Download

1 / 18

• 200 likes • 594 Views

VIX - THE FEAR INDEX. Stephen Perno Kaitlin Cherundolo. What is VIX?. VIX ticker symbol for Chicago Board Options Exchange Volatility Index VIX Measures: Market expectations Expected Movement in the S&P 500 Correlation between high value of VIX and market volatility

E N D

VIX - THE FEAR INDEX Stephen Perno Kaitlin Cherundolo

What is VIX? • VIX ticker symbol for Chicago Board Options Exchange Volatility Index • VIX Measures: • Market expectations • Expected Movement in the S&P 500 • Correlation between high value of VIX and market volatility • Relation to high option prices

History of VIX • The original VIX • Based on S&P 100 Index option prices • Extracted implied volatilities from option-pricing model (Black+Scholes, etc.) • Constructed using implied volatilities of 8 different option series • 1993 - The new VIX Index was introduced in a paper by Professor Robert E. Whaley of Duke University

History of VIX • December 24, 1993 - The VIX's lowest recorded value (between 1990 and 2008) • 2003 - The underlying index is changed from the CBOE S&P 100 Index (OEX) to the CBOE S&P 500 Index (SPX). • Estimates expected volatility from option prices in wide range of strike prices, not just at-the-money strikes as in original VIX

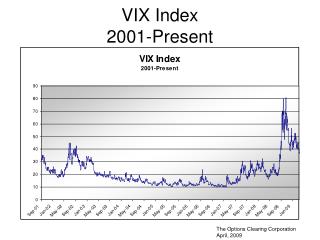

History of VIX • March 26, 2004 - Trading in futures on the VIX Index began. • February 2006 - VIX options were launched in. • October 24, 2008 - VIX reached an intraday high of 89.53. • Between 1990 and October 2008, the average value of VIX was 19.04

How Is VIX Calculated? • Old VIX calculated from Black Scholes option pricing model • Uses a newly developed formula to derive expected volatility by averaging the weighted prices of out-of-the money puts and calls • Independent of any model

Where… σ = VIX/100 VIX = 100*σ T = maturity F = forward index level derived from index prices K[i] = strike price of i-th out-of-the-money option call if K[i] > F put if K[i] < F ΔK[i] = interval between strike prices – half the distance between the strike on either side of K[i] K[0] = first strike below forward index level, F R = risk-free interest rate Q(K[i]) = midpoint of bid-ask spread for each option with strike K[i] Generalized Formula for VIX

Interpreting the Numbers • If VIX = 23, • Expected change of 23% of the S&P Index over 30 days (annualized) OR • Up and down movement in the S&P OR • Index options priced with a 68% chance that S&P 500’s 30-day return < 6.64%.

Why Is It Called the “Fear Index”? • VIX is a measure of fear of volatility in either direction • Investors believe: • High value of VIX translates into a greater degree of market uncertainty • Low value of VIX is consistent with greater stability • When investors anticipate large upside volatility, they are unwilling to sell upside "call" stock options unless they receive a large premium

Example: Long Term CapitalManagement and Russian Debt Crises in 1998

Correlation Graph for VIX and SPX Note: Negative slope implies negative correlation between VIX and SPX.

VIX-based Derivative Instruments • VIX futures contracts, which began trading in 2004 • Exchange-listed VIX options, which began trading in February 2006

Critiques of VIX • VIX measures index option volatility over 30 days when equity options have 2-6 month maturities • Volatility usually high in technology stocks, and low in utility stocks • So, VIX may be too simplistic to estimate for all types of stocks

So, Does VIX Predict the Future?!? • Given what we have seen: • Correlation = YES • Predictor = NO?

Addendum – Other Volatility Indexes Beyond VIX • Nasdaq-100 Volatility Index (VXN) • DJIA “ “ (VXD) • Russell 2000 “ “ (RVX) • S&P 500 3-Month “ “ (VXV) • Commodities and Foreign Currencies • Crude Oil “ “ (OVX) • Gold “ “ (GVZ) • EuroCurrency “ “ (EVZ)

Bibliography • http://en.wikipedia.org/wiki/VIX • http://www.cboe.com/micro/vix/vixwhite.pdf • http://www.riskglossary.com/link/spreads.htm • http://finance.yahoo.com(DOW, S&P500, and VIX)