Download

1 / 24

240 likes | 351 Views

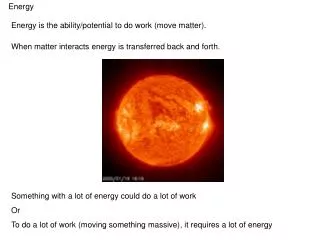

ENERGY INSURANCE MUTUAL. 19th ANNUAL RISK MANAGERS INFORMATION MEETING. The Westin Innisbrook Golf Resort Tarpon Springs, Florida February 27 - March 1, 2005. The Evolving Landscape of Directors’ & Officers’ Liability:

E N D

ENERGY INSURANCE MUTUAL 19th ANNUALRISK MANAGERSINFORMATION MEETING The Westin Innisbrook Golf Resort Tarpon Springs, Florida February 27 - March 1, 2005

The Evolving Landscape of Directors’ & Officers’ Liability: A Discussion of Securities Litigation, Settlement Trends & Market Response February 28, 2005

Federal Securities Fraud Class Action FilingsFrequency 493 92 93 94 95 96 97 98 99 00 01 02 03 04 2005 YTD Pre-Reform Act Post-Reform Act Source: Securities Class Action Clearinghouse (2/8/05)

Mega D&O Case Settlements / Court Awards 2004-2005Severity • McKesson $960 million • Global Crossings $245 million • Raytheon Company $210 million • Symbol Technologies, Inc. $138 million • Royal Dutch Shell $150 million • Bristol-Myers Squibb $300 million • Qwest $250 million • AT&T $100 million Cash amounts

10 Largest Public Company D&O SettlementsSeverity • Cendant $3.2 b 2001 • Credit Lyonnaise S.A. $772mm 2003 • McKesson Corp (pending) $960mm 2005 • Time Warner $510mm 2004 • MCI/WorldCom $500mm 2003 • Bank of America $490mm 2002 • Waste Management $457mm 2001 • CompUSA $454mm 2002 • HCA $418mm 2002 • Lucent $315mm 2003

From Filing to Settlement / DismissalDuration SOURCE: Willis Re Professional Liability 2004 Federal Securities Class Action Filings & Settlements Analysis

Broadening the Litigation NetProliferation • Federal securities class actions • Non-class action shareholder claims-The institutional investor lead plaintiff • State Blue Sky Law claims • Shareholder derivative actions • Creditor derivative actions • ERISA-based claims – regulatory • ERISA-based claims – single claimant • ERISA-based claims – class action • SEC investigations / penalties • State Attorney General actions • Local criminal prosecutions • State criminal prosecutions • Whistleblowers - False Claims Act

Top Plaintiff’s Law Firms 2003Momentum These firms recovered the highest settlement totals for securities class actions during 2003

2004 Securities Class Action Filings By Industry(Total vs. Energy) Source: Cornerstone Research’s 2004: A Year in Review

Marketplace ResponsePricing Perspective Possible ranges based uponunderwriter perception Underwritertendency Rates Willis effort Large Non-profit Private Companies Small to Mid-Sized Large Cap Cap Cap/Distressed Types of Companies

Market Observations • Volatility – mega claims + traditional claims are driving losses • More $100 million+ claims than ever • But no amount too insignificant to pursue (materiality not a factor) • Average loss numbers up • 1986: $1.5 million • 2001: $15 million • 2003: $25 million • 2004: project $27 million+ • Institutional Investor changes the landscape • Seeking larger settlements • Seeking individual assets (50% plaintiff arrangements) • Greatest threat to D&O? • Regulatory exposure has surpassed shareholder exposure • 18 SEC penalty payments in xs of $50 million in history of SEC • 12 occurred in past 15 months • 2000 companies under SEC investigation since 1996

