Download

1 / 14

150 likes | 419 Views

Swaps Chapter 26. Financial Institutions Management, 3/e By Anthony Saunders. Introduction. Market for swaps has grown enormously Serious regulatory concerns regarding credit risk exposures Motivated BIS risk-based capital reforms

E N D

SwapsChapter 26 Financial Institutions Management, 3/e By Anthony Saunders

Introduction • Market for swaps has grown enormously • Serious regulatory concerns regarding credit risk exposures • Motivated BIS risk-based capital reforms • Growth in exotic swaps such as inverse floater generated controversy (e.g., Orange County, CA). • Generic swaps in order of quantitative importance: interest rate, currency, commodity.

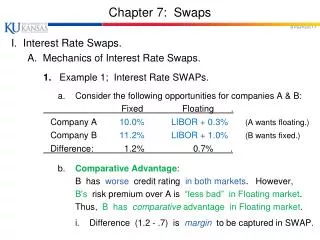

Interest Rate Swaps • Interest rate swap as succession of forwards. • Swap buyer agrees to pay fixed-rate • Swap seller agrees to pay floating-rate. • Purpose of swap • Allows FIs to economically convert variable-rate instruments into fixed-rate (or vice versa) in order to better match assets and liabilities.

Interest Rate Swap Example • Consider money center bank that has raised $100 million by issuing 4-year notes with 10% fixed coupons. On asset side: C&I loans linked to LIBOR. Duration gap is negative. DA - kDL < 0 • Second party is savings bank with $100 million in fixed-rate mortgages of long duration funded with CDs having duration of 1 year. DA - kDL > 0

Example (continued) • Savings bank can reduce duration gap by buying a swap (taking fixed-payment side). • Notional value of the swap is $100 million. • Maturity is 4 years with 10% fixed-payments. • Suppose that LIBOR currently equals 8% and bank agrees to pay LIBOR + 2%.

Realized Cash Flows on Swap • Suppose realized rates are as follows End of Year LIBOR 1 9% 2 9% 3 7% 4 6%

Swap Payments End of LIBOR MCB Savings Year + 2% Payment Bank Net 1 11% $11 $10 +1 2 11 11 10 +1 3 9 9 10 - 1 4 8 810- 2 Total 39 40 - 1

Off-market Swaps • Swaps can be molded to suit needs • Special interest terms • Varying notional value • Increasing or decreasing over life of swap. • Structured-note inverse floater • Example: Government agency issues note with coupon equal to 7 percent minus LIBOR and converts it into a LIBOR liability through a swap.

Macrohedging with Swaps • Assume a thrift has positive gap such that DE = -(DA - kDL)A [DR/(1+R)] >0 if rates rise. Suppose choose to hedge with 10-year swaps. Fixed-rate payments are equivalent to payments on a 10-year T-bond. Floating-rate payments repriced to LIBOR every year. Changes in swap value DS, depend on duration difference (D10 - D1). DS = -(DFixed - DFloat) × NS × [DR/(1+R)]

Macrohedging (continued) • Optimal notional value requires DS = DE -(DFixed - DFloat) × NS × [DR/(1+R)] = -(DA - kDL) × A × [DR/(1+R)] NS = [(DA - kDL) × A]/(DFixed - DFloat)

Pricing an Interest Rate Swap • Example: • Assume 4-year swap with fixed payments at end of year. • We derive expected one-year rates from the yield curve treating the individual payments as separate zero-coupon bonds and iterating forward.

Currency Swaps • Fixed-Fixed • Example: U.S. bank with fixed-rate assets denominated in dollars, partly financed with £50 million in 4-year 10 percent (fixed) notes. By comparison, U.K. bank has assets partly funded by $100 million 4-year 10 percent notes. • Solution: Enter into currency swap. • Fixed-Floating currency swaps.

Credit Swaps • Credit swaps designed to hedge credit risk. • Total return swap • Pure credit swap • Interest-rate sensitive element stripped out leaving only the credit risk.

Credit Risk Concerns • Credit risk concerns partly mitigated by netting of swap payments. • Netting by novation • When there are many contracts between parties. • Payment flows are interest and not principal. • Standby letters of credit may be required.