Download

1 / 36

370 likes | 397 Views

Learn how to use T-bill and Eurodollar futures for speculation and hedging against changes in short-term interest rates. Dive into the intricacies of pricing and arbitrage opportunities.

E N D

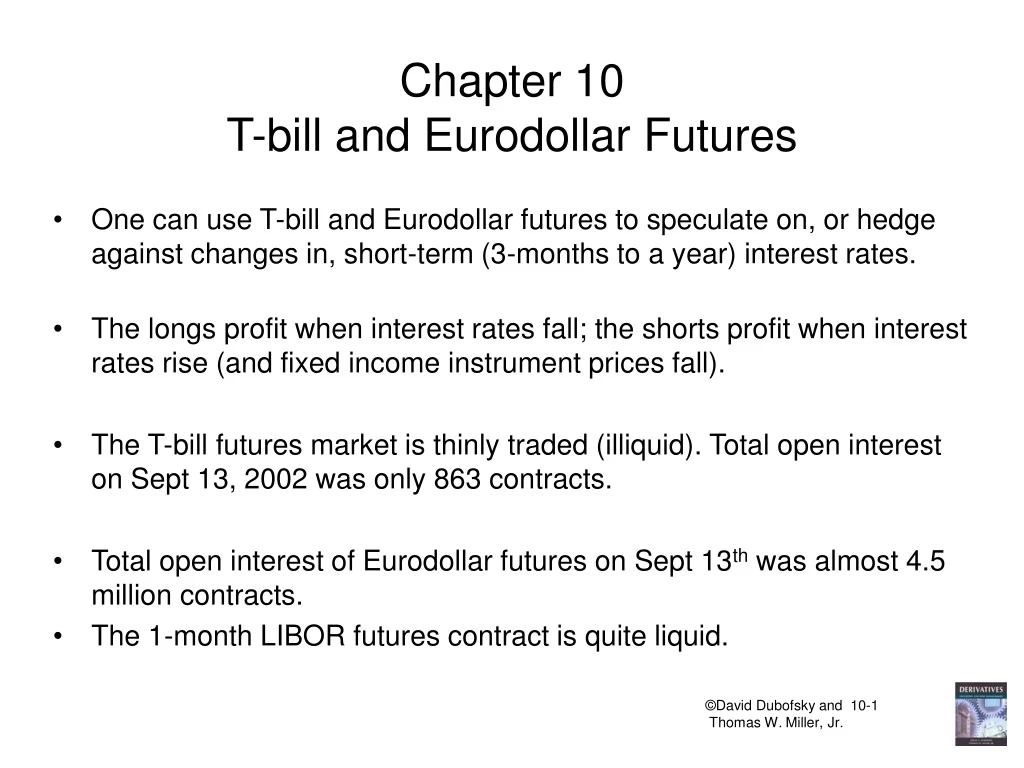

Chapter 10T-bill and Eurodollar Futures • One can use T-bill and Eurodollar futures to speculate on, or hedge against changes in, short-term (3-months to a year) interest rates. • The longs profit when interest rates fall; the shorts profit when interest rates rise (and fixed income instrument prices fall). • The T-bill futures market is thinly traded (illiquid). Total open interest on Sept 13, 2002 was only 863 contracts. • Total open interest of Eurodollar futures on Sept 13th was almost 4.5 million contracts. • The 1-month LIBOR futures contract is quite liquid.

T-bill Futures, I. • Underlying asset is $1MM face value of 3-month Tbills • IMM Index = 100 – dy • dy is the forward discount yield on a 3 month T-bill: Where: F = face value = $1,000,000 for a T-bill futures contract P = price t = days to maturity (91 days for a 3-month T-bill) (A surprisingly difficult formula!)

T-bill Futures, II. • Note that the discount yield is not a rate of return. • If the day count method is actual/365, the annualized rate of return, r, with simple interest, is • This is called the bond equivalent yield (if t < 182 days)

T-bill Futures, III. • The futures discount yield is the forward yield on a 3-month T-bill, beginning on the delivery date of the contract. Example: • Suppose today is October 8, the delivery day for the Dec contract is Dec. 18th, and the futures price is 97.22. • Then, someone who goes long a T-bill futures contract has “essentially” agreed to buy $1 million face value of 3-month T-bills on Dec. 18th, at a forward discount yield of 2.78%, which is a forward price of $992,972.78. • One tick = $12.50 = 1/2 basis point change in the yield. • The contract is cash-settled. • To speculate, go long T-bill futures if you think that 3-month T-bill prices will rise (yields on 3-month T-bills will fall). Sell T-bill futures to bet on falling prices (rising yields).

