Download

1 / 8

80 likes | 364 Views

Use the following information for Questions 1 through 4.

E N D

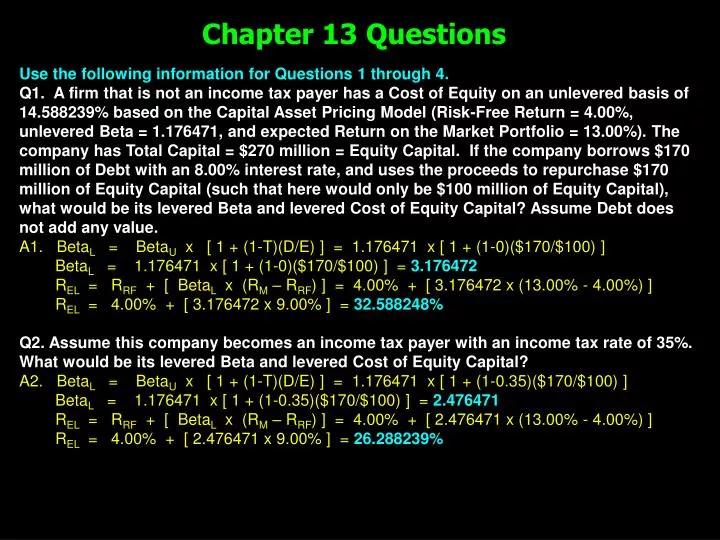

Use the following information for Questions 1 through 4. Q1. A firm that is not an income tax payer has a Cost of Equity on an unlevered basis of 14.588239% based on the Capital Asset Pricing Model (Risk-Free Return = 4.00%, unlevered Beta = 1.176471, and expected Return on the Market Portfolio = 13.00%). The company has Total Capital = $270 million = Equity Capital. If the company borrows $170 million of Debt with an 8.00% interest rate, and uses the proceeds to repurchase $170 million of Equity Capital (such that here would only be $100 million of Equity Capital), what would be its levered Beta and levered Cost of Equity Capital? Assume Debt does not add any value. A1. BetaL = BetaU x [ 1 + (1-T)(D/E) ] = 1.176471 x [ 1 + (1-0)($170/$100) ] BetaL = 1.176471 x [ 1 + (1-0)($170/$100) ] = 3.176472 REL = RRF + [ BetaL x (RM – RRF) ] = 4.00% + [ 3.176472 x (13.00% - 4.00%) ] REL = 4.00% + [ 3.176472 x 9.00% ] = 32.588248% Q2. Assume this company becomes an income tax payer with an income tax rate of 35%. What would be its levered Beta and levered Cost of Equity Capital? A2. BetaL = BetaU x [ 1 + (1-T)(D/E) ] = 1.176471 x [ 1 + (1-0.35)($170/$100) ] BetaL = 1.176471 x [ 1 + (1-0.35)($170/$100) ] = 2.476471 REL = RRF + [ BetaL x (RM – RRF) ] = 4.00% + [ 2.476471 x (13.00% - 4.00%) ] REL = 4.00% + [ 2.476471 x 9.00% ] = 26.288239% Chapter 13 Questions

Q3. Assuming this company is not an income tax payer: (1) What is its unlevered WACC? A3.(1) WACC = (E/V)(REU) + (D/V)(RD)(1-T) REU = RRF + [ BetaU x (RM – RRF) ] = 4.00% + [ 1.176471 x (13.00% - 4.00%)] REU = 4.00% + [ 1.176471 x 9.00% ] = 14.588239% WACCU = ($270/$270)( 14.588239%) + ($0/$270)(8.00%)(1-0) WACCU = 14.588239% (2) What is its levered WACC? A3.(2) WACCL = (E/V)(REL) + (D/V)(RD)(1-T) WACCL = ($100/$270)(32.588248%) + ($170/$270)(8.00%)(1-0) WACCL = (0.370370 x 32.588248%) + (0.629630 x 8.00%)(1) WACCL = 12.069709% + 5.037040% = 17.106749% Q4. Assuming this company becomes an income tax payer with an income tax rate of 35%: (1) What is its unlevered WACC? A4.(1) WACCU = (E/V)(REU) + (D/V)(RD)(1-T) WACCU = ($270/$270)(14.588239%) + ($0/$270)(8.00%)(1-0.35) WACCU = 14.588239% + 0.00% WACCU = 14.588239% + 0.00% = 14.588239% (2) What is its levered WACC? A4.(2) WACCL = (E/V)(REL) + (D/V)(RD)(1-T) WACCL = ($100/$270)(26.288239%) + ($170/$270)(8.00%)(1-0.35) WACCL = (0.370370 x 26.288239%) + (0.629630 x 8.00%)(0.65) WACCL = 9.736375% + 3.274076% = 13.010451% Chapter 13 Questions

Use the following information for Questions 5, 6, 7, 8 and 9. Assume EBIT is a proxy for Free Cash Flow before income taxes are subtracted. Assume Debt does add value. XYZ Corporation has an expected EBIT = $4,600; WACCU = 17.00%; D = $9,000; RD = 7.00%; T = 35%; Assume RA = WACCU REU = 17.00% RRF = 5.00% BetaU = 1.20 RM = 15.00% Q5. What is the Value of the firm on an unlevered basis? A5. VU = EBIT x (1 – T) = $4,600 x (1 – 0.35) = $2,990 = $17,588 RA 0.1700 0.1700 Q6. How much value would the Debt add to the company? A6. Value added by Debt = D x RD x T = D x T = $9,000 x 0.35 = $3,150 RD Q7. What is the Value of the firm on a levered basis? What is the value of the Equity on a levered basis? A7. VL = VU + Value Added by Debt = $17,588 + $3,150 = $20,738 Chapter 13 Questions

