Download

1 / 38

380 likes | 499 Views

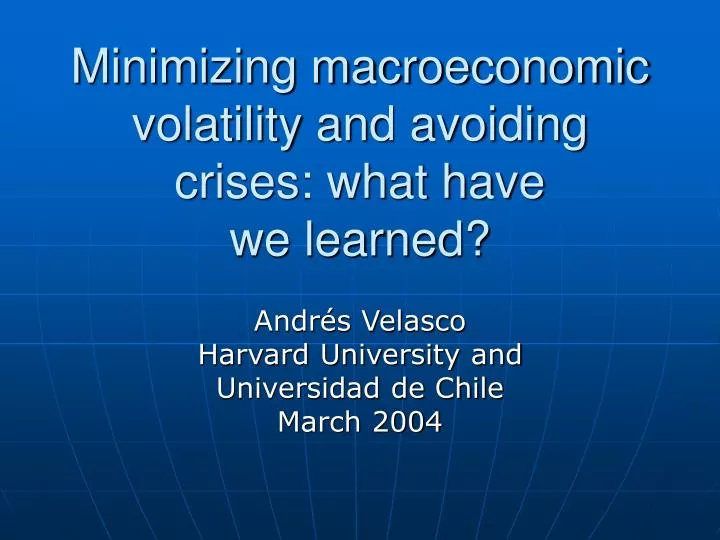

Minimizing macroeconomic volatility and avoiding crises: what have we learned?. Andrés Velasco Harvard University and Universidad de Chile March 2004. Fact of life: Latin America is volatile. Exogenous volatility: terms of trade, world interest rates, access to world capital markets

E N D

Minimizing macroeconomic volatility and avoiding crises: what have we learned? Andrés Velasco Harvard University and Universidad de Chile March 2004

Fact of life: Latin America is volatile • Exogenous volatility: terms of trade, world interest rates, access to world capital markets • Policy volatility: pro-cyclical fiscal and monetary policies • Volatile outcomes: output, consumption, investment, relative prices • Striking fact: real exchange rate is 3 times more volatile in LAC than in the OEDC

Fact of life: recurrent crises since 1980 Argentina (twice), Bolivia, Brazil (twice), Bulgaria, Chile, Colombia, the Czech Republic, Dominican Republic, Ecuador, Hungary, Indonesia, Korea, Malaysia, Mexico (twice), Panama, Pakistan, Philippines, Peru, Romania, Russia, Thailand, Turkey, Ukraine, Uruguay (twice) and Venezuela.

What’s new? • In the 1950s, 1960s and 1970s, LAC often suffered current account crises: lack of financing called for adjustment, cut in expenditure • Since 1980: mostly capital account crises • Larry Summers: 21st century crises • Great volatility of output and relative prices for countries that do not experience full-blown crises

LAC-7 Total Capital Flows (4 quarters, millions of US dollars and in % of GDP) Russian Crisis 100000 6% Post-Adjustment Period 5% 80000 4% % GDP (LAC-7 average) 3% 60000 2% 1% 40000 0% -1% 20000 -2% 0 -3% 1997-I 1998-I 1999-I 2000-I 2001-I 2002-I 2003-I 1997-III 1998-III 1999-III 2000-III 2003-III 2001-III 2002-III Includes Argentina, Brazil, Chile, Colombia, Mexico, Peru and Venezuela

What’s new about the new crises? • Not just fall in net new financing that calls for adjustment • Sudden stops cause capital accounts to reverse sign: much greater adjustment • Not just exchange rate crises: also debt crises and financial crises (banks) • Not just public sector crises: also private debts (Chile, Korea, Indonesia) and private deposits (Argentina, Uruguay, others) • Scarce liquidity paramount: Asia, Mexico • Crises contagious: post Asia, post Russia

What’s not fully understood about the new crises? • They blur the traditional distinction between liquidity and solvency. • Lack of liquidity causes costs: recession, devaluation, abandonment of projects • These costs then ensures solvency problems: low tax revenue, low corporate profits, large debts (when measured in domestic currency) • Expectations can become self-fulfilling and occurrence and timing of crises arbitrary

Moreover… you can suffer even if you do not have a full blown crisis • Classic example: Chile versus Australia in late 1990s • Even in best behaved countries: pro-cyclical capital flows, large current account adjustments • Result: pro-cyclical monetary and fiscal policies • Result: precautionary recessions (Caballero 2003)

Chile: current account reversal Current Account Deficit: 1990-2001 (% GDP)

