Download

1 / 25

250 likes | 385 Views

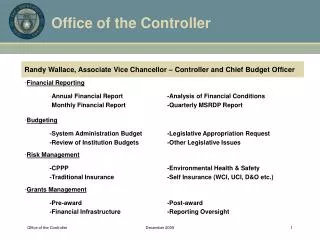

Office of the Controller and Internal Controls. Sandra Featherson Associate Director of Controls Office of the Controller February 2010. Abbreviated Organization Chart. Henry T. Yang Chancellor. Anne Broome Vice President, Financial Management, UCOP. Sheryl Vacca

E N D

Office of the Controller and Internal Controls Sandra Featherson Associate Director of Controls Office of the Controller February 2010

Abbreviated Organization Chart Henry T. Yang Chancellor Anne Broome Vice President, Financial Management, UCOP Sheryl Vacca Senior Vice President/Chief Compliance and Audit Officer, UCOP Vacant Vice Chancellor, Administrative Services Vacant University Auditor Ron Cortez Associate Vice Chancellor, Administrative Services Jim Corkill, Controller, Accounting Services and Controls Craig Whitebirch Director, Audit and Advisory Services

Office of the Controller Provide leadership in a campus-wide effort to ensure effective controls and accountability practices. Assist management in assessing their control environment and the effectiveness and efficiency of operations. Ensure that campus financial policies and procedures are clear, adequate, and current. Evaluate systems and participate in system development to ensure proper controls are implemented and compliance with policy. Audit and Advisory Services Independent evaluation of systems of accountability and control. Investigate reported cases of alleged improper financial activities. Serve as the liaison between the University community and external audit agencies. Distinct and Complimentary Roles

Business Officer Institute (BOI) • BOI Feedback • Common Audit Findings Control Advisory Committee (CAC) Financial Risk Assessment Campus Financial Mgmt. Training & Manual Departmental Control Self- Assessments Departmental Process Risk Assessment Campus Wide Process Risk Assessment UCSB Control Initiative

Assessments • Departmental Control Self Assessments • Departmental Process Risk Assessment • Campus Wide Process Risk Assessment

Office of the Controllerhttp://controller.ucsb.edu • Jim Corkill Controller Director of Accounting Services and Controls x5882 jim.corkill@accounting.ucsb.edu • Sandra Featherson Associate Director of Controls x7667 sandra.featherson@accounting.ucsb.edu • Neil Clark Administrative Analyst x8593 neil.clark@accounting.ucsb.edu • Tonika Jones Administrative Assistant x8593 tonika.jones@accounting.ucsb.edu

Internal Controls • What are Internal Controls? • Definition • COSO Model • Examples • Why are They Important? • Who is Responsible for Internal Controls?

Internal Control - A definition • Internal Control is a process, effected by a college or university’s governing board, administration, faculty and staff, designed to provide reasonable assurance regarding achievement of objectives in the following areas: • Effectiveness and efficiency of operations • Reliability of financial reporting • Compliance with applicable laws and regulations Internal Control Concepts & Applications, 1992, Committee of Sponsoring Organizations of the Treadway Commission

COSO Internal Control Model • COSO stands for Committee of Sponsoring Organizations. • Committee was formed to develop a common definition of internal controls and provide guidance on judging its effectiveness. • COSO is referred to as an Internal Control Model or framework.

COSO Internal Control Model • Officially adopted by the University of California • A tool for departments to use in evaluating their internal controls.

COSO Internal Control Model There are five components of internal control in the COSO Model: • Control Environment • Risk Assessment • Control Activities • Information and Communication • Monitoring

Control Environment Control Environment • The “tone at the top” set by people in positions of authority • Based on attitudes and habits of those in authority • An element in establishing the organizational culture

Control Environment Control Environment Factors: • Integrity and Ethical Values • Commitment to Competence • Management’s Philosophy andOperating Style • Assignment of Authority andResponsibility

Risk Assessment • Risk - Anything that gets in the way of meeting your goal/objective • Risk Assessment - The identification and analysis of relevant risks associated with achieving business goals/objectives

Risk Assessment • Why is a risk assessment important? • Risks impact an organization’s