Download

1 / 8

100 likes | 469 Views

Budgeting Basics- Taking an All Funds Approach . Northern Arizona University University Budget Office. Funding Shifts. State appropriation funding has decreased from nearly 40% of funding sources in FY08 to 23% in FY14

E N D

Budgeting Basics-Taking an All Funds Approach Northern Arizona University University Budget Office

Funding Shifts • State appropriation funding has decreased from nearly 40% of funding sources in FY08 to 23% in FY14 • Tuition and Fees, Government Grants and Contracts, and Auxiliary funding sources have increased during this time

State Funding • State Budget continues to be significantly impacted from the reduction in General Fund Appropriations • FY13 marked the first year General Fund Appropriations made up less than 50% of the initial State Budget • Increased funding from tuition collections has helped offset the 31% decline in general fund appropriation since 2008

Local (Designated/Auxiliary) Funding • Beginning Balance; Revenue; Net Transfers In • Providing significantly more sources of funding to support unit operations • 65% growth from FY09 actual funding sources to FY14 budgeted funding sources

Combined State and Local Resources • Impact from adding local funding resources to state resources is significant for all units

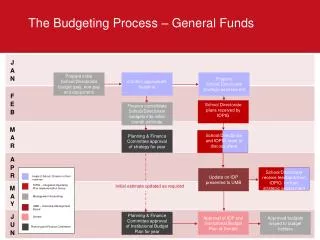

All Funds Budgeting • Important to incorporate all funding sources during the budgeting process and throughout the year • Helps to determine what resources are available to fund University, Division and Department priorities • Questions to further clarify your decisions • What are your recurring expenses (e.g. people) and what are the changes you expect to those recurring expenses (either new ones or ones that should/need to end)? • Should/Could they be funded on state funds or local funds? • What are your 1 time expenses (operations/capital/new initiatives)? • Do you have room for those expenses on your state funds (if expenses are allowed) or do you have local funds to cover it? • Do you have funding to cover your expenses through state funds, beginning balances, new revenue? • Is your revenue a recurring revenue stream or a one time event? • Do you expect to see a decrease or increase in your local ending balance compared to your beginning balance? • What other changes do you expect?

General questions to consider during budgeting process • What additional transactions do you expect to see before year end that will impact your YTD revenue and expense? • How do your YTD expenses/revenues compare to the projected amount for the end of the year? • If you are projecting LESS than your YTD amounts, what transactions do you expect that will decrease the amount by the end of the year? • If you are projecting MORE, is the additional amount realistic given the amount of time left in the year?

Resources to use in Budgeting • NSTAR Reports • Finance • HR • Salary Change Report (JFR access on Budget Shares drive) • Budget Adjustments and Local Fund Transfer listings (JFR Access on Budget Shares drive) • Business Objects Reports • Transaction Detail • Status of Funds • Payroll • PS Financials • Budget Overview