T-bill Futures Pricing, I. • Cash and carry arbitrage: borrow (until delivery), buy the T-bill that will have 3 months to maturity on the delivery date, and sell the futures contract. • Reverse cash and carry arbitrage: buy the cheap futures contract, sell short the deliverable T-bill (borrow), and lend the proceeds until delivery. • Remember that the deliverable T-bill will have 3 months to maturity on the delivery day of the futures contract. If there are t1 days until delivery, then today, the deliverable T-bill has t1+91 days to maturity. • (BTW, The same arbitrage concepts hold for Eurodollar futures.)

T-bill Futures Pricing, II. • Buying T-bill futures = agreement to lend money to the US government in the future. Sell T-bill futures = agreement to borrow in the future. • Refer to Section 5.3. You can create forward borrowing and lending situations by using spot pure discount debt instruments, such as T-bills. • The two forward rates should be equal, or else there will be an opportunity to arbitrage. • (BTW, The same concepts hold for Eurodollar futures.)

Eurodollar Futures, I. • When foreign banks receive dollar deposits, those dollars are called Eurodollars. • Underlying asset is the 90-day $1,000,000 Eurodollar time deposit interest rate; LIBOR • Cash settled • IMM Index = 100 – aoy • aoy = add on yield on a 90-day forward Eurodollar time deposit (LIBOR). • If the IMM Index is 95.19, then the futures LIBOR is 4.81%.(100 – 95.19 = 4.81) • LIBOR rises => IMM index falls. (A surprisingly difficult formula!)

Eurodollar Futures, II. • 1 tick = 0.5 basis point in 3-month futures LIBOR = $12.50 (0.25 basis point = $6.25 for the spot month contract). • To speculate that LIBOR will rise, sell Eurodollar futures (declining prices of debt instruments mean rising interest rates). • To profit if short term interest rates fall, buy Eurodollar futures. • Four months prior to the delivery date, a Eurodollar futures contract is ~ to a 4X7 FRA. • 12 months prior to delivery a Eurodollar futures contract ~ 12X15 FRA.

Eurodollar Futures, III. • Through the first six months of 2002, CME 3-month Eurodollar futures were the 2nd most actively traded futures contract in the world, with over 106 million contracts traded. • This great success is attributable to: • The size of the spot Eurodollar market is enormous, estimated to be in the $trillions. • Buyers and sellers of money market instruments that possess a default risk premium find that Eurodollar futures yields are more highly correlated with yields on their spot securities than T-bill yields. • Eurodollar futures are effective at hedging short-term interest rate exposure.

Hedging With Eurodollar Futures • If a firm holds a spot position that will experience losses if short-term interest rates rise (prices of debt instruments fall), then this short hedger will sell short-term interest rate futures contracts. • If an individual holds a cash position that will experience losses when short term interest rates fall, then this long hedger will buy short-term interest rate futures contracts. • Thus, the hedger must first identify whether higher or lower interest rates are feared. • Then the proper futures contract(s) to trade must be determined. • Finally, the "proper" number of futures contracts to be bought or sold (the hedge ratio) must be determined.

Eurodollar: Futures Settlement Prices as of 07/28/99 http://www.cme.com

Locking in a Single-Period Borrowing Rate Using Eurodollar Futures • On July 28, 1999, a firm plans to borrow $50 million for 90 days, beginning on September 13, 1999. • The firm will borrow at the Eurodollar spot market on September 13th. • (For ease of presentation, the loan begins on the expiration date of the September futures contract, September 13, 1999. Loans beginning on any other date will mean that the hedge possesses some basis risk.) • The current spot 3-month Eurodollar rate is 5.3125%. • However, this rate does not matter to the firm because the bank will not be borrowing at the current spot 3-month rate. • timelinetimelinetimelinetimelinetimelinetimelinetimelinetimeline. Subliminal Hint

The firm will be borrowing in the spot market 47 days hence. Thus, on July 28th, the interest rate at which the firm will be borrowing on September 13th is unknown. • The firm fears that when it comes time to borrow the funds in the Eurodollar spot market, interest rates will be higher (Eurodollar Index will be lower). • Such a situation calls for a short hedge using Eurodollar futures contracts. (Why does it call for a short hedge?) • On July 28, 1999, the closing price for September Eurodollar futures was 94.555. (IMM Index) • Assuming transactions costs of zero, by shorting 50 Eurodollar futures contracts on July 28, 1999, the firm can lock in a 90-day borrowing rate of 5.445%. • Rate: 100 – 94.555.