Fiscal Surplus: 1990-2001 (% GDP) Chile: fiscal strength

What causes sudden stops, limited access to capital and crises?Moral failure against market failure • Unwillingness to pay • Sovereign risk • Moral hazard (bailouts, implicit guarantees) • Inability to pay • Unforeseen real shocks • Lack of liquidity • Mismatches

Implications of the moral hazard view • Capital flows to emerging markets should be large. But… they are small • Capital should flow from rich to poor. But… it is often the other way around • Flows should have increased after bailouts of 95-98. But… they fell • Capital should be skewed away from FDI and toward bonds and loans. But… it’s been the other way around

Conclusion Moral hazard “would imply that either emerging market policymakers deliberately brought their economies into painful maelstrom (in exchange, perhaps, for a brief mirage of affluence) or that they exhibited a fantastic lack of judgment, bordering on the insane. However, since there is no scientific evidence that those characteristics are the monopoly of emerging market policymakers, …the moral hazard view must … be classified as an intellectually appealing but unsubstantiated conjecture.” (Calvo 2001)

What is to be done? • What emerging market countries can do for themselves • Strengthening institutions / credibility • Improving monetary and exchange rate policy • Borrow less • Reducing mismatches and improving risk-sharing • What the world can do for emerging market countries • Providing liquidity • Rethinking crisis resolution • Reducing volatility of capital flows and EM asset prices • Help overcome thin markets and externalities

Strengthening institutions • Common place of the year: improve institutions • Obvious: better Chile and Singapore than many others • Problem: the Sweden syndrome • Question: how to do it? • Are their shortcuts? • Can macro policies help?

Tough rules ≠ strong institutions • Tough rules can lack credibility: currency boards • Credibility can be decreasing in the degree of toughness (Neut and Velasco, 2003) • The dagger in the wheel • With good institutions you do not need tough rules

Tough rules ≠ strong institutions • Example: independent central banks and inflation targeting • Example: Chile since the early 1990s • Better example: Brazil since 2002 • Constrained discretion (Bernanke and Mishkin, 1997) • Key: make the sausages but do not tell me how

Inflation and Inflation-Target Rates: 1990-2002 (% y-o-y) Chile: inflation targeting

What is to be done? • What emerging market countries can do for themselves • Strengthening institutions / credibility • Improving monetary and exchange rate policy • Borrow less? • Reducing mismatches and improving risk-sharing • What the world can do for emerging market countries • Providing liquidity • Rethinking crisis resolution • Reducing volatility of capital flows and EM asset prices • Help overcome thin markets and externalities

Can floating work? • Fashion is consolidated • Problem: fear of large real exchange rate volatility and mismatches • Problem: fear of floating, recent reserve accumulation • But give it time…

LAC-7: Exchange Rate & International Reserves Nominal & Real Exchange Rate Stock of International Reserves (vis-à-vis US dollar) (millions of US dollars) Post-Adjustment Period Post-Adjustment Period 195000 210 185000 190 +8% 175000 170 165000 Nominal exchange rate 150 +16% 155000 130 145000 110 135000 Real exchange rate 125000 90 Dic-98 Dic-99 Dic-00 Dic-01 Dic-02 Dic-03 Jun-98 Jun-99 Jun-00 Jun-01 Jun-02 Jun-03 Jun-99 Jun-00 Jun-03 Jun-98 Jun-01 Jun-02 Includes Argentina, Brazil, Chile, Colombia, Mexico, Peru, Venezuela

Nominal Exchange Rate and Flotation Band (pesos/dollar) Chile: fear of floating?

Can floating improve institutions? • It signals nascent fiscal imbalances (Tornell and Velasco 1997) • It can build support for central bank independence (Mishkin and Posen, 1997) • More generally: institutions operate better with some flexibility (prevent steam from building up)

What is to be done? • What emerging market countries can do for themselves • Strengthening institutions / credibility • Improving monetary and exchange rate policy • Borrow less? • Reducing mismatches and improving risk-sharing • What the world can do for emerging market countries • Providing liquidity • Rethinking crisis resolution • Reducing volatility of capital flows and EM asset prices • Help overcome thin markets and externalities

Borrow less? “Developing-country leaders need to realize that borrowing is like taking steroids: it gives countries a short-term performance boost but leads to insidious long-term problems. Look at the modern history of most Latin American countries.” Ken Rogoff, Newsweek International, February 16, 2004.

