Download

1 / 9

90 likes | 163 Views

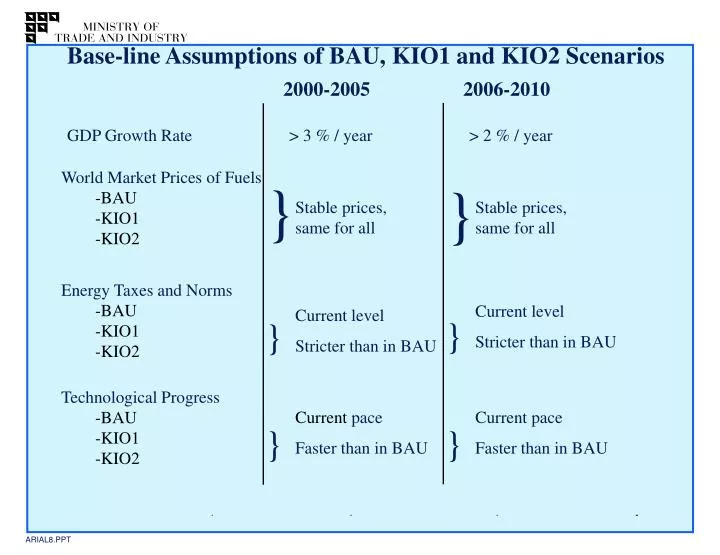

Base-line Assumptions of BAU, KIO1 and KIO2 Scenarios. 2000-2005. 2006-2010. GDP Growth Rate. > 3 % / year. > 2 % / year. World Market Prices of Fuels -BAU -KIO1 -KIO2. }. }. Stable prices, same for all.

E N D

Base-line Assumptions of BAU, KIO1 and KIO2 Scenarios 2000-2005 2006-2010 GDP Growth Rate > 3 % / year > 2 % / year World Market Prices of Fuels -BAU -KIO1 -KIO2 } } Stable prices, same for all Stable prices, same for all Energy Taxes and Norms -BAU -KIO1 -KIO2 Current level Stricter than in BAU Current level Stricter than in BAU } } Technological Progress -BAU -KIO1 -KIO2 Current pace Faster than in BAU Current pace Faster than in BAU } } ARIAL8.PPT

Base-line Assumptions of BAU, KIO 1and KIO2 Scenarios 2000-2005 2006-2010 Use of Renewables -BAU -KIO1 -KIO2 Current development Increase from BAU Current development Increase from BAU } } Natural Gas Network -BAU -KIO1 -KIO2 } } Current, same for all Extending in Southern Finland, same for all Nuclear Power -BAU -KIO1 -KIO2 } } Current capacity, same for all Current capacity KIO2: additional 1300 MW Electricity Imports -BAU -KIO1 -KIO2 } } 7-8 TWh / year, same for all 6 TWh in 2010, same for all

GDP by Sector, bn FIM 1995 1000 900 Services 800 Construction 700 Industry Primary production 600 500 400 300 200 100 0 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Total Production by Branch of Industry, bn FIM 1995 350 Electrical 300 Other 250 Metals 200 Chemicals Wood Processing 150 100 50 0 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Projected World Market Prices of Crude Oil, Natural Gas and Hard Coal in KIO Scenarios, 2000 = 1 1,6 1,4 1,2 1 Crude Oil, USD/bbl 0,8 Natural Gas, USD/1000 m3 0,6 Hard Coal, USD/t 0,4 0,2 0 1995 2000 2005 2010 2015 2020

Diversity in Electricity Supply, TWh 100 Wind Power 90 80 Hydro Power 70 CHP, industry 60 CHP, District Heat 50 TWh 40 Condensing Power (fossil fuels) 30 Electricity Imports 20 NuclearPower 10 0 2000 2010 2010 ’Natural Gas’ ’Nuclear Power’

CONCLUSIONS (1/2) • GHG emissions depend on a few major factors: • the growth and structure of the economy • the structure of electricity supply (imports, hydro power, nuclear power, electricity produced from fossil fuels) • GHG emissions projected in the BAU scenario will exceed target levels in 2008/12. Determined and effective action is necessary to curb emissions. • The Energy Conservation Programme and the Action Plan for Renewable Energy Sources are certain to be implemented. Together these two programmes could account for about a half of the targeted emission reduction. • Use of coal has to be curbed considerably. Alternatives: mostly increasing the utilisation of natural gas and building nuclear power plants

CONCLUSIONS (2/2) • In all scenarios, expenditures for energy consumers and the national economy will increase. • Furthermore, unemployment will slightly increase. • The nuclear power alternative will have a more positive impact on unemployment and the national economy than the natural gas alternative.