Download

1 / 6

60 likes | 71 Views

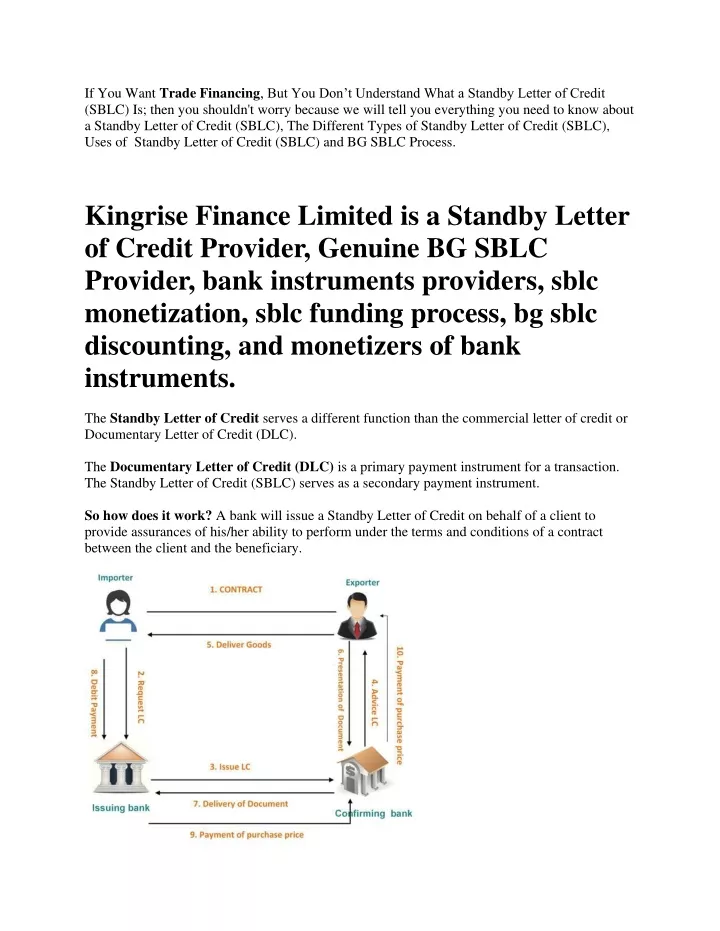

If You Want Trade Financing, But You Donu2019t Understand What a Standby Letter of Credit (SBLC) Is; then you shouldn't worry because we will tell you everything you need to know about a Standby Letter of Credit (SBLC), The Different Types of Standby Letter of Credit (SBLC), Uses ofu00a0 Standby Letter of Credit (SBLC) and BG SBLC Process.u00a0<br><br>Kingrise Finance Limited is a Standby Letter of Credit Provider, Genuine BG SBLC Provider, bank instruments providers, sblc monetization, sblc funding process, bg sblc discounting, and monetizers of bank instruments.The Standby Letter of Credit serves a different function than the commercial letter of credit or Documentary Letter of Credit (DLC).<br><br>If you need further information about Standby Letter of Credit (SBLC), Bank Guarantee (BG) or any other financial instrument kindly contact Kingrise Finance Limited For More Information and Assistance.<br><br>Email: info@kingrisefinance.com<br>Website: www.kingrisefinance.com<br>Blog: https://kingrisefinance.blog

E N D

If You Want Trade Financing, But You Don’t Understand What a Standby Letter of Credit (SBLC) Is; then you shouldn't worry because we will tell you everything you need to know about a Standby Letter of Credit (SBLC), The Different Types of Standby Letter of Credit (SBLC), Uses of Standby Letter of Credit (SBLC) and BG SBLC Process. Kingrise Finance Limited is a Standby Letter of Credit Provider, Genuine BG SBLC Provider, bank instruments providers, sblc monetization, sblc funding process, bg sblc discounting, and monetizers of bank instruments. The Standby Letter of Credit serves a different function than the commercial letter of credit or Documentary Letter of Credit (DLC). The Documentary Letter of Credit (DLC) is a primary payment instrument for a transaction. The Standby Letter of Credit (SBLC) serves as a secondary payment instrument. So how does it work? A bank will issue a Standby Letter of Credit on behalf of a client to provide assurances of his/her ability to perform under the terms and conditions of a contract between the client and the beneficiary.

The parties involved with the transaction do not expect that the Standby Letter of Credit (SBLC) will ever be drawn upon. The Standby Letter of Credit guarantees the beneficiary of the performance of the client’s obligation. The beneficiary is able to draw under the credit by presenting documents and evidence to the issuing bank that the client has not performed its obligation. The issuing bank is obligated to make payment if the documents presented comply with the terms and conditions of the Standby Letter of Credit. So What is a Standby Letter of Credit (SBLC)? A Standby Letter of Credit (SBLC or SLOC) is a legal document that guarantees a bank’s commitment of payment to a seller in the event that the buyer or the bank’s client defaults on the agreement. A standby letter of credit helps facilitate international trade between companies that don’t know each other and have different laws and regulations. Although the buyer is certain to receive the goods and the seller certain to receive payment, a Standby Letter of Credit (SBLC) doesn’t guarantee the buyer will be happy with the goods. A standby letter of credit can also be abbreviated SBLC or SLOC. Click Here to Get A Standby Letter Of Credit (SBLC) From One Of Our Top World Banks Trade Finance Business — Standby Letters of Credit (SBLC) Why are they issued? Standby Letters of Credit (SBLC) are usually issued by banks to guarantee financial obligations, to assure the refund of advance payments, to support performance and bid obligations, or to assure the completion of a sales contract. The Standby Letter of Credit always has an expiration date. The Standby Letter of Credit is often used to guarantee contract performance or to strengthen the credit worthiness of a client. If payments are made in accordance with the suppliers’ terms and conditions, the Standby Letter of Credit (SBLC) would not have to be drawn on. The seller goes directly to the customer for payment. What if the client doesn’t pay? If the client is unable to pay, the seller presents the documents to the issuing bank for payment. The Standby Letter Of Credit (SBLC) is governed by a set of guidelines known as the

