Download

1 / 25

250 likes | 255 Views

Join Anil Chadha & Co. and Soubhagya Consultancy Services for an interactive session on GST. Learn about the latest updates, challenges, and opportunities related to GST implementation. Gain insights from industry experts and get customized solutions for your business. Don't miss out on this informative event!

E N D

India Convention Promotion BureauINTERACTIVE SESSION ON GST25 April 2019 Anil Chadha & Co Soubhagya

The Firm Anil Chadha & Co Arjun Chadha & Co Soubhagya Consultancy Services Pvt Ltd Chadha Mangla & Co

Anil Chadha & Co – Background • Integrated consultancy firm specializing in providing bespoke Tax & Transaction Advisory solutions • Founded by Anil Chadha, one of India’s senior-most chartered accountants, in 1976 and has vast experience in the realms of Tax, Transactions, Investment Structuring and Corporate Finance • The firm’s USP is its ability to offer end-to-end solutions under one roof, which eliminates the need for clients to separately interact with lawyers, banks and financiers, valuers, tax consultants and auditors • Over the past 4+ decades, the firm has advised Indian clients across all sectors including, • Automotive • Construction and real estate • Information technology and software exports • FMCG and trading • Financial services • The firm has also extensive experience in structuring cross-border investments across international jurisdictions, with numerous clients based out of the United States, United Kingdom and East Africa • Further, in tandem with its overseas affiliates, we have the requisite expertise in managing investments made by Indian investors in overseas jurisdictions

The Firm360o Approach In-house research and international affiliates External Resources Corporate Finance, PE and VC advisory Execution team Business consulting and IT Tax & regulatory Transaction structuring Assurance Industryexperts Customized solutions • Multi-dimensional teams combining the functional expertise & experience of individuals with specialized skill base in various sectors • 360o suite of financial services • Account Leader for each client – Operates as the single point of contact • Industry specialists – In-depth knowledge of practical issues and solutions

Arjun Chadha Arjun Chadha Partner – Tax and Regulatory Services Anil Chadha & Co, Chartered Accountants, New Delhi Email: Arjun@chadhaco.in Phone: +91 11 49873821 | +91 98116 62221 • Key Technical Experience (other than GST) • Advised on tax implications of setting up and operation of large manufacturing facilities • Advised non-resident developers of a large real estate venture in Delhi on optimum investment vehicles and repatriation of funds • Assisted a number of infrastructure and telecom companies in submission of bids • Conducted due diligences on corporates in case of buy-side and sell-side transactions • Comprehensive tax health checks from compliance and structuring perspectives • Ltigationupto Tribunal level as arguing counsel • Retained counsel on tax matters for a number of large corporates (Action Shoes, Federal Mogul Group, Anand Automotive Group, MandoAutomotive India, Dana Automotive, Henkel India, Bliss GVS Pharma, Savvy Investors Group - KensvilleGolf Resort, Gujarat) • GST Experience • GST transition and implementation • Re-structuring of operations and transaction structures and identifying opportunities to rationalise costs • Review of contracts and cost build-ups to optimise GST liability • Re-structuring of purchase contracts with a view to maximize input tax credit • On-going advisory and compliance • GST support to MSME vendors of large manufacturers • Advance rulings • Advise on and structuring of specific transactions to optimise the GST liability e.g. mergers, slump sale, transfer of majority shareholding, inter-state and cross-border transactions etc. Arjun is a Partner with the Tax and Regulatory Services division of the firm and has over 10 years of experience in indirect and direct tax consulting. Qualified as a Chartered Accountant in 2009. Consultant - Ernst & Young India (tax division) for 3 years. Arjun is a tax expert and has represented large real estate, automotive and manufacturing entities before tax authorities at various levels. He has advised several large multinational and Indian corporates on various tax matters, such as GST transition and implementation, GST impact assessment studies, domestic and cross-border transaction structuring, supply chain review, contract review, litigation support, bid submission, due diligence and health checks.

GST & MICE Open Issues

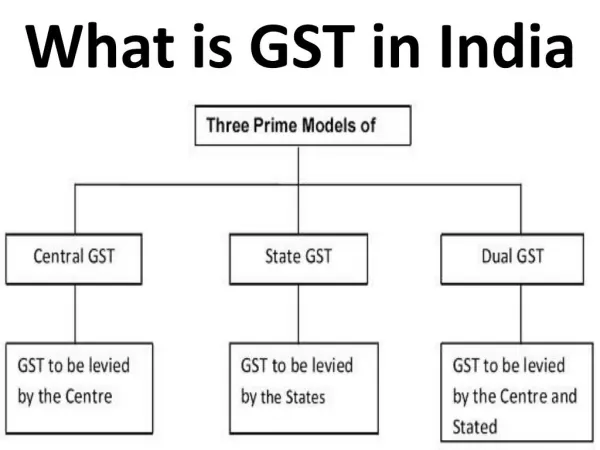

Place of Supply Rules • GST is a destination-based tax, i.e., the goods/services will be taxed at the place where they are consumed and not at the origin. • The state where they are consumed will have the right to collect GST • This makes the concept of ‘Place of Supply’ crucial • Standard provisions: • Place of supply is the location of the recipient • If recipient is unregistered and location is not available, place of supply is the location of the service provider

