Download

1 / 15

150 likes | 238 Views

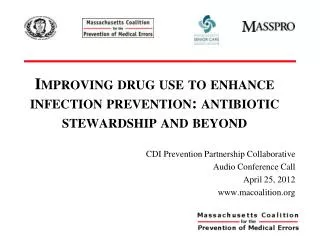

TELE NORTE LESTE PARTICIPAÇÕES S.A. Conference Call 2001, 4 th Quarter. Utilization Rate (%). 92%. 92%. 89%. 82%. 1998. 1999. 2000. 2001. Plant Growth. 5.3. 18.1. 3.0. 14.8. 12.8. 11.8. 10.5. 9.7. 8.8. 7.8. Lines in Service. Lines Installed. (in millions). 1998. 1999.

E N D

TELE NORTE LESTE PARTICIPAÇÕES S.A. Conference Call 2001, 4th Quarter

Utilization Rate (%) 92% 92% 89% 82% 1998 1999 2000 2001 Plant Growth 5.3 18.1 3.0 14.8 12.8 11.8 10.5 9.7 8.8 7.8 Lines in Service Lines Installed (in millions) 1998 1999 2000 2001 Slide 1

Line Blockage and Disconnections Disconnected Lines (in thousands) Blocked Lines (in thousands)* 900 9.5% 2001= 2,288 767 8.5% 1,500 8.1% 6.4% 636 1,187 1,185 1,152 600 945 1,000 472 413 300 500 0 0 Mar-01 Jun-01 Sep-01 Dec-01 1Q01 2Q01 3Q01 4Q01 Partial Total % of Total Lines in Service * End of Period Slide 2

Gross Revenue (R$ Million) CAGR (2001/98) 25.3% +97% (98/01) Slide 3

Operating Expenses Breakdown (R$ Million) 1,528 1,266 825 710 % 4,328 10 2,977 17 2,774 2,460 19 % 32 25 33 27 34 21 30 51 40 33 38 -10 Slide 4

Bad Debt Provision (R$ Million) Slide 5

CAPEX Evolution (R$ Billion) Slide 6

Consolidated Income Statement Plant Growth Anatel Targets Bad Debt Provisions for Contingencies F-M Traffic Growth Debt increase Slide 7

Capex 10.1 2.8 2.5 2.5 2.2 1998 1999 2000 2001 2002 2002 OUTLOOK CAPEX Reduction (R$ Bi) 2001 10.1 R$ bi 2002 2.5 R$ bi Wireline Business Wireless Business Slide 8

Lines in Service by year end 14.8 11.8 9.7 7.8 1998 1999 2000 2001 2002 2002 OUTLOOK Revenue Drivers - 1. Platform Expansion (mn) Average Lines in Service 15.5/15.6 13.6 10.6 8.6 7.2 1998 1999 2000 2001 2002 Slide 9

2002 OUTLOOK Cost Drivers • Headcount Reduction - 40% in average 3rd Party services - LIS reduction Bad debt control - lower than 5% of Gross RevenueMarketing expenses• wireline (30% reduction)•wireless (as partially investment)Interconnection• Renegotiation under new environment (SMP) Slide 10

Debt Structure – December 2001 (R$ mn) LT DEBT 2002 14% 2006 and beyond 2003 36% 17% 2004 ST 1,388 16% Cash 1,234 2005 17% • DEBT PROFILE • R$ 5,382 million foreign currency (60%)*: • LIBOR +/- 7% p.a. • R$ 3,556 million in Brazilian currency (40%): • (+/- 17% p.a.) Net Debt 7,705 Long Term 7,549 TOTAL = 8,938 * Fully Hedged Slide 11

2002 OUTLOOK TNL - PCS “ TNL - PCS “ Oi Oi ” ” ð Apr /02 - Ready to Launch ð 6 Metropolitans Areas - 120 cities ð Main suppliers: Nokia, Alcatel, Siemens ð Technology GSM/GPRS Target (12 months) 500.000 Subs ð Operating Agreements Infrastructure Co- siting Interconnection Roaming ð Operating Synergies Billing & Credit Infrastructure & BackOffice Data Base Slide 12

“SAFE HARBOR” STATEMENT This presentation contains forward-looking statements. Statements that are not historical facts, including statements about our beliefs and expectations, are forward-looking statements and involve inherent risks and uncertainties. These statements are based on current plans, estimates and projections, and therefore you should not place undue reliance on them. Forward-looking statements speak only as of the date they are made, and we undertake no obligation to update publicly any of them in light of new information or future events.

Investor Relations New Adress Rua Humberto de Campos, 425 / 8º andar Leblon Rio de Janeiro -RJ Phone: ( 55 21) 3131-1314/1315/1313 Fax: (55 21) 3131-1325/ 3131-1326 E-mail: invest@telemar.com.br Visit our new website: http://www.telemar.com.br/ri