Uniform Customs and Practice (UCP 600), which was first created in the 1930s by the International Chamber of Commerce (ICC). The difference between Bank Guarantee (BG) & Letter of Credit (LOC) Bank Guarantee is not the same as a letter of credit, although with both instruments the issuing bank accepts a customer’s liability if the customer defaults. With a guarantee, the seller’s claim goes first to the buyer, and if the buyer defaults, then the claim goes to the bank. With letters of credit, the seller’s claim goes first to the bank, not the buyer. Although the seller will likely get paid in both cases, letters of credit offer more assurance to sellers than guarantees generally do. LOC is a financial document which imposes an obligation on the bank to make payment to the beneficiary on completion of certain services as required by the applicant. LOC is issued by the bank when the buyer requests his bank to make payment to the seller on the receipt of certain goods or services. That is, when the buyer runs into cash flow difficulties or similar situations and thus cannot make immediate payment to the seller, he will approach his bank to make the payment to the seller on submission of certain documents. The bank will later recover the amount paid from the buyer along with the required charges. On the other hand, under BG, the bank is required to make payment to the third-party only if the applicant fails to make the payment to the third-party or does not fulfil the required obligations under the contract. A BG is essentially used to ensure a seller from loss or damage due to the non-performance by the other party in a contract. However, there are a lot of differences between LOC and BG. Major differences between Letter of Credit (LOC) and Bank Guarantee (BG) Particulars LOC BG BG is an assurance given by the bank to the beneficiary to make the specified payment in case of default by the applicant. The bank assumes to make the payment only when the customer defaults to make payment. Only when the customer defaults the payment to the beneficiary, the bank makes the payment. LOC is an obligation accepted by a bank to make payment to a beneficiary if certain services are performed. Nature Bank retains the primary liability to make the payment and later collects the same from the customer. Bank makes the payment to the beneficiary as and when it is due. It need not wait for a default to be made Primary liability Payment

Particulars LOC by the customer. LOC ensures that the amount will be paid as long as the services are performed as per the agreed terms. There are multiple parties involved here – LOC Issuing bank, its customer, the beneficiary (third party), and advising bank. Generally, this is more appropriate during the import and export of goods and services. Bank assumes more risk than the customer. BG BG assures to compensate for the loss if the applicant does not satisfy the specified conditions. Way of working Number of parties involved There are only three parties involved – banker, its customer, and the beneficiary (third party). Suits any business or personal transactions. Suitability Risk Customer assumes the primary risk.

How Does a Client Receive a Standby Letter of Credit (SBLC) from KINGRISE FINANCE LIMITED. The best way to Receive a Standby Letter of Credit (SBLC) Is through Kingrise Finance Limited. Kingrise Finance Limited was incorporated in Hong Kong on 22-SEP-1999 to provide Business Loan, SME Loans, Project Financing, Recourse / Non Recourse Loans, Secured / Unsecured Loans, Standby Letter of Credit Funding, Bank Guarantee, Performance Guarantee Bond, Tender Bond Guarantee, Advance Payment Guarantee, Bank Comfort Letter etc. Step 1: Application Fill out and return the Standby Letter of Credit (SBLC) Application Step 2: Issuing of Draft A draft of the Standby Letter of Credit (SBLC) will be created for you and your seller/supplier/exporter to review. Step 3: Draft Review and Opening Payment a) Finalize the draft between you and your seller/exporter and sign off on the draft (changes are free of cost). b) We issue you a payment invoice for the SBLC, which you arrange to pay. c) Once we receive your wire payment, we will release the finalized Standby Letter of Credit (SBLC) to the bank for issuance and delivery. Step 4: Issuance More often than not, the bank will issue the Standby Letter of Credit (SBLC) within 48 hours of release. Once issued, a copy of the SBLC will be emailed to you as it is transmitted by SWIFT, including the reference number of the SBLC. Your seller’s bank should be able to receive and confirm the Standby Letter of Credit (SBLC) transmission soon thereafter. Step 5: Presentation of Documents Once the seller/exporter has prepared and loaded all goods for shipment, they must send the

specified documents for that particular shipment to their own bank. Their bank will then forward the documents to our bank, and we will email you copies of the presentation and all of the documents that were submitted by the seller/exporter for your review and approval. Step 6: Payment of Goods Before our bank can release the original documents, we must receive payment for the presentation. Once we have received payment, we cosign the documents to you and overnight them to your freight forwarder or to whomever you wish. This completes the transaction. If you need further information about Standby Letter of Credit (SBLC), Bank Guarantee (BG) or any other financial instrument kindly contact Kingrise Finance Limited For More Information and Assistance. Email: info@kingrisefinance.com Website: www.kingrisefinance.com Blog: https://kingrisefinance.blog