Download

1 / 7

70 likes | 79 Views

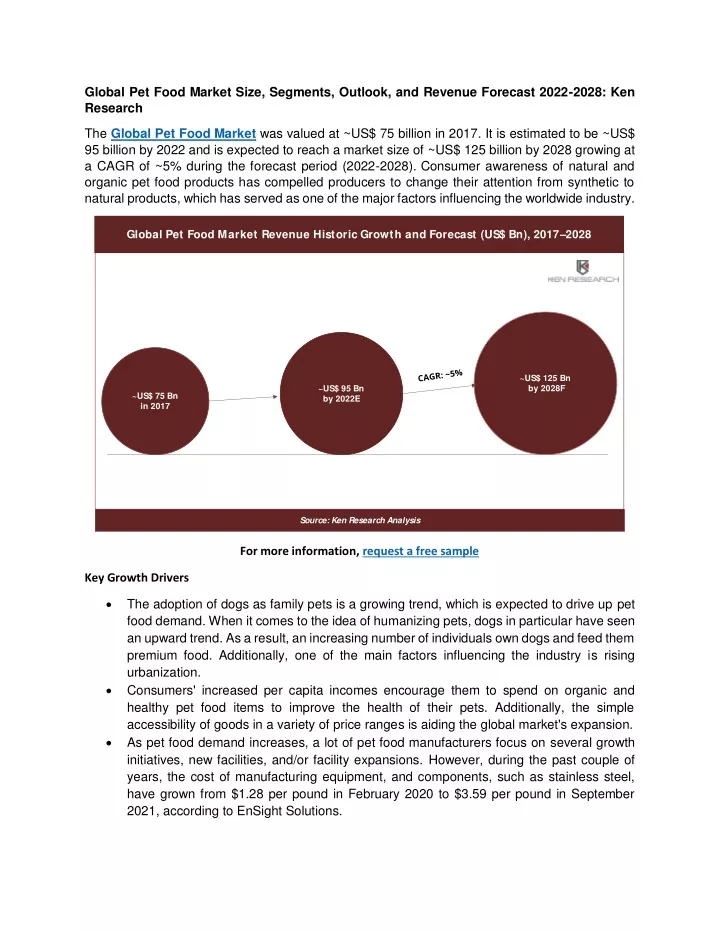

The Global Pet Food Market was valued at ~US$ 75 billion in 2017. It is estimated to be ~US$ 95 billion by 2022 and is expected to reach a market size of ~US$ 125 billion by 2028 growing at a CAGR of ~5% during the forecast period (2022-2028). <br>For More Information on the Research Report, refer to below links: u2013<br>https://www.kenresearch.com/business-research/global-pet-food-market-outlook-2028/

E N D

Global Pet Food Market Size, Segments, Outlook, and Revenue Forecast 2022-2028: Ken Research The Global Pet Food Market was valued at ~US$ 75 billion in 2017. It is estimated to be ~US$ 95 billion by 2022 and is expected to reach a market size of ~US$ 125 billion by 2028 growing at a CAGR of ~5% during the forecast period (2022-2028).Consumer awareness of natural and organic pet food products has compelled producers to change their attention from synthetic to natural products, which has served as one of the major factors influencing the worldwide industry. Global Pet Food Market Revenue Historic Growth and Forecast (US$ Bn), 2017–2028 ~US$ 125 Bn by 2028F ~US$ 95 Bn by 2022E ~US$ 75 Bn in 2017 Source: Ken Research Analysis For more information, request a free sample Key Growth Drivers The adoption of dogs as family pets is a growing trend, which is expected to drive up pet food demand. When it comes to the idea of humanizing pets, dogs in particular have seen an upward trend. As a result, an increasing number of individuals own dogs and feed them premium food. Additionally, one of the main factors influencing the industry is rising urbanization. Consumers' increased per capita incomes encourage them to spend on organic and healthy pet food items to improve the health of their pets. Additionally, the simple accessibility of goods in a variety of price ranges is aiding the global market's expansion. As pet food demand increases, a lot of pet food manufacturers focus on several growth initiatives, new facilities, and/or facility expansions. However, during the past couple of years, the cost of manufacturing equipment, and components, such as stainless steel, have grown from $1.28 per pound in February 2020 to $3.59 per pound in September 2021, according to EnSight Solutions.