Emerging Markets Spreads & Domestic Interest Rates Emerging Markets Spreads Spreads & Domestic Interest Rates (EMBI+ adj. for Argentina, in bp) (domestic lending rates, June 1998=100) Russian Crisis Russian Crisis 155 1400 1400 135 1200 1200 115 1000 Spread ENRON effect 1000 EMBI+ adj. for Argentina 95 EMBI+ adj. for Argentina 800 Domestic lending rates 800 75 600 600 55 400 400 Pre- Russian Crisis Spread Interest Rates 200 35 200 Jun-97 Jun-98 Jun-99 Jun-00 Jun-01 Jun-02 Jun-03 Jun-97 Jun-98 Jun-99 Jun-00 Jun-01 Jun-02 Jun-03 Includes: Brazil, Chile, Colombia, Mexico, Peru & Venezuela

Borrow less? • Sure, some crises have been caused by over-borrowing, but… • Even with strong fiscal position sudden stops can happen • Sharp increases in Debt/GDP ratios often come from real devaluations • Why have it if you cannot use it (Rodrik, 1999) • Much of the borrowing done by the private sector. How to stop?

What is to be done? • What emerging market countries can do for themselves • Strengthening institutions / credibility • Improving monetary and exchange rate policy • Borrow less? • Reducing mismatches and improving risk-sharing • What the world can do for emerging market countries • Providing liquidity • Rethinking crisis resolution • Reducing volatility of capital flows and EM asset prices • Help overcome thin markets and externalities

Borrow better (1) • Key: the tale of raincoats and bathing suits • Avoiding crises: prevent mismatches • The Calvo et al measure: (B+eB*)/(Y+eY*) • First thing: borrow less in dollars • Second thing: open up the economy • Openness may also reduce movements in the real exchange rate, but not very much

Chile: real exchange rate Multilateral Real Exchange Rate 1986=100 120.00 110.00 100.00 90.00 80.00 70.00 60.00 Jul-97 Jan-95 Jul-02 Jul-92 Apr-96 Jan-90 Jan-00 Jun-90 Jun-95 Jun-00 Feb-92 Feb-97 Feb-02 Oct-93 Sep-96 Oct-98 Sep-01 Oct-03 Sep-91 Dec-92 Dec-97 Nov-90 Apr-91 Mar-94 Mar-99 Apr-01 Dec-02 May-03 May-93 Aug-94 Nov-95 May-98 Aug-99 Nov-00 Date All relevant currencies 5 most relevant currencies

Borrow better (2) • Key: better risk-sharing • Can we separate default risk from commodity or real exchange risk? • Who should bear commodity or real exchange risk? Can it be diversified? • Peso bonds? Indexed peso bonds? Commodity bonds (Frankel, 2002)? • Some progress: Czech Republic, Hungary, Singapore, Taiwan, Chile Mexico

What is to be done? • What emerging market countries can do for themselves • Strengthening institutions / credibility • Improving monetary and exchange rate policy • Borrow less? • Reducing mismatches and improving risk-sharing • What the world can do for emerging market countries • Providing liquidity • Rethinking crisis management • Reducing volatility of capital flows and EM asset prices • Help overcome thin markets and externalities

Providing liquidity • Liquidity crises require a net international provider of liquidity • The possibility of moral hazard does not invalidate this role • Does the IMF do this? • Size: total resources are 200 b., total sovereign debt market 290 b., many other kinds of claims • Speed: ex ante versus ex post conditionality • After the CCL, what? • Role of other IFIs

Crisis resolution • SDRM debate: a wrong turn, mostly • Sovereign bonds a small part of the problem • Bonds with CACS will help, but… • Need to think about broader concerted actions: coordinated rollovers, etc. • A role for capital controls?

What is to be done? • What emerging market countries can do for themselves • Strengthening institutions / credibility • Improving monetary and exchange rate policy • Borrow less? • Reducing mismatches and improving risk-sharing • What the world can do for emerging market countries • Providing liquidity • Rethinking crisis management • Reducing volatility of capital flows and EM asset prices • Help overcome thin markets and externalities

Filling in the missing markets • There is an externality in market creation: they need not spring up on their own • Example: Brady bonds • Role for IFIs in this • Lending to countries in their own currencies? • Lending in a basket EM currency? (Eichengreen and Hausmann)

Improving risk sharing and stabilizing asset prices • Emerging market bond fund (Calvo, 2003) • Emerging market collateralized debt obligations (Caballero, 2003) • An IFI role here as well

Do we need a new international effort to avoid and resolve crises? Gandhi: it would be a good idea