Download

1 / 14

140 likes | 250 Views

Maximizing Shareholder Value in Catastrophe Management. Session 10 Casualty Actuarial Society Catastrophe Issues Special Interest Seminar John Tedeschi ACAS, MAAA Senior Vice President Guy Carpenter & Co. 212-323-1629 JTEDESCHI@GUYCARP.E-MAIL.COM. Agenda.

E N D

Maximizing Shareholder Value in Catastrophe Management Session 10 Casualty Actuarial SocietyCatastrophe Issues Special Interest Seminar John Tedeschi ACAS, MAAA Senior Vice President Guy Carpenter & Co. 212-323-1629 JTEDESCHI@GUYCARP.E-MAIL.COM

Agenda • Review of how to measure catastrophe losses • What is included in a loss model • What’s not included in a loss model • How are companies measuring catastrophe losses as an impact to capital 2

Loss Modeling • Dynamic Financial Modeling requires • Catastrophe Per Occurrence Loss Distribution • Annual Frequency Assumptions • Time Horizon • Natural Disasters • Hurricane, Earthquake, Tornado, Winter Storm, Hail, Flood, Straight-line Wind, Volcano, Subsidence, Freeze, Flood, Brush Fire... 3

Loss Estimation Modeling • The most popular • AIR, EQECAT and RMS • Others • TOPCAT, REI, ARA • Definition of Loss Exceedance Curves can vary by modeler • example 4

Guy Carpenter & Company, Inc. CAS Catastrophe Issues Special Interest Seminar Loss Exceedance Curve 5

Guy Carpenter & Company, Inc. CAS Catastrophe Issues Special Interest Seminar Per Occurrence Exceedance Curve Example Event #1Event #2 Event #3 F1=0.04 F2=0.03 F3=0.01 PMF PMF PMF 0.6 0.55 0.7 0.2 0.15 0.1 0.2 0.3 0.2 10 30 70 20 40 90 30 60 130 Loss Loss Loss 6

Guy Carpenter & Company, Inc. CAS Catastrophe Issues Special Interest Seminar Per Occurrence Exceedance Curve Approach I Loss Freq. Prob. of Non-Exce 90 0.01 1.00 40 0.03 0.99 20 0.04 0.96 7

Guy Carpenter & Company, Inc. CAS Catastrophe Issues Special Interest Seminar Per Occurrence Exceedance Curve Approach II Loss Freq. Prob. of Non-Exce 130 0.001 1.00 90 0.007 0.999 70 0.002 0.992 600.00450.99 40 0.0165 0.9855 30 0.017 .969 20 0.024 0.952 10 0.008 0.928 8

What is included in loss model? • Class of Business • Auto Physical Damage • Inland Marine / Ocean Marine • Workers Compensation / General Liability • Unknown Locations • etc • Portions of Loss • Loss Adjustment Expense (ULAE and ALAE) • Business Interruption • Demand Surge/Debris Removal 9

What is included in loss model? • Loss Assessments • Involuntary Pools • Guaranty Funds • State Pools - eg FHCF, JUA • Other Losses that destroy equity • Reinsurance Reinstatement Premiums • Un-collectable Reinsurance (eg FHCF) • State Imposed Coverage 10

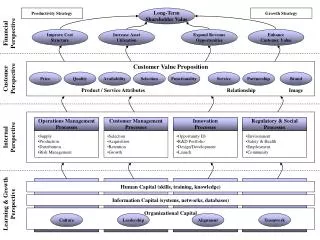

Metrics on Capital • Multiple Metrics are preferred • monitor single large catastrophe • monitor accumulation of many smaller cats • monitor varying time horizons • Total PML measured gross or net basis to: • Surplus • Earnings • Income 11

Example: S&P’s Catastrophe Methodology • Cat Recovery Ratio: • Net Expected Cat Exposure (NECE) to 3yr avg Pre-tax Income • Cat Exposure Ratio: • NECE to Surplus • Cat Liquidity Ratio: • NECE to Liquid Assets 12

S&P Benchmarks AAAAAABBB Cat Recovery Ratio: 0-1.0 0.5-2.5 2.0-5.0 4-6 Cat Exposure Ratio: 0-15% 10-35% 15-40% 30-60% Cat Liquidity Ratio: 0-10% 7.5-25% 20-50% 40-100% 13

Conclusion • Shareholder value should be measured from many perspectives and over multiple years. • DFA and other analysis can be used to measure the benefit of alternative financial strategies: • finite risk • equity options • cat bonds 14