Input tax credit • IGST can be set-off against IGST – even if place of supply is different • One state local CGST & SGST cannot be set-off against another state’s local CGST & SGST • Issue in travel industry because of anomaly in PoS Rules • Even within the same state, CGST and SGST cannot be set-off against each other • New provision: • IGST credit has to be set-off against IGST, CGST and SGST liability • CGST credit can be used to pay CGST only after IGST credit has been exhausted • SGST credit can be used to pay SGST only after IGST credit has been exhausted

Input tax credit - misconceptions • Credit can be availed if I give my GSTIN to supplier • I can avail credit of previous months at any time in the future • Can be availed only up to 30th September after the end of the FY • For FY 2017-18 – 31st March 2019 • Credit can be availed if amount is reflecting in my GSTR-2A • Credit can be claimed in Delhi even if PoS of purchases is outside Delhi • May be eligible in case of IGST • Never eligible in case of another state’s CGST & SGST

ITC matching • Filing of GSTR-2 is not mandatory as of now • GSTR-2A is being auto-filled based on GSTR-1 filed by vendors • If suppliers are not filing returns correctly, credit will not reflect in GSTR-2A • GST department – notices for mismatch • GSTR-2A to be reconciled with purchase ledger and invoices • All credit in GSTR-2A is not automatically eligible – check restrictions • Corrective action – vendors should rectify or file their returns

GST on reimbursable expenses • Normally all reimbursable and incidental expenses are included in Value of Supply • Exclusion of reimbursable expenses – Pure Agent • Contractual agreement with the client to incur expenditure in the course of supply of goods or services • Does not hold any title to the goods or services procured • Does not use the supplies for his own interest • Receives only the actual amount incurred • Makes payment to the third party on authorization by the client • Payment made on behalf of the client has been separately indicated in the invoice • Charges additional amount for the services he supplies on his own account

GSTR – 9 & 9C • GSTR-9 to be filed by all regular assessees • GSTR-9C is an additional requirement – turnover over Rs 2 crore • GST audit to be done by a CA or CMA • Audited financial statements to be attached • Due date – 30th June 2019 • Insert forms

GST Amendment Act – w.e.f. 1st February 2019 • Place of business – The concept of business verticals for separate registrations has been done away with. Now, assessees will be able to obtain multiple registrations in the same State for separate places of business, which was previously possible only for separate business verticals. • Reverse charge - • Will be applicable only on specified purchases by registered persons from unregistered suppliers • Deleted – Earlier provision that was applicable for all purchases from unregistered suppliers • Deleted – Rs 5,000/- daily limit for exemption • Specified items have not been notified as yet • Input tax credit –discussed • Change in credit utilization method • Change in blocked credit items

GST Amendment Act – w.e.f. 1st February 2019 • Reverse charge - • Will be applicable only on specified purchases by registered persons from unregistered suppliers • Deleted – Earlier provision that was applicable for all purchases from unregistered suppliers • Deleted – Rs 5,000/- daily limit for exemption • Specified items have not been notified as yet • Input tax credit – discussed • Change in credit utilization method • Change in blocked credit items • Place of business – • Deleted – separate business verticals for separate registrations • Inserted – Multiple registrations in the same State for separate places of business • Debit notes and Credit notes – • Deleted – Linking each debit/ credit note to a single invoice • Inserted – Can issue single debit/credit note against multiple invoices issued in a FY

GST Amendment Act – w.e.f. 1st February 2019 • New return formats will be issued w.e.f. 1st June 2019 • Quarterly return for medium and large assessees • Annual return for small assessees • Tax payment will be monthly • Matching of ITC will be effective • Export of Services • The amendment allows to avail export benefits is services are provided to persons located in Nepal & Bhutan and consideration is received in INR • Import of Services • An entity, even though not registered under GST, if receives services from their related parties located outside India, in course or furtherance of business, falls under the ambit of GST • Recovery of tax • Dues of one state can be recovered from unit of the same person in another state

Changes effective from 1st April 2019 • Threshold exemption limit increased to Rs 40 lakhs • Only available for intra-state suppliers of goods • Not applicable for services – limit is still Rs 20 lakhs • Limit for special category states (HP, Uttarakhand, NE states) – Rs 20 lakhs • Composition scheme • Limit increased from Rs 1 crore to Rs 1.50 crore • Traders and manufacturers can provide services also – upto 5 lacs or 10% of turnover, whichever is less • Composition scheme for service providers – 6% uptoRs 50 lakhs – inter-state supplies not allowed • Real Estate Sector – option to pay tax @ 1% or 5% without ITC

474 DS, New Rajendra Nagar, New Delhi – 110060 • Phone: +91 11 28742482 | +91 11 49873821 • Mail: Arjun@chadhaco.in