Case I. Spot 90-Day LIBOR on September 13th is 5.445%. • The firm’s interest expense would be: $680,625 = 50,000,000 * 0.05445 * (90/360) • Because September 13th is the settlement date for the Eurodollar futures contract, the futures price will equal the spot price, the 90-day LIBOR rate. (Why?) • Thus, in this case, there is no profit or loss on the futures contracts because the firm went short at 94.555.

Case II. Spot 90-Day LIBOR on September 13th is 5.845%. • Here, the bank’s actual interest expense would be higher than “anticipated” because interest rates rose above the original futures interest rate: $730,625 = 50,000,000 * 0.05845 * (90/360) • To calculate the futures profit on the 50 contracts, one must recall that each full point move in the IMM Index (i.e., 100 basis points) represents $2,500 for one futures contract. The delivery day futures price is 100-5.845 = 94.155. Thus, (94.555 – 94.155) * 2500 * 50 = $50,000 • Here too, the net interest expense for the firm is $730,625 - $50,000 = $680,625.

Case III. Spot 90-Day LIBOR on September 13th is 5.045%. • The bank’s actual interest expense would be: $630,625 = 50,000,000 * 0.05045 * (90/360) • However, because interest rates are lower, the bank loses on its short futures position. The delivery day futures price is 100-5.045 = 94.955. The futures loss is (94.555 – 94.955) * 2500 * 50 = ($50,000) • The net interest expense for the firm equals the interest expense with the 5.045% rate, plus the loss on the futures position. It is the same as the two previous cases: $630,625 + $50,000 = $680,625.

An Important Note on Basis Risk • It is important to note that the firm has removed basis risk from these transactions because the loan commenced on the futures expiration date. • This example shows that no matter what the spot rate is in 47 days, the firm can protect itself from higher rates. • Note that part of the cost of this protection is the foregone opportunity to make more money if rates fall.

Locking in a Multi-Period Borrowing Rate Using Eurodollar Futures: A Strip Hedge • Now suppose that on July 28, 1999, the firm plans to borrow $50 million for one year, beginning on September 13, 1999. • The firm plans to borrow in the spot Eurodollar market. • If the firm chooses to borrow quarterly, the firm would likely use a portfolio of 90-day Eurodollar futures contracts to hedge this borrowing cost, and it has two basic choices in the way it could hedge against increases in quarterly borrowing rates. • They are a strip hedge and a stack hedge (frequently called a rolling hedge). • To execute a strip hedge, the bank would sell 200 Eurodollar futures contracts: 50 in each of fourdifferentdelivery months. (To execute a stack hedge, the bank would initially sell 200 futures contracts in one delivery month.) • We will focus on an example of a strip hedge.

Because the firm will borrow $50 million in September and every 90 days three times thereafter, the firm initiates a strip hedge by selling 50 Eurodollar futures contracts in each of four delivery months: September, December, March, and June. • The short positions in these 200 futures contracts are all entered on July 28th. • Thus, a strip hedge can be thought of as a portfolio of single-period hedges. • In the strip hedge shown below, the hedger has hedged borrowing costs for four successive quarters. • In the following table, rates and prices that are known on July 28th appear in bold italics. • In this example, note that the firm faces a new loan rate at the start of each of four successive 90-day loan periods. • As an example of how to read the table, “S50@94.555” means go short 50 contracts at a futures price of 94.555, and “L50@ 94.35” means go long 50 contracts at a futures price of 94.35.

Strip Hedge Using Eurodollar Futures Spot 3-mo. Date LIBOR Sept. 1999 Dec. 1999 March 2000 June 2000 7/28/1999 5.3125% S50@94.555S50@94.19S50@94.185 S50@93.95 9/13/1999 5.65% L50@ 94.35 12/13/1999 5.85% L50@94.15 3/13/2000 6.00% L50@94.00 6/19/2000 5.90% L50@94.10 Futures LIBOR rate: 5.445% 5.81% 5.815% 6.05% (on 7/28/99) Gain (Loss) in Euro$ Futures: $25,625 $5,000 $23,125 ($18,750)* *The $18,750 loss occurs because the June 2000 futures price rose from 93.95 to 94.10. This is a loss of 15 ticks. Each tick is worth $25. The firm sold 50 futures contracts. Therefore, 15 ticks * $25/tick * 50 contracts = -$18,750.

