knowledge about factors which are operative in a particular situation • Problems associated with large data requirements of large models. Errors of specification- omission of variables, equations, & wrong mathematical form of functions

2. Estimation of the model The estimation process involves the ff. Stages: • Gathering data-: cross-sectional, time series & panel data • Examination of the identification condition of the function • Examination of the aggregation problems of the function (aggregation over individuals, commodities, time,& space) • Examination of the degree of correlation among the explanatory variables

5. Choice of the appropriate econometric technique:- i. Single equation techniques:- Classical Least Squares (CLS) OR ordinary Least Squares(OLS) method, Indirect Least Squares (ILS) or reduced-form technique, 2SLS, Limited information maximum likelihood method,etc. ii. Simultaneous equation techniques:- 3SLS, FIML

3. Evaluation of estimates Are the parameters theoretically meaningful and statistically satisfactory? We use 3 criteria for the evaluation; • Economic ‘a priori’ criteria: are the parameters of the correct signs and the right size? • Statistical criteria: first-order tests- usually by using the correlation coefficient & the standard deviation (error)

3. Econometric criteria: second-order test (test of the statistical tests). This may involve tests of consistency, efficiency, unbiasedness, assumptions, identification, etc.

4. Evaluation of the Forecasting Power of the Model • Forecasting is one of the major objectives of econometrics. • Given data on personal consumption (Y) and GDP (X) from 1982-1996 in billions of dollars the estimated consumption function is given by: • We can forecast the mean consumption expenditure for 1997 given GDP=7269.8 billion dollars as

Actual consumption for 1997 was 4913.3 billion dollars • Forecast error is 37.81 billion dollars • Question is: is the error large or small?

Properties of econometric models • Econometric models are judged based on • Theoretical plausibility • Explanatory ability • Accuracy of the estimates of the parameters • Predictive power • simplicity