Supply networks were negatively impacted by the COVID-19 outbreak. As a result of restrictions on the flow of raw materials, the pet food industry suffered in terms of supply and cash flow. On the other side, as a greater number of people adopted pets in response to a growing desire for the company during the lockdown, pet food consumption steadily increased in various regions of the world. Market participants shifted their attention away from physical storefronts and toward e-commerce platforms to meet this requirement. Key Trends by Market Segment By Product Type: Dry food segment held the largest market share in 2021, as it provides the crunch and chewing that animals require to maintain their general wellness. Dry food helps maintain good dental health by preventing plaque formation and minimizing tartar accumulation on the animal's teeth. Dry food does not require freezing in the same way that canned food does. Pet owners prefer pet food in the form of dry food. This is because dry-form products are more convenient and have a longer shelf life than wet food. The most popular choice for dogs is dry food because it is inexpensive and accessible to many dog owners. By Animal Type: The dog food segment held the largest market share in 2021, owing to the growing trend of nuclear families and consumers' increased preference for dogs as companions and security. Dogs are widely preferred as pets around the world, which is a significant factor in its dominance in the market. Moreover, the market for natural and high-quality dog food is being driven by the high costs involved with the maintenance and well-being of dogs. Another key factor in the segment's expansion is the introduction of dog treats and nutrient-dense food. In addition, dogs require a variety of nutrients to live a healthy life. Therefore, to keep their dogs healthy, dog owners have been concentrating on giving them quality pet food that contains these nutrients. This is expected to drive demand for pet food in the coming years.

Global Pet Food Market Revenue Share by Animal Type (in %), 2021 Dog Food Cat Food Others Source: Industry Publications and Articles, Ken Research Analysis Visit this Link Request for custom report By Ingredient: Animal-derived segment held the largest market share in 2021, as it provides high nutrition value which is required for a pet on a daily routine to meet its need for essential nutrients and energy. Pet food production has been using animal-based meat and meat products as a part of their basic ingredients. Fish meals, chicken meals, and other animal meals are commonly utilized in the production of cat and dog diets all over the world. The robust nutritious profile of animal-sourced pet food contributes to its high level of popularity. The accessibility of animal sources also contributes to market expansion. By Animal Age Group: Above 6 months segment held the largest market share in 2021, owing to the need to provide a proper balance diet to the pet. Between 6 and 12 months of age, the pets need a shift in their diet. The puppy can then start eating adult food when he is typically getting close to adult height. Spaying or neutering frequently takes place at this time as well, which reduces your dog's need for extra energy and provides justification for switching from puppy to adult dog food. A similar requirement for nutrition from pet food is observed for other pet animals as well. By Distribution Channel: Supermarkets and Hypermarkets segment held the largest market share in 2021, as they provide convenience to the consumer. This dominance can be explained by the great preference of consumers to purchase goods from big-box retailers because they have a wide variety of options for brands and pricing there. Supermarkets and Hypermarkets also provide pet food at a discounted rate and offer premium quality pet food products.

Global Pet Food Market Revenue Share by Distribution Channel (in %), 2021 Supermarkets and Hypermarkets Pet Stores Online Stores Others Source: Industry Publications and Articles, Ken Research Analysis To more about industry trends, Request a free Expert call By Geography: North Americais expected to account for the largest share among all regions within the total Pet Food Market, during the forecast period 2022-2028 One of the key factors in North America dominance is the high rate of pet adoption in American households. According to a survey done by the American Pet Products Association (APPA) in 2020, 70% of households in the USA, or 90.5 million homes, own a pet. The adoption of pet humanization and the favorable public perception of it in North America is fostering market expansion for wholesome pet food products.