Strip Hedge Summary and Introduction to Bundles and Packs • The effective borrowing rate for each quarter is the implied futures rate at the time the hedge is placed. • This can be assured only if the firm borrows on each of the futures contracts’ delivery days. • This is just as it is in the one-period case above. • Thus, one can see that a strip hedge is a portfolio of one-period hedges. • To expedite the execution of strip trades the CME offers bundles and packs for Eurodollar futures. • Bundles and Packs are simply "pre-packaged" series of contracts that facilitate the rapid execution of strip positions in a single transaction rather than constructing the positions with individual contracts.

Eurodollar Bundles and Packs • Bundles: The simultaneous sale or purchase of one each of a consecutive series of Eurodollar contracts. • There are 1,2,3,5,7, and 10-year Eurodollar Bundles available for trading. • For example, a two-year bundle consists of the first eight Eurodollar contracts. • A five-year "forward" bundle, which is composed of the twenty Eurodollar contracts from years six through ten, is also listed. • Packs: Asimultaneous purchase or sale of an equally weighted, consecutive series of Eurodollar futures. The number of contracts in a pack is fixed at four. • Packs are designated by a color code that corresponds to their position on the yield curve. For example, the red pack consists of the four contracts that constitute year two on the curve, the green pack those in year three, etc. There are nine Eurodollar packs (covering years two through ten) available for trading at a given time. • Distant Contract Liquidity makes identification impossible. • CME color codes: Years one (contracts 1-4) through ten (contracts 37-40) are represented, respectively, by: white, red, green, blue, gold, purple, orange, pink, silver, and copper.

Some Extra Slides on this Material • Note: In some chapters, we try to include some extra slides in an effort to allow for a deeper (or different) treatment of the material in the chapter. • If you have created some slides that you would like to share with the community of educators that use our book, please send them to us!

We Will Begin with a Review of Some Interest Rate Basics • In Particular, we need to internalize two sets of interest rates. • The Zeros. • The Forwards. • Hint: There is a relationship between them, that is best seen via a timeline.

Out of Many Interest Rates, one is Named the Zero Rate. (Collectively, the Group of Zero Rates are Called ‘the Zeros’.) • A zero rate from time 0 to maturity T, is the rate of interest earned on an investment that provides a payoff onlyat time T. (think of a zero-coupon bond). • Because these rates are quoted today, i.e., at time 0, they are also known as spot rates. • Although sometimes we must calculate these, zeros are not mythical creatures. • Treasury STRIPS.

Out of Many Rates, one is Named the Forward Rate. (Collectively, they are ‘the Forwards’.) • The forward rate is the future zero rate implied by today’s term structure of zero interest rates. • Expectations Theory of the Term Structure: forward rates equal expected future zero rates.

Calculating Forward Rates Zero Rate for Forward Rate n n an -year Investment for th Year n Year ( ) (% per annum) (% per annum) 1 10.0 2 10.5 11.0 3 10.8 11.4 4 11.0 11.6 5 11.1 11.5

A Handy Formula for Forward Rates: • Suppose that the zero rates for time periods T1and T2are R1 and R2 with both rates continuously compounded. • The forward rate for the period between times T1 and T2 is:

Example: Calculating a Forward Rate, I. T: 0 1 2 3 10.0% f1,2% 10.5% f2,3% 10.8%

Example of Calculating the Forward Rate with Periodic Interest Rates • With Annual Rates:

Short Hedge Situations Using Eurodollar Futures • A manager of a portfolio consisting of short-term debt securities fears that a rise in short term interest rates will cause the value of the portfolio to decline. • A bank makes a one year fixed rate loan, and funds it with 90 day negotiable CD's. After 90 days, the bank will have to return to the credit market to borrow for another 90 days. It fears interest rates will be higher at that date. • A bank plans to issue CD's, or a corporation plans to sell commercial paper (or take out any short term loan) in the near future. • An individual buys a house, but the bank will not guarantee his mortgage rate until the loan is approved, which will be in six weeks. His loan rate is tied to a short-term Treasury security index. • An institution plans on selling a part of its investment portfolio of money market investments to meet an upcoming cash requirement. • A government securities dealer who is carrying an inventory of T-bills fears that a rise in interest rates will lower its value. • A firm has an existing variable rate loan, and next week, the interest rate will be reset.

Long Hedge Situations Using Eurodollar Futures • A bank or firm wishes to purchase six month CD's as an investment, but either there is a temporary insufficient supply of these securities, or the bank or firm temporarily lacks the cash needed to make the purchase. • A portfolio manager knows that $X million will be received at the end of this month for investment in short-term securities. Current yields are very attractive, and the manager fears interest rates will fall between today and the day that the funds will be received. • A bank makes a variable rate loan that is financed with a longer term CD.