Q8. (a) What is the Cost of Equity (RE) on a levered basis (REL)? (b) What is the Debt Financing Risk Premium? A8. (a) BL = BU x [ 1 + (1-T)(D/E)] = 1.20 x [ 1 + (1- 0.35)($9,000/$11,738)] BL = 1.20 x [ 1 + (0.65)(0.766741)] = 1.20 x 1.498382 = 1.798058 REL = 5.00% + [1.798058 x (15% - 5%)] = 22.980580% (b) The Debt Financing Risk Premium = 22.980580% less 17.00% = 5.980580% Q9. What is the Weighted Average Cost of Capital on a levered basis (WACCL = RL)? A9. RAL = WACCL = [(E/V) x (RE)] + [(D/V) x (RD) x (1 – T)} RAL = WACCL = [($11,738/$20,738) x (22.980580%)] + [($9,000/$20,738) x (7.00%) x (1 – 0.35)] = [ 13.007332% ] + [ 1.975% ] = 14.982332% Chapter 13 Questions

For Q10, use the following information. Assume no change in the required return on assets (RA) irrespective of the company’s income tax position, and assume EBIT is a proxy for Free Cash Flow before any income taxes are subtracted. Assume Debt does add value. Wilson Picket Fences Inc. has an annual EBIT of $2 million and a required return on assets (RA) of 18.00%. It is subject to a 30% income tax rate, and has $5 million of Debt. Q10. What is the Value of this business on a levered basis? What is the value of the Equity on a levered basis? A10. VL = VU + [ D x T ] = EBIT x (1 – T) + [D x T] = $2 mil. x (1 – 0.30) + [$5 mil. x 0.30] RA 0.18 VL = $7.778 mil. + $1.5 mil = $9.278 million Q11. Chapter 12 is about the “Capital Structure Question”. What is this Capital Structure Question? A11. Does it create economic value for common stockholders to use Debt Capital? And, if so, How much Debt Capital should be used? Chapter 13 Questions

Q12. What are the basic Non-Economic Factors that influence the use of Debt for a company? How can using Debt impact a company’s ability to compete in the marketplace? A12. (a) Non-Economic Factors: Business Owners’ preferences for using Debt, and how a company’s Industry uses Debt. (b) Under certain conditions Debt use can lower a company’s WACC, and this means its minimum required Free Cash Flow can be lower, and this can help a company by reducing pressures to raise product prices or pay its employees lower levels of compensation (relative to its competitors). Q13. What are the basic Economic Factors that influence the use of Debt for a company? A13. -Are there any cash income tax benefits for using Debt? If not, then Debt use will have fewer, if any, economic benefits (i.e., won’t create value for common stockholders). -Debt use increases a company’s total risk, and thereby increases its Cost of Equity capital. -If a company has a high level of Business Risk, then it must have a lower level of Financial Risk (Debt use) [and vice versa]. -A company must limit its use of Debt capital to avoid bankruptcy costs, and one rule of thumb is to use a little less Debt than its industry average (assuming the use of Debt has significant economic benefits for common stockholders). Chapter 13 Questions

Q14. What “bad” things can Debt represent? What “good” things can Debt represent? A14. Bad things: -Debt usage increases a company’s total risk by making Earnings Per Share, Return on Equity, and Free Cash Flow less Debt Service Payments more variable. -Debt use means a company has some degree of bankruptcy risk -Lenders may be willing to loan a credit-worthy company more Debt than would be prudent for that company to use, and so the over-use or imprudent use of Debt becomes a strong temptation for management. -Debt use increases the Cost of Equity Capital. Good Things: -Debt Capital has a substantially lower cost than Equity Capital. -Under certain conditions Debt use can lower a company’s WACC, and thereby create substantial value for common stockholders. -Debt Capital can help a company grow faster by allowing management to invest in more business projects, and thereby grow Free Cash Flow by a higher rate (and a higher growth rate for Free Cash Flow can also create more value for common stockholders. Q15. How does the level of business risk for a company or industry influence the use of Debt for that company or that industry? Examples? A15. If the a company has a relatively high level of business/operating risk, then it must keep its level of financial risk (i.e., the use of Debt) at a relatively lower level (and vice versa, except the use of Debt is always optional). Chapter 13 Questions

Q16. Mustang Bikes Inc. makes a line of bicycles, and these bicycles sell for an average price of $1,500 each. Currently, the company employs a number of workers to make the bicycles, such that variable costs are $850 per bike and total fixed costs are $2,500,000 per year. Kerry Hall, the owner of the company, is evaluating the acquisition of a new machine which will help manufacture the bikes on a more automated basis. If the company acquires the machine, total fixed costs per year will increase to $3,800,000 but variable costs per bike will be reduced to $670 per bike. Hall is interested in the new machine but not if the Break-Even point for their company’s sales volume in units for this line of bicycles would be increased by more than 10%. If the estimates are accurate about total fixed costs and variable costs per bike, What is the new Break-Even point in bikes? Would it make sense to acquire the new machine, given their desire that the Break-Even point not be increased by more than 10%? A16. Current Operating Break-Even Point in Unit Sales = Fixed Costs_______ = $2,500,000 ($1,500 less $850) ( $650) = 3,846.1538 bikes Proposed Op. Break-Even Point in Unit Sales: = Fixed Costs _____ = $3,800,000 ($1,500 less $670) ($830 ) = 4,578.31 bikes Q. Is the new Break-Even point more than 10% higher than the current Break-Even point? = 4,578.31/ divided by 3,846.1538 = 1.1904 = 19% higher. A. Yes, it represents a 19% increase. So, no, it does not make sense given the Company’s preference not to increase its Operating Break-Even point by more than 10%. Chapter 13 Questions and Answers