Major Regions by Revenue Share within Global Pet Food Market, 2021 Largest Region North America Europe Asia Pacific LAMEA Source: Ken Research Analysis Competitive Landscape The Global Pet Food Market is highly competitive with ~200 players which include globally diversified players, regional players, and country-niche players with their niche in pet food. Regional players constitute ~45% of the competitors, while the county-niche players are the second largest by type. Some of the major players in the market include Mars Incorporated, Hill's Pet Nutrition, Inc., The J.M. Smucker Company., Schell & Kampeter, Inc., The Hartz Mountain Corporation, Nestlé Purina, Blue Buffalo Company, Ltd., Wellness Pet Company, Inc., Tiernahrung Deuerer GmbH, Head up for tails, among others.

Competitive Landscape of Global Pet Market Market - Estimated Share of Total Competitors by Type and Porter’s 5 Forces Analysis of Industry Estimated Share of Total Competitors by Type, 2021 Porter’s 5 Forces Analysis of Industry Bargaining Power Of Suppliers: LOW 20% 35% Internal Competitive Rivalry: HIGH Bargaining Power Of Buyers:HIGH 45% Country-Niche Players Regional Players Global Players Threat Of New Entrants: HIGH Threat Of Substitutes: MODERATE Source: Industry Publications, Ken Research Analysis Recent Developments Related to Major Players In December 2020, Nestle Purina Petcare announced plans to invest US$ 550 million to increase the size of its Georgian pet food production facility. In March 2021, Leading pet food producer Mars, Inc., with headquarters in the USA, committed US$ 200 million to develop its Royal Canin facility in Lebanon. To increase its production capacity, the company installed five new corporate lines. In September 2020, Nestle Purina announced intentions to build a wet pet food factory in Hartwell, investing US$ 320 million and employing 240 employees by 2023. With US$ 870 million spent on the company's Hartwell operations, the facility is expanding to increase processing, packaging, and warehousing capacity in response to rising demand for Purina's premium and nutrient-rich pet care brands. Conclusion The Global Pet Food Market is forecasted to continue the growth that is witnessed since 2017. Some of the primary factors driving market expansion are an increase in per capita disposable income, an increase in the tendency of nuclear families, and a quick increase in pet humanization. Though the market is highly competitive with ~200 players, few global players control the dominant market share and regional players also hold a significant market share. Note: This is an upcoming/planned report, so the figures quoted here for a market size estimate, forecast, growth, segment share, and competitive landscape are based on initial findings and might vary slightly in the actual report. Also, any required customizations can be covered to the best feasible extent for Pre-booking clients, and the report delivered within a maximum of two working weeks.

Ken Research has recently published report titled, Global Pet Food Market Size, Segments, Outlook, and Revenue Forecast 2022-2028. In addition, the report also covers market size and forecasts for the four region’s Pet Food Markets. The revenue used to size and forecast the market for each segment is US$ billion. Market Taxonomy Dry Food Wet Food Snacks and Treats Product Type Dog Food Cat Food Others Animal Derived Plant Derived Others Below 6 months Above 6 months Supermarkets and Hypermarkets Pet Stores Online Stores Others North America (USA, Canada, Mexico) Europe (Germany, UK, France, Spain, Italy) Asia-Pacific (China, Japan, South Korea, India, Indonesia, Australia) LAMEA (Latin America, Middle East, Africa) Mars, Incorporated Hill's Pet Nutrition, Inc. The J.M. Smucker Company. Schell & Kampeter, Inc. The Hartz Mountain Corporation Nestlé Purina Blue Buffalo Company, Ltd. Wellness Pet Company, Inc. Tiernahrung Deuerer GmbH Head up for tails Animal Type Ingredient Animal Age Group Distribution Channel By Geography Leading Companies