Download

1 / 8

80 likes | 176 Views

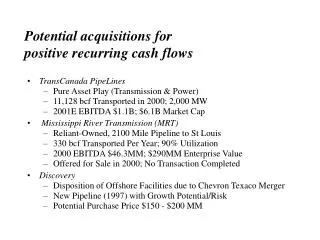

Potential acquisitions for positive recurring cash flows. TransCanada PipeLines Pure Asset Play (Transmission & Pipes) 2001E EBITDA $1.1B; $6.1B Market Cap Mississippi River Transmission (MRT) Reliant-Owned, 2100 Mile Pipeline to St Louis 330 bcf Transported Per Year; 90% Utilization

E N D

Potential acquisitions for positive recurring cash flows • TransCanada PipeLines • Pure Asset Play (Transmission & Pipes) • 2001E EBITDA $1.1B; $6.1B Market Cap • Mississippi River Transmission (MRT) • Reliant-Owned, 2100 Mile Pipeline to St Louis • 330 bcf Transported Per Year; 90% Utilization • 2000 EBITDA $46.3MM; $290MM Enterprise Value • Offered for Sale in 2000; No Transaction Completed • Discovery • Disposition of Offshore Facilities due to Chevron Texaco Merger • Auction Process Commencing in November • New Pipeline (1997) with Growth Potential/Risk

Dispositions of non-strategic assets • Trailblazer Pipeline • Potential Sale to EOTT or NBP • Target Gain: $38MM • Beaver • Potential Sale of NNG Transmission/Field Assets • Duke Expression of Interest • Target Gain: $20MM • MOPS • Disposition of NNG Offshore Facilities • $13.0 Million Williams Offer Accepted; PSA Near Completion • Close Subject to FERC Approval; 6-9 Mos.

Alaska Highway Pipeline$500 million • Rejoin the Alaska Northwest Natural Gas Transportation Company (ANNGTC) with a minority interest of 9.4 percent. Other participants include TCPL, Foothills, PG&E, DUK, EPNG, SEM, NiS, and WMB. • Pursuant to ANGTA, ANNGTC was authorized to develop, build, own, and operate a new 745 mile pipeline capable of transporting up to 4 bcf/d of gas from the Alaskan North Slope to the Alaska/Canada border for ultimate delivery to markets in Canada and the lower 48 states of the US (“Alaska Highway Pipeline”). • Project rationale: recognize 26 MM gain resulting from re-instatement of historic capital contributions previously written off by Northern Arctic Gas Company (“NAGC”), an Enron affiliate; participate in distributions from the ANNGTC Partnership following successful completion of the pipeline. • Principle risks: allowed rate of return, ANS Producer support, emergence of competing projects, historic residual contingent liabilities. • Status: MOU imminent; commercial proposal for ANS Producers in 4Q-01; restated Project Agreements in 1Q-02; commercial operations in 2007.

TransPecos$xxx million • Form a 50/50 joint venture with KMI to develop, build, own, and operate a new xxx mile, yy bcf/d pipeline across the Texas panhandle. The project provides PEMEX with diversification in gas supplies (access to NNG, NGPL, TW, and EPNG). • Opportunity to earn positive cash flows, attractive equity returns. Upsides associated with increased throughputs on NNG and TW. • Principle risks: PEMEX credit concentration, competition in the market area with EPNG. • LOI signed between TW and KMI; commercial proposal tendered to PEMEX; A+ cost estimates completed; PEMEX discussions ongoing; FERC application in [2Q02]; commercial service [???].

Sun Devil Project$680 million • Develop new facilities on Transwestern to transport 0.5 bcf/d of natural gas from San Juan to power generators in Phoenix. • Project rationale: earn positive operating cash flows, attractive ROE. • Principle risks: SJ – Permian, SJ – Cal Border gas price spreads; competition from KMI’s Sonoran Pipeline in the supply area; competition from EPNG in the market area. • Open season closed August 30 – 1.3 Bcf/d in bids received; A+ estimates completed; currently negotiating commercial commitments with anchor shippers; FERC application to be filed in 2Q-2; commercial service in 2nd half 2004.

Transwestern Sta 1 Heat Recovery$20 million • Form a non-regulated affiliate to develop, build, own and operate a 15 MW power plant at Tranwestern’s Compressor Station No. 1 using waste heat exhausted from the new combustion turbine placed in service under the Redrock expansion. • Project rationale: earn positive operating cash flows, attractive ROE; test case for comparable projects at other locations (FGT, NNG). • Principle risk: volatile power prices • Seeking long term power sales with Mohave Electric Co-op, ENA West Desk

Preliminary analysis Gas consumption in the Southeast is expected to grow primarily to serve gas-fired electricity generation Southeast gas markets are underserved, resulting in higher delivered prices. Gas supply from the Gulf coast is forecast to peak by 2005 LNG imports may be needed to fill the gap in gas supply Gulfstream and Gulf Pines are new competition to established gas pipeline providers Potential prospects Assess the value of Gulf Pines pipeline as an extension of FGT. Assess the value of Cypress as an extension of FGT into Georgia and possibly further into the Carolinas. Assess the value of Koch Gateway as a possible acquisition to enhance FGT gathering and to supply Gulfstream. Design a grassroots pipeline to compete with Gulf Pines. Southeast region

Preliminary analysis Growth in gas demand is driven by construction of new gas-fired power plants, which are displacing older, less efficient facilities. Re-alignment of regional bulk power transfers obscures growth patterns in gas markets. Traditional supply basins (Rocky Mtns, San Juan, Canada) will serve new growth. Growing dependence on Canadian and Alaskan resources. California: excess facilities to serve core markets; capacity releases, by-pass pipelines, and private storage to serve non-core; pent-up demand for by-pass regulatory reforms. Potential prospects Assess acquisition of PGT to access Alaskan and Canadian gas supplies and markets in the Pacific Northwest. Assess acquisition of Tuscarora and Paiute to access major cities in Nevada and provide a gateway to central California. Explore joint venture possibilities with CIG in constructing the Ruby Pipeline to- connect with the Paiute System in northern Nevada extend to the Wild Goose storage facility in the Bay Area access low cost, abundant Rocky Mountain Gas Supplies. Western region