WorldCom SettlementStatus • 10 former directors agreed to pay $18M of a $54M settlement New York State Common Retirement Fund’s lawsuit, pending in the U.S.D.C. S.D.N.Y. • $36M from D&O coverage • Unique facts • Egregious actions by directors and officers • Fraud • Insider Selling • Lead plaintiff • Settlement not a function of contract language • Plaintiffs withdraw from settlement agreement • US District Judge rejected key provision • Directors will stand trial with other defendants on Feb 28th in absence of new settlement agreement

Growth in A-Side Coverage Personal Assets Protection • An answer to two separate questions: • Why do we buy D&O insurance? • How much is enough? • Now prevalent in D&O programs for most Fortune 500 companies • In part a response to changing liability environment

D&O Program DesignTraditional + A-Side DIC IDL $25MM DIC feature Broad Form A-Side $50MM xs $100MM D&O (A/B/C Coverage) $100MM • Factors to Consider: • Balance sheet protection • Personal asset protection • DIC feature on the A-side program • Potential to share limits with fiduciary

Program DesignImpact of Layering PROs • Attract more capacity • Spread risk among multiple carriers • Less reliance upon single carrier capacity • Take advantage of ILF discounts • Create impediment to swift settlement CONs • Create impediment to swift settlement • Potential cost driver • Smaller premium bank/carrier • Claim • Renewal

Critical Coverage Issues2005 Renewal • Severability of the application • Non-rescindable A-side protection • Severability & imputation of the conduct exclusions • Pollution Exclusion (existence, carveouts) • Entity coverage vs. predetermined allocation • Coinsurance • Continuity • Definitions • Application • Claim • Loss • Notice of claim provision • Narrow Insured vs. Insured Exclusion • Global protection • Employed Lawyers’ coverage (?) • Bilateral Discovery

Renewal StrategiesRisk and Cost Mitigation Techniques • Introduction of Non-rescinding Side A Coverage into the Primary policy form • Corresponding Impact on Traditional A Side/DIC Marketing and Premium Negotiation • Continued Emphasis on Increased Limit Factors (ILF’s) vs. Underlying Rates • Increased reluctance within the Excess community • For Companies that are migrating back to traditional D&O structures is Continuity an Issue? • Engage Multiple Constituencies within the Firm

Limits DeterminationFactors for Consideration • Benchmarking • Peer group • Industry • Market capitalization • Market capitalization impact analysis • Settlement trends • Board mandate • Historical limit carried • Claims experience • Individual or corporate protection • Cost

With All the Focus on Your D&O Renewal, What of Your Fiduciary Liability Program? Top 5 indicators of a tricky Fiduciary renewal: • Employer securities in any employee benefit plan anywhere, anyhow, anywhere in the world. • (Significant) under- or over-funding in any DB plan anywhere in the world. • M&A activity, or the reverse, divestitures. • Changes to the benefit promise (especially retiree benefits, or, when combined with any of the above). • Conversion to a cash balance plan (a class by itself).

Just What Do We Mean by a “Tricky” Fid Renewal? • Rate increases: market not yet flattening • Retention increases: approaching D&O for E/R securities • Restrictions of T&C, including: • Severability (D&O all over again) • Choice of counsel • Personal conduct exclusions • Possible sublimits or common-claims tie-ins • Duty-to-defend • Getting a quote at all: no Bermuda, no real London capacity…

Recommended Fiduciary Renewal Strategy • Recognize that the market is in correction (after 30 years) • Don’t allow this renewal to get lost in the shuffle (focus, prepare, be aware, give it the time that it may need) • Be strategic in choosing your ER carriers (aggregation is either a requirement or an impediment) • Consider adding the coverage to an aggregate excess program(but…) • Beware of possibly fully eroding D&O program (if simply delete ERISA exclusion from this other tower of coverage) • Be prepared to differentiate your risk (“here’s how we are addressing our underfunding…”)

The Evolving Landscape of Directors’ & Officers’ Liability: A Discussion of Securities Litigation, Settlement Trends & Market Response February 28, 2005