Download

1 / 18

180 likes | 375 Views

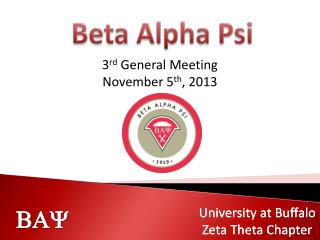

Alpha and beta attribution in property investment. The regression line. Y. residua l. gradient of the line is b (beta ). a (alpha). X. Meet alpha and beta. Return. Security Market Line. Risk (beta). Return may simply be a reward for taking more risk – this is beta.

E N D

The regression line Y residual . . . . . . gradient of the line is b (beta) . . . . a (alpha) X

Meet alpha and beta Return Security Market Line Risk (beta) Return may simply be a reward for taking more risk – this is beta

Meet alpha and beta Return Security Market Line Alpha Risk (beta) Return may be consistently higher without taking more risk – this is alpha

Alpha or beta? Opportunistic Distressed sellers Development, significant redevelopment, financial engineering, emerging sectors Value-added Repositioning Moderate redevelopment Core-plus Stable lease roll Moderate NOI Upside Return: 20%+ Leverage: 65-75%+ Return Return: 16-19% Leverage: 60-65% Core Fully leased multi- tenant property Return: 11-14% Leverage: 30-50% Return: 8-10% Leverage: 0-30% Risk

Which is best? • Sharpe ratio: return / risk • Market: 9.06%/7.41% = 1.22 • Fund A: 11.56%/7.41% = 1.56 • Fund B: 10.00%/15.70% = 0.64 • Information ratio: excess return / tracking error • Market: no tracking error, infinite information ratio • Fund A: no tracking error, infinite information ratio • Fund B: 0.94%/11.47% = 0.08

What is alpha? • Sub-market selection • geography: country/region • sector • Transaction and development skills • Asset management expertise

What is beta? • Leverage • Vacant buildings • Developments

Alpha and beta in property investment • Alpha and beta originate from structure and stock selection • Stock alpha • Cost control, leasing, asset enhancement, acquisitions, dispositions • Asset management and transaction skills • Structure alpha • Higher than benchmark allocations to outperforming markets and sectors • Risk classes constant • Stock beta • Continuum from ground rents to speculative developments • Structure beta • More volatile sectors, higher risk geographies

Cash flow based stock level attribution • Geltnerinvestigates the stock selection effect in more detail • Measures impact of these activities by isolating cash flows • Acquisition initial yield • Cash flow change • Yield shift

Performance attribution framework for property funds • Attribution of `excess’ IRR of a property fund • Fund structure: almost entirely the impact of leverage; fees will limit this • Beta • Timing: return impact of fund capital movements • Manager timing skill is reflected in this and is a source of alpha

Example: fund cash flows • Closed-ended • UK wide mandate but segment focussed: 4/12 UK segments • 55% in one of these • £99mn GAV / £26mn equity • 65-70% LTV • 22 assets • £4.5m average lot size • 2.5 year average hold period • Transaction skills • Capital distributed back quickly • Delivered a 31% net IRR to investors • But what was behind this?

Risk adjusted performance attribution Fund CAPM Net Fund TWRs vs Benchmark • Total returns: Fund 25.6% v benchmark 14.9% • Annualized SD: 23.0% v benchmark 5.3% • CAPM not statistically robust, but we have insight into the drivers of fund returns: • High beta – leverage, structure, asset level risk, short investment horizon • No evidence of alpha - but manager has been paid performance fees

Conclusions • Defined sources of alpha and beta in direct property and indirect property investment • Huge growth in unlisted property funds seen in recent times • Performance attribution framework for indirect funds • Need to consider fund structure which we believe is beta • Need to consider cash flow timing • Illustrative case study • At the direct property level the fund outperformed through segment specialisation • No evidence that it outperformed on a risk adjusted basis though – high beta • Were performance fees deserved? • Practical limitations • Data hungry analysis and the required information is not always available • Credibility of benchmarks