Download

1 / 13

130 likes | 186 Views

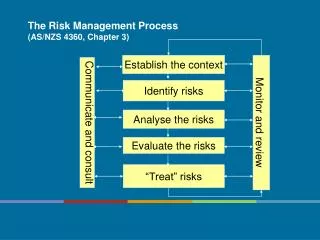

Chapter 3: The Risk Management Process (Continued). Objectives. Explain the methods used to select appropriate risk treatments; Discuss the factors that affect how risk treatments are implemented; Explain how risk management programs are monitored;

E N D

Objectives • Explain the methods used to select appropriate risk treatments; • Discuss the factors that affect how risk treatments are implemented; • Explain how risk management programs are monitored; • Apply risk management principles to a case study.

Step 3: Selecting the Best Techniques Once exposures have been identified and analyzed and alternative risk management techniques formulated to minimize the effects of those exposures, the best apparent technique or combination of techniques for dealing with each exposure is chosen. Treatment methods will be combined and integrated to effectively and economically control exposures. www.improvingyourmemorytechniques.com

The Insurance Method • Once very widely used • The client asks the producer or the insurer to price all possible insurance coverages and to assist in prioritizing the various kinds of insurance into three categories: • E • D • A • The buyer starts with the essential coverages and continues to buy until budgeted funds were used up. • BUT there is a disadvantage….

The Minimum Expected Loss Method • Better approach to select the best combination of risk management techniques • Name is misleading as includes more than just pure losses which may have to be paid. • Cost of each possible risk management technique is calculated and the results of applying each technique to potential losses is estimated. • The program that best meets these objectives with the lowest overall cost is the one chosen. • DISADVANTAGE: loss costs are often difficult to predict with certainty and effect of major capital expenditures for loss control must be adjusted to the short term.

REVIEW: Bon Ton Case Study Pg. 3 - 4 www.retailsolutionsonline.com

Step 4: Implementing Chosen Techniques • Requires a technical decision as to what should be done and managerial decisions about who should be responsible for accomplishing each phase of the program. • Communication system and method to allocate costs are also needed. www.psychologytoday.com

Deciding What To Do?!?! • Once framework has been agreed upon, details must be worked out: • Sprinkler types? • Water supply? • Contractor? Etc…… • Insurance policy terms must be negotiated and coverage must fit new risk management program. • Success of the project depends on commitment and co-operation of all senior staff members. • Producer can act as a risk management consultant.

Prioritizing and Responsibility • Prioritizing is necessitated by budget restraints and other factors. • Priorities must be set to ensure that effective implementation is achieved. • Risk manager is usually a staff officer, without line managerial authority to direct operations. Must be skilled in the art of diplomacy and tact for success. • Large organizations the objectives are codified into a risk management policy statement and a risk management manual. Small organizations, the general manager or owner makes and implements the decisions. • Policy Statement: • : Departments authority or claims handling, insurance purchasing, loss prevention audits and other similar activities.

Communication and Allocation • Requires an extensive internal and external communications network. • Communication is a two-way process. • Allocation of risk cost is important! • The cost of risk is composed of : • Cost of loss control • Insurance premiums, • Retained losses, and • Overhead of the risk management department. • Cost allocation provides risk managers with leverage. www.englishwithatwist.com

Step 5: Monitoring Results and Modification • Regular re-evaluation (and change) of programs is necessary. • Changes must be detected and the risk management program adapted to them. • Standards and benchmarks must be established to measure performance and evaluate programs. • Brokers/producers bring risk management principles to organizations. They must maintain regular contact with clients to determine if needs have changed. • An ideal risk management program is carefully formulated, tested and monitored over a long period of time.

Applying Risk Management Principles REVIEW Case Study: The Yummy Ice Cream Company Ltd. Pg. 8 - 15

Questions??? Courtesy of: www.mindlessranting101.blogspot.com