Download

1 / 8

80 likes | 352 Views

DELTA (?). DELTA = ? in portfolio value / ? in the underlying market variableExample: Suppose you a have portfolio that has exposure to changes in the value of gold. If the value of your portfolio decreases by $100 when the value of gold increases by $0.1/ounce, then the delta of the portfolio equ

E N D

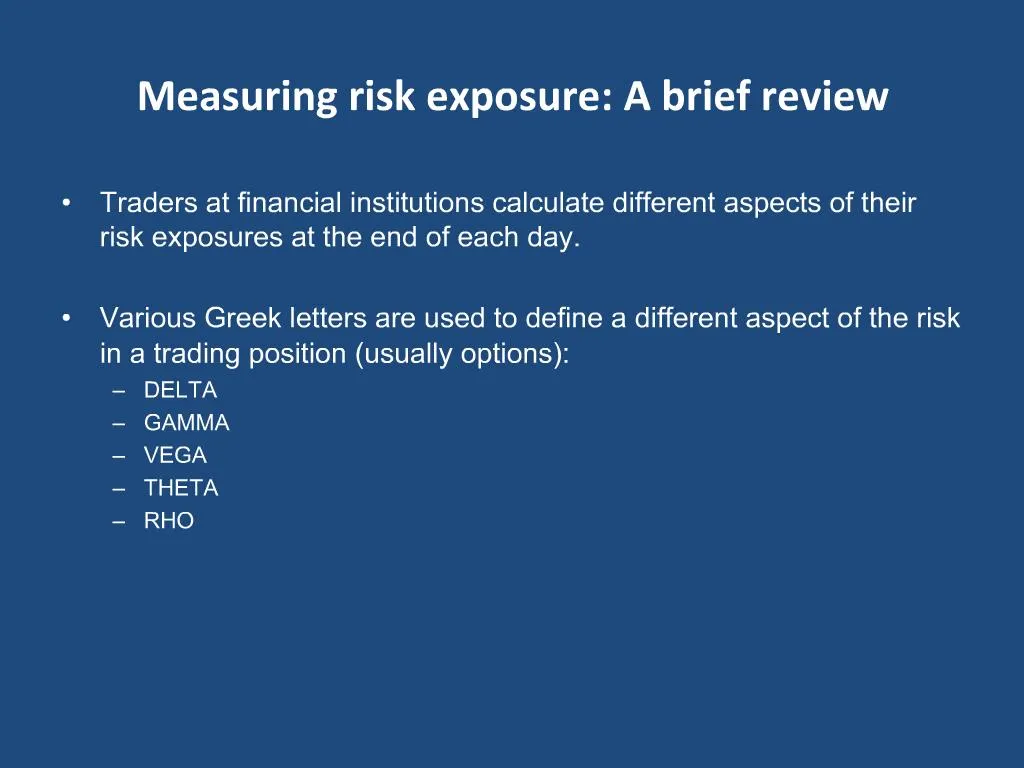

1. Measuring risk exposure: A brief review Traders at financial institutions calculate different aspects of their risk exposures at the end of each day.

Various Greek letters are used to define a different aspect of the risk in a trading position (usually options):

DELTA

GAMMA

VEGA

THETA

RHO

2. DELTA (?) DELTA = ? in portfolio value / ? in the underlying market variable

Example: Suppose you a have portfolio that has exposure to changes in the value of gold. If the value of your portfolio decreases by $100 when the value of gold increases by $0.1/ounce, then the delta of the portfolio equals -$100/$0.1 = -$1,000

Interpretation: $1 increase in the ounce of gold results in $1,000 trading losses.

Delta-neutral portfolio: If you add to your portfolio gold that is worth $1,000, your exposure to changes in the price of gold will be zero; put differently, you will have a delta-neutral portfolio.

3. Linear vs. Non-linear products When the price of a product is linearly dependent on the price of an underlying asset a ``hedge and forget�� strategy can be used

Non-linear products require the hedge to be rebalanced to preserve delta neutrality

4. GAMMA (G) Measures how the portfolio�s delta changes with respect to the price of the underlying market variable.

If G = 0, then you don�t need to make adjustments to your delta-neutral portfolio.

However, if G is large (in absolute terms), you need to frequently rebalance in order to protect yourself against exposure to a market variable.

Long option positions have high gammas. Black-Scholes option pricing model is based on the idea of making a portfolio�s gamma neutral by continuously rebalancing with respect to changes in the price of underlying asset.

5. VEGA (?) ? measures the change in portfolio value with respect to changes in the volatility of the underlying market variable.

High ? implies high exposure to changes in volatility

? of a long option position is positive.

6. THETA (T) T measures the rate of change in the value of the portfolio with respect to the passage of time (all else the same). It is also referred to as the time decay of the portfolio.

T < 0 for options

T is not something to hedge against

7. RHO (?) ? is the change in the value of portfolio with respect to interest rates.

8. Black-Scholes option pricing formula