Download

1 / 13

130 likes | 232 Views

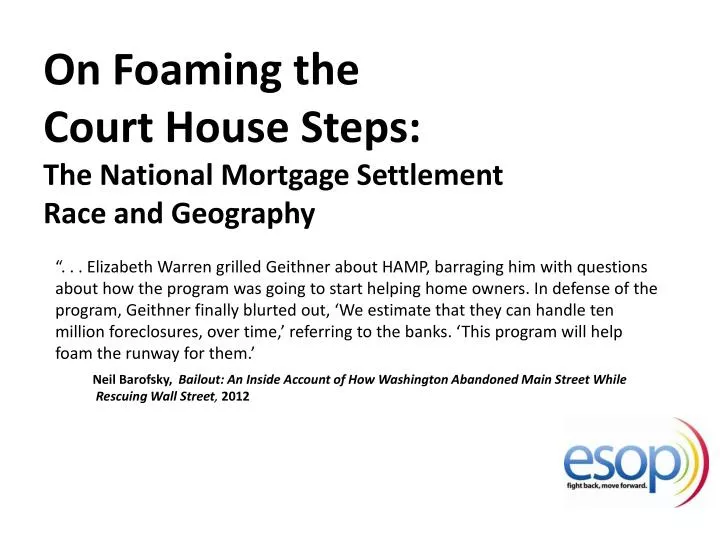

On Foaming the Court House Steps: The National Mortgage Settlement Race and Geography.

E N D

On Foaming the Court House Steps: The National Mortgage SettlementRace and Geography “. . . Elizabeth Warren grilled Geithner about HAMP, barraging him with questions about how the program was going to start helping home owners. In defense of the program, Geithner finally blurted out, ‘We estimate that they can handle ten million foreclosures, over time,’ referring to the banks. ‘This program will help foam the runway for them.’ Neil Barofsky, Bailout: An Inside Account of How Washington Abandoned Main Street While Rescuing Wall Street, 2012

This graphic captures why the (mal)Distribution of the NMS Consumer Relief can’t be helpfully measured by dollar totals. Costal home values distort the allocations. The only fair measure is the number of borrowers who obtained relief in each state.

“At-Risk” homeowners uses the April 2013, LPS Mortgage Monitor report of delinquency and pending foreclosure rates, broken out by state. That percentage was then multiplied by the “corrected” state-level, pending mortgage tally included in the Mortgage Bankers’ 3Q12 National Delinquency Survey. The resulting number is a rough take on how many homeowners in each state are “seriously delinquent” or in the parlance of LPS, “non-current.” To arrive at the percentages in the chart above, I took the total number of borrowers who obtained Consumer Relief, by state, in the most recent NMS Monitor’s Report (March 2013) and divided it by each state’s total of At-Risk borrowers.

This graph converts the calculations from the previous slide into a number of homeowners who did, and did not, obtain relief under the NMS. “0” on the vertical axis would mean that the number of borrower recipients under the NMS, as of March of 2013, correlates to the number of at-risk borrowers in each state, assuming that the NMS were distributed to each state in proportion to it’s share of at-risk homeowners nationally. By this estimate, while Ohio borrowers totaled 9,593 if there was parity there would be an additional 12,379 consumer relief recipients.

Criminal offenses against public justice of staggering and unknown proportions • To get back to the conduct that created the liability supporting the final NMS Consent Decree, servicers, trustees, lawyers, default services providers, and the banks that housed and/or funded the foregoing parties, orchestrated an historically unprecedented wave of crimes against public justice in the state and federal courts, in order to mislead judges, magistrates, trustees, land records clerks, homeowners andthe public. These crimes included: • Conspiracy to commit forgery and forgery of lost notes and mortgage assignments in the form of legally baseless wholly “reconstructed” documents. • Conspiracy to commit forgery and forgery of note “allonges” intended to mislead homeowners and the courts into believing that the foreclosing entity was legally entitled to pursue a forfeiture.

There were uncountable instances of: • Suborning perjury and perjury by written, sworn and notarized affidavits asserting facts unknown to the corporate affiant intended to persuade a court to order a legally baseless forfeiture and sale of a mortgaged home. • Conspiracy to commit misrepresentation and impersonation, and misrepresentation and impersonation and signature forgery by the foreclosing parties (and their vendors) asserting an elevated legal status and authority within the involved lender-corporation(s). These fictitious “Linda Green” events happened hundreds of thousands of times while servicers and their vendors prosecuted foreclosures across the country.