Download

1 / 30

300 likes | 384 Views

Lecture 7. Intermediate Targets, Money Supply or Interest rates?. Examine the problems related to the pegging of the rate of interest Examine Friedman’s argument in the context of adaptive expectations.

E N D

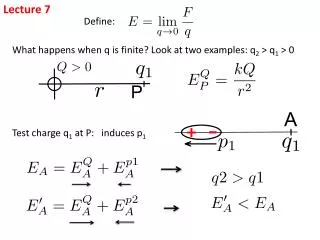

Lecture 7 Intermediate Targets, Money Supply or Interest rates?

Examine the problems related to the pegging of the rate of interest • Examine Friedman’s argument in the context of adaptive expectations. • Confirm the Sargent- Wallace finding for the instability of an interest rate peg with rational expectations • Show that an interest rate target is feasible under RE

The Friedman critique of interest rate pegging • Friedman showed that pegging the rate of interest leads to instability of inflation and output • The argument owes a lot to Thornton (1806) and Wicksell • A positive real shock can lead to accelerating inflation and above capacity growth.

The model • Let m = money, y = output, r = real rate of interest, R = nominal rate of interest and = rate of inflation (e = expected inflation) • R = r + e • Let the demand for money be given by md - p = y - R • Let the IS curve be y = -r • Let the ‘Phillips’ curve be = (y-y*)+ e

Instability of of the interest rate peg with Adaptive Expectations

A positive IS curve shock R LM R* IS(e)’ IS+u IS Y Y*

Sargent & Wallace confirm the same result with RE • Should the monetary authorities use the interest rate or the money supply as its instrument of control? • It depends on the flexibility of prices and relative magnitudes of demand (real) versus nominal shocks • S&W show that if money is the instrument of control, there is a determinate price level • If R is the control variable, there is not.

McCallum (1981) (1986) • If the monetary authorities follow an interest rate rule, it is possible to obtain a determinate price level. • mt = m* + a(Rt-R*) • In a simple model with a forward expectations IS curve and a LM curve and a price surprise supply curve. • There is a deterministic solution and a stochastic solution

Monetary Policy - intermediate targets • The role of monetary policy in a stochastic environment • The intermediate target - money supply or interest rate to stabilise output? • When is the money supply the most appropriate intermediate target? • When the interest rate? • When a combination?

Assumptions • Authorities know the structure of the economy • Uncertainty is additive • Shocks to the IS curve are given by u and E(u) = 0 and E(u)2 = 2u • Shocks to the LM curve are given by v and E(v)=0 and E(v)2 = 2v • The price level is fixed and we are in the short-run

IS-LM Model • IS Schedule y = y0 - R + u • LM Schedule m = y - R + v • A positive u shifts the IS curve up • A positive v shifts the LM up to the left.

u, v > 0 LM+v R LM IS+u IS y

R* with only IS shocks R R* IS+u IS IS-u Y

R* with only LM shocks LM+v • R LM LM-v R* Y Y*

M* with only IS shocks • R LM IS+u IS IS-u Y

M* with only LM shocks • R LM+v LM LM-v IS Y

If only IS shocks - which is best intermediate target? • R LM IS-u R* IS+u IS Y

If LM shocks only - which is best intermediate target? • R LM+v LM LM-v R* IS Y* Y

Combination policy • R LM if IS shocks only LM if IS & LM shocks LM if LM shocks only IS Y

Summary • Interest rate is best intermediate target if LM shocks dominate • Money supply is best intermediate target if IS shocks dominate • Combination policy is superior to both if shocks come from both IS and LM