Download

1 / 16

160 likes | 371 Views

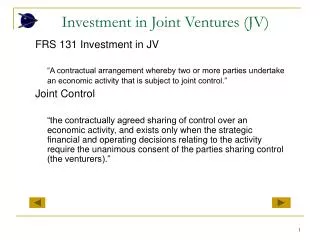

FRS 131 Investment in JV “A contractual arrangement whereby two or more parties undertake an economic activity that is subject to joint control .” Joint Control

E N D

FRS 131 Investment in JV “A contractual arrangement whereby two or more parties undertake an economic activity that is subject to joint control.” Joint Control “the contractually agreed sharing of control over an economic activity, and exists only when the strategic financial and operating decisions relating to the activity require the unanimous consent of the parties sharing control (the venturers).” Investment in Joint Ventures (JV)

Two common characteristics: two or more venturers are bound by a contractual arrangement; and the contractual arrangement establishes joint control. No one party controls the venture unilaterally nor dominates the financial and operating decisions Cont.

Examples of areas covered by the contractual arrangement: The activity, duration and reporting obligations of the JV The appointment of the BODs or equivalent governing body and voting rights of the venturers Capital contributions of the venturers Manner of sharing among the venturers of the JV output, income, expenses and results Cont.

Three forms of JV (FRS 131) (a) Jointly controlled operations No establishment of a separate business enterprise Two or more venturers share their operations, resources and expertise in order to produce, market and distribute jointly a particular product such as ship or aircraft. Each venturer uses its own assets and incurs its own expenses At the end, they share the revenue form the sale of a joint venture product and any expenses incurred in common Cont.

(b) Jointly controlled assets No establishment of a separate business enterprise The venturers have joint control of one or more assets contributed for the JV such as holiday villa & gas pipeline. Each venturer may take a share of the output from the assets and each bears an agreed share of the expenses incurred. Cont.

(c) Jointly controlled entities Establishment of a separate business enterprise which could be a company, partnership or other form of entity The JV will have its own set of accounts and prepare its own set of financial statements For the venturer its contribution to the JV will be disclosed as an investment and for the JV the contributions made by the venturers are capital distribution Cont.

FRS 131 requires the venturer to account for the interest in JV in its separate financial statement, which is not held for sale, at cost or in accordance with FRS139 In the consolidated financial statements the venturer has either to apply the equity method or proportionate consolidation Accounting Treatment of JV

A venturer shall discontinue the use of proportionate consolidation from the date on which it ceases to have joint control over a jointly controlled entity. (para 36) A venturer shall discontinue the use of the equity method from the date on which it ceases to have joint control over, or have significant influence in, a jointly controlled entity. (para 41). Cont.

FRS 131 Para 45 From the date on which a jointly controlled entity becomes a subsidiary of a venturer, the venturer shall account for its interest in accordance with FRS 127. From the date on which a jointly controlled entity becomes an associate of a venturer, the venturer shall account for its interest in accordance with FRS 128. Cont.

The venturer is exempted from using the proportionate consolidation or equity method except the following situations: (a) The investment is classified as held for sale in accordance with FRS 5 (b) the parent company that has interest in a jointly controlled enterprise satisfies the exemptions under paragraph 10 of FRS 127 that it: (i) itself is a wholly owned subsidiary Cont.

(b) The venturer is exempted from presenting consolidated financial statement; or (c) When all the following apply: (i) itself is a wholly owned subsidiary (ii) itself a partially-owned subsidiary and its owners (including those not entitled to vote) had been informed about and do not object to the ventrurer not to apply proportionate consolidation or equity method (iii) Venturer’s debt and equity instruments are not traded in a public market. Cont.

(iv) Venturer did not file nor in the process of filing financial statements with security commission. (v) The ultimate or the intermediate parent of the venturer is incorporated in Malaysia and produces consolidated financial statements available for public use that comply with FRS. Cont.

FRS 131 “a method of accounting whereby a venturer’s share of each of the assets, liabilities, income and expenses of a jointly controlled entity is combined line by line with similar items in the venturer’s financial statements or reported as separate line items in the venturer’s financial statements.” Proportionate Consolidation

In proportionate consolidation the investor’s share of the net assets will be consolidated with that of the investor’s net assets. Each item of the assets and liabilities of the investor and the investor’s share of each item of asset and liability of the JV will be aggregated. If the investor has a 25% interest in a JV then only 25% of each asset and liability will be consolidated and not 100%, unlike when consolidating a subsidiary and disclosing the MI in the subsidiary. Cont.

Likewise, the items in the income statement (revenues and expenses) are treated similarly by aggregating the investor’s revenues and expenses by aggregating with the venturer’s 25% share in the JV enterprise There is no MI in any JV entity as each partner is an equal partner to the JV Cont.

On consolidation, the cost of investment in a venturer’s account is cancelled off with its proportionate share of the net assets of the JV entity as at the acquisition date, with the resulting difference (if any) being treated as goodwill on consolidation There is no goodwill if the JV is established by the venturer’s themselves If the equity method (alternative method) is used, the cost of investment is not eliminated and the amount of investment in JCE would be reported in balance sheet Cont.