Download

1 / 5

50 likes | 105 Views

for more details visit http://www.jvvco.in/services.html for services related to accounting and taxation like chartered accountant in vapi, top ca firms in vapi, financial planning and advisory services in vapi, auditing services in vapi, service tax return filing services in vapi, financial planner in vapi, company law service in vapi, Business Restructuring Services in vapi, asset valuation service in vapi, income tax consultants in vapi

E N D

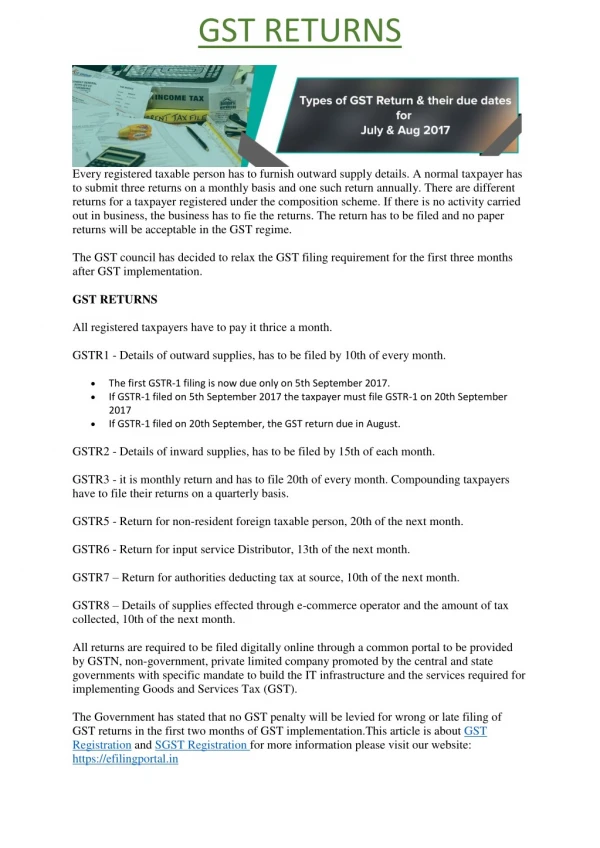

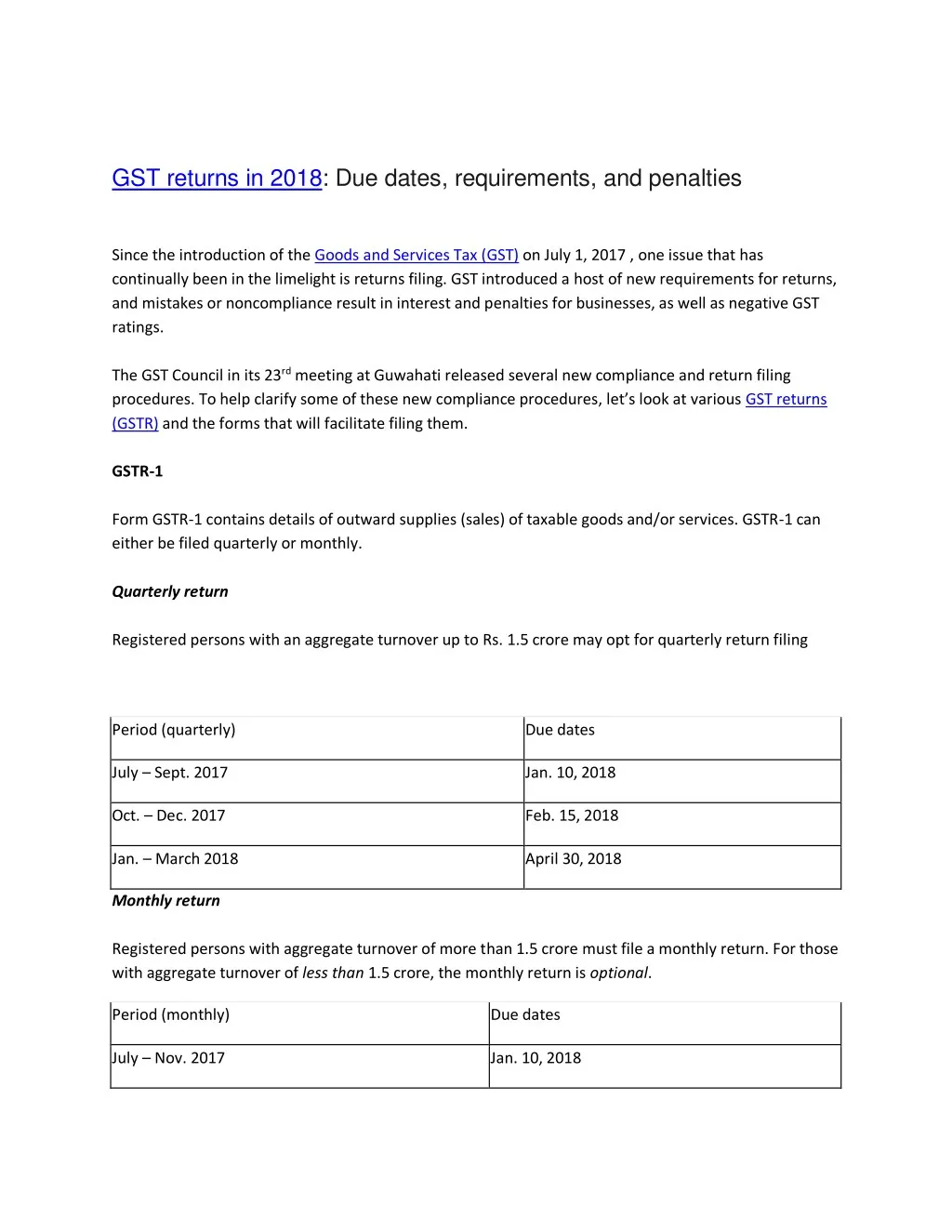

GST returns in 2018: Due dates, requirements, and penalties Since the introduction of the Goods and Services Tax (GST) on July 1, 2017 , one issue that has continually been in the limelight is returns filing. GST introduced a host of new requirements for returns, and mistakes or noncompliance result in interest and penalties for businesses, as well as negative GST ratings. The GST Council in its 23rd meeting at Guwahati released several new compliance and return filing procedures. To help clarify some of these new compliance procedures, let’s look at various GST returns (GSTR) and the forms that will facilitate filing them. GSTR-1 Form GSTR-1 contains details of outward supplies (sales) of taxable goods and/or services. GSTR-1 can either be filed quarterly or monthly. Quarterly return Registered persons with an aggregate turnover up to Rs. 1.5 crore may opt for quarterly return filing Period (quarterly) Due dates July – Sept. 2017 Jan. 10, 2018 Oct. – Dec. 2017 Feb. 15, 2018 Jan. – March 2018 April 30, 2018 Monthly return Registered persons with aggregate turnover of more than 1.5 crore must file a monthly return. For those with aggregate turnover of less than 1.5 crore, the monthly return is optional. Period (monthly) Due dates July – Nov. 2017 Jan. 10, 2018

Dec. 2017 Feb. 10, 2018 Jan. 2018 March 10, 2018 Feb. 2018 April 10, 2018 March 2018 May 10, 2018 Important considerations that need to be taken into account while filing GSTR-1 Businesses need to be careful to file correctly. This is especially important right now because there have been several due date extensions that require taxpayers to upload GST returns for multiple periods at once, and choosing the correct period is very important. Businesses need to be careful to avoid duplicating invoices. Further, it is important to correctly categories goods under the correct HSN codes and make sure to charge the correct tax rate. Mentioning the right tax type, i.e., CGST, SGST, IGST, is also important. Further, details of aggregate turnover in the previous year and a valid digital signature will also be required when filing GSTR-1. GSTR-2 and GSTR-3 For the time being, the GST Council has suspended the requirement to file forms GSTR-2 and GSTR-3. Filing is expected to resume after March 31, 2018. GSTR-2 will contain details of inward supplies (purchases) of taxable goods and/or services that affect the input tax credit (ITC) claimed. This form will need to be filed by the 15th of the following month. Form GSTR-2 will require the following details: Invoice-wise details of all interstate and intrastate supplies received from registered or unregistered persons Goods that have been imported and services rendered Debit and credit notes, if any, received from supplier Amount of ineligible ITC on inward supplies when the taxable status of the supplies could not be determined at the invoice level in form GSTR-2 GSTR-3, a monthly return, will finalize the details of outward and inward supplies and be sent along with payment of tax. The form must be filed by the 20th of the following month.

GSTR-3 is divided into two parts, i.e., part A and part B. Part A will be electronically generated based on information furnished in forms GSTR-1 and GSTR-2, as well as other liabilities of preceding tax periods Part B will contain the tax liability, interest, and penalty paid and refund claimed from a company’s cash ledger, if any. The system will compute the tax liability based on GSTR-1, minus any ITC claimed in GSTR-2 GSTR-3B All businesses are required to file a simple GST return in form GSTR-3B through March 2018. It is required to be filed by the 20th of the next month. Period (monthly) Due dates Dec. 2017 Jan. 20, 2018 Jan. 2018 Feb. 20, 2018 Feb. 2018 March 20, 2018 March 2018 April 20, 2018 GSTR-4 Composition dealers are required to file a quarterly GST return using form GSTR-4 by the 18th of the month following the quarter for which the return is being filed. Period (quarterly) Due dates July – Sept. 2017 Dec. 24, 2017 Oct. – Dec. 2017 Jan. 18, 2018 Jan. – March 2018 April 18, 2018 GSTR-5 GSTR-5 is a return for non-resident foreign taxable persons. This return is to be filed on a monthly basis by the 20th of the following month. The due date for the period July – Dec. 2017 is Jan 31, 2018.

GSTR-6 This return is for input service distributors. It is to be filed monthly by the 13th of the following month. At this point the GST portal has facilitated GSTR-6 filing only for the month of July 2017. Soon-to-be required returns GSTR-7: Applies to authorities deducting tax at the source. It will need to be filed on a monthly basis by the 10th of the following month. GSTR-8: To be filed by ecommerce operators on a monthly basis by the 10th of the next month. GSTR-9: Every dealer will need to furnish this annual return by 31 December after the end of the financial year. The first annual return under GST for the period April 2017 to March 2018 will need to be filed by Dec. 31, 2018. GSTR-10: To be filed only when a taxpayer’s registration is cancelled or surrendered, within three months after the cancellation. GSTR-11: This return is for UIN holders to report details of inward supplies to be furnished by a person having UIN and claiming a refund. It must be furnished by the 28th of the month following the month for which the statement is being filed. Late filing The GST Act mandates filing returns. In cases where there are no transactions for particular period, taxpayers will still need to file a nil GST return. Missed returns cannot be filed in a subsequent month or quarter. Therefore late filing will have a cascading effect leading to heavy fines and penalty. Pursuant to the GST Act, late fees of Rs. 100 per day per return will be levied on companies in cases of late filing. This means total late fees of Rs. 200 per day (100 under CGST and 100 under SGST), subject to a maximum of Rs. 5,000 for a particular period. There are no late fees for IGST returns. The GST Council has waived late fees for GSTR-3B for July, August, and September. Any late fees paid for these months will be credited back to the company’s electronic cash ledger under ‘Tax’ and can be utilized to make future GST payments. In addition, the GST Council reduced the fees for filing GSTR-3B and GSTR-4 returns after their due dates to: Rs. 50 per day of delay in normal cases

Rs. 20 per day of delay for taxpayers having nil tax liability for the month Interest on delayed tax payments is charged at 18 percent per annum on the amount of outstanding tax and is calculated from the day following the missed due date until the actual date of payment. Using GST compliance software can greatly assist businesses in filing returns accurately and on time. for more details visit http://www.jvvco.in/services.html for services related to accounting and taxation like chartered accountant in vapi, top ca firms in vapi, financial planning and advisory services in vapi, auditing services in vapi, service tax return filing services in vapi, financial planner in vapi, company law service in vapi, Business Restructuring Services in vapi, asset valuation service in vapi, income tax consultants in vapi