Download

1 / 21

210 likes | 319 Views

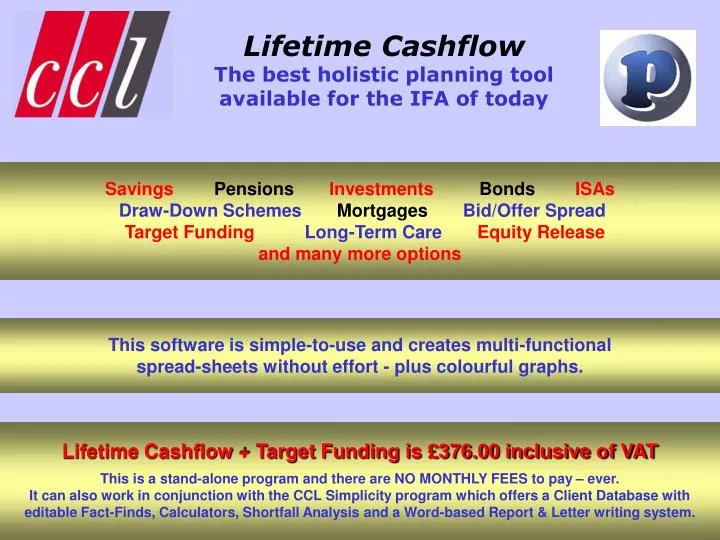

Lifetime Cashflow The best holistic planning tool available for the IFA of today. Savings Pensions Investments Bonds ISAs Draw-Down Schemes Mortgages Bid/Offer Spread Target Funding Long-Term Care Equity Release and many more options.

E N D

Lifetime Cashflow The best holistic planning toolavailable for the IFA of today SavingsPensionsInvestments Bonds ISAs Draw-Down Schemes Mortgages Bid/Offer Spread Target Funding Long-Term Care Equity Release and many more options This software is simple-to-use and creates multi-functional spread-sheets without effort - plus colourful graphs. Lifetime Cashflow + Target Funding is £376.00 inclusive of VAT This is a stand-alone program and there are NO MONTHLY FEES to pay – ever. It can also work in conjunction with the CCL Simplicity program which offers a Client Database with editable Fact-Finds, Calculators, Shortfall Analysis and a Word-based Report & Letter writing system.

Click or Space to Continue First we will set up the spread-sheet to show the period of the plan. Here we have entered by age from 43 to 95 years – the maximum range is 200 years.

Click or Space to Continue We have also personalised the plan with the client’s name and selected an appropriate growth rate. The growth rates are USER DEFINABLE so that you can change any or all of them at any time.

Click or Space to Continue We have now entered the current value of the client’s existing investments. If required, each item can have a descriptive note entered in the box in the bottom left of the screen.

Click or Space to Continue Current or future planned investment levels can now be entered in the Annual or Monthly columns. You can also index these at any annual rate chosen by the client or advised by the IFA. Here we have indexed at 4% (See Note)

Click or Space to Continue Levels of investment or even the scale of indexation can be changed at any time. Here we see an increase to the investment following the repayment of the mortgage (see the Notes panel).

Click or Space to Continue You can also take an “investment holiday” or cease investment completely at any time. Here we show that the client wishes to make no further savings after retirement age.

Click or Space to Continue Single investments or one-off draw downs of funds can also be entered. Here we see that the clients are planning to move to a smaller property after the children leave home. Or they may be planning to buy a property abroad.

Click or Space to Continue You can either enter the amount of income the clients want (indexed if required) and see when the money runs out or, as here, enter a percentage to draw from the fund to see what they can safely take as income. You could also enter an annuity rate.

Click or Space to Continue Here we have scrolled down to the bottom of the plan to see what happens if the client requires a pension of £25,000 pa on retirement indexed at 5% each year. Note the shortfall from 82 onwards.

Click or Space to Continue If preferred, you can also display and plane as a graphical representation of the same situation. This can often be a simpler way of showing a client that a plan does (or doesn’t) work. You can even change the growth rate while the graph is on the screen.

Click or Space to Continue We have now inserted the anticipated Tax-Free Lump Sum from the client’s occupational pension. Any number of single, annual or monthly payments can be added to each plan.

Click or Space to Continue On the above screen, we have added the assessed annual State Pension entitlement calculated by Simplicity and added this to the plan, using the client’s view of how much this increases each year (here it is 1.5%).

Click or Space to Continue These additions also make a major difference to the Graph which you can click onto using the button at the top left of the screen and then, just as easily, click back to the Spreadsheet.

Click or Space to Continue Having saved the previous plan, we have now set-up a one-screen scenario for a 32 year old retiring at 65 to assess his pension fund. The pension plan has a £200 pm contribution, less 5% B/O spread, indexed at 4% pa with a 1% management charge. SO SIMPLE!!!

Click or Space to Continue TARGET FUNDING OPTION - The clients have stated that, at the age of 65, they would like to have a fund of £500,000. Assuming that money devalues at 2% pa, what monthly saving is required in each year, assuming a 4% pa indexation of the amount saved?

Click or Space to Continue Target Funding has now worked out what fund is required in 33 years to be the equivalent of £500,000 today and the level of monthly savings needed today and in each year up to 65 years old to achieve this Target Fund.

Click or Space to Continue However, if the client incorporates his current investments in the plan by inserting the value, as above, this will immediately reduce the amount of monthly savings required today and in each year up to 65.

Click or Space to Continue And above, we have also inserted the anticipated Tax-Free Lump Sum from the client’s occupational pension. This further reduces the amount of monthly contributions required to reach the Target Fund.

Lifetime CashflowThe best holistic planning toolavailable for the IFA of today Lifetime Cashflow + Target Funding is £376.00 inclusive of VAT This is a stand-alone program and there are NO MONTHLY FEES to pay - ever. It can also work in conjunction with the CCL Simplicity program which offers a Client Database with editable Fact-Finds, Calculators, Shortfall Analysis and a Word-based Report & Letter writing system. CCL Software Limited Battenhall Lodge, 60 Battenhall Road, Worcester, WR5 2BX FreePhone: 0800 0199 853 Email Address: info@ccl-uk.com Sales Desk: 01905 356660 Web Site: www.ccl-uk.com