Download

1 / 32

330 likes | 468 Views

Module 6-WACC. Drew Williams. Basic Facts. Energy technology, project management, and maintenance (97% from oil and gas) Headquarted in Paris, France Revenue = 8.2 Billion Euros 11.5 Billion in Assets Employ 38,000 people in 48 countries 2 Major Segments Onshore/Offshore

E N D

Module 6-WACC Drew Williams

Basic Facts • Energy technology, project management, and maintenance (97% from oil and gas) • Headquarted in Paris, France • Revenue = 8.2 Billion Euros • 11.5 Billion in Assets • Employ 38,000 people in 48 countries • 2 Major Segments • Onshore/Offshore • Subsea—niche area

Financial Goals and Operating Priorities 6-8% margins on Onshore/Offshore projects ~15% margins on all subsea projects Continue to be the leader in tough climate and subsea contacts Keep a consist and robust order backlog Continue to innovate through extensive investment in R&D Focus on high growth areas i.e. Asia, Middle East, Brazil

Disclosures Did you hear about the cartoonist who was found dead in his home? The details are sketchy

Major Acquisitions • Global Industries Ltd. • December 2011 • 100% Ownership • Sub-Sea know-how • Further entry into US and Mexican waters • $1.262 Billion Purchase • Issues • Did not produce 2011 Financials • Solution: Use 2010 financials + Extrapolate 2011 Quarterly Income Numbers

Major Acquisitions • Stone & Webster Process Technologies • Purchase segment from The Shaw Group • Refining and Petroleum Chemicals—diversify • Further enter US Market • $295.3 Million Purchase • Isssues • No Financials for this Segment within Shaw • Purchased a segment of a segment • Different Fiscal Year (August 31 Year End) • The Shaw Group purchased in Feb 2013 • Solution: Input=0, cite as flaw in calculation, rely on group members more heavily

Determining Cost of Capital • Step 1: Determine Cost of Equity • Using CAPM • Step 2: Determine Cost of Debt • Using Financial Expense and NFL • Using F/S Disclosures • Step 3: Find Enterprise Cost of Capital from Cost of Debt and Cost of Equity • Weighted average

Cost of Equity-CAPM • Use inputs of Beta, risk-free rate, and Market return • Beta must be calculated using historic returns • Risk Free rate must be observed using available resources • Return on the market must be estimated • Only Beta is Firm Specific

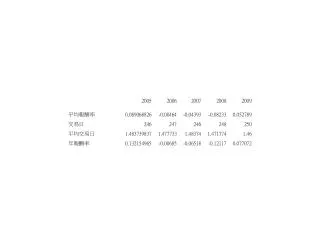

Estimating CAPM Inputs- Beta *Note: Did not subtract r(rf)—Bloomberg Method—small error possible • Beta- Stock’s Covariance with Market Returns • Method for obtaining Beta of Technip • Obtain Weekly Returns (yahoo finance) between 1/1/09 to 1/4/14 for TKPPY Adj. Price • Obtain Weekly Returns (yahoo finance) between 1/1/09 to 1/4/14 for S&P 500 • Run Regression with S&P 500 as independent variable and TKPPY as dependent • Beta = Coefficient of Correlation

Snapshot of Data Pun: I stayed up all night to ponder where the sun went…then it dawned on me

Problem with Results • Adj closing price jumps—no good explanation • No Big announcement on this day • Same Company’s stock trading in France featured no volatility • Trades as an American Depository Receipt (ADR) • Bank buys French Stock, sells it in multiples within US in USD • Seems to be an error

“Solution” to Issue Run Regression on Adj. Closing Price returns from 3/22/11 Run Additional Regression on Closing Price from 1/1/09 Run Regression on Technip stock traded on French Exchange

Regression Results-TKPPY ADJ Close from 3/22/11 • Key Stats: • Beta • R squared • Confidence Interval

Regression on TKPPY Closing Price from 1/1/09 • Key Stats: • Beta • R squared • Confidence Interval

Regression on TEC.PA from 1/1/09 to 1/4/14 • Key Stats: • Beta • R squared • Confidence Interval

Beta from Outside Sources • Observations • Ranges from 1.347 to 1.9 • 3 Sources did not have a Beta value for Technip • Huddles toward 1.5 or 1.9

Picking a Beta • Take Average of External Betas = 1.69 • Take Average of Internal Betas = 1.55 • Average 2 Values to get Beta = 1.62 • Rough Estimate • Many Beta numbers are justifiable • Find out what is driving split between ~1.5 estimates vs. ~1.9 estimates

Estimating Risk Free Rate • Yahoo Finance • r(rf) = 3.687% • Use as proxy of the risk free rate

Estimating Market Premium I would say 4% seems about right My decision: 4% Lloyd Blankfein—Goldman Sachs CEO

Final Cost of Equity r(rf) = 3.6870% Beta = 1.62 r(mkt)-r(rf) = 4% r(Eq) = 10.17%

Cost of Debt • Use of 2 Methods • Formulaic: (Interest Expense/Average amount of Interest Bearing Debt) * (1-T) • Financial Expense/NFL • Using F/S Disclosure • Average L-T borrowing Rate * (1-T)

Cost of Debt-Formula • Seems counterintuitive • Result of a negative NFL (NFA) • Observe other method

Cost of Debt F/S Disclosure • Borrowing Rate = 3.93% • Tax Rate = 33.33% (French Statutory) • r(debt) = 2.62% • Seems more intuitive • Does not take into account reformation

Cost of Capital for the Enterprise-Value of the Enterprise • Enterprise Value = market cap + NFL • NFL = €(251.32) • Exchange Rate = 1.36 • NFL = $(341.80) • Market Cap = $9,668.73 • 439.288 = # of shares • $22.01 = Share Price • Enterprise Value = $9,326.93

Cost of Capital for the Enterprise-Weighted Average With Formula Cost of Debt With F/S Disclosure Cost of Debt r(debt) = 2.62% V(debt) = $(341.80) V(Enterprise) = $9,326.93 r(equity) = 10.17% V(Equity) = $9,668.73 WACC = 10.44% • r(debt) = -28.5% • V(debt) = $(341.80) • V(Enterprise) = $9,326.93 • r(equity) = 10.17% • V(Equity) = $9,668.73 • WACC = 11.59%

Questions It’s impossible to explain puns to kleptomaniacs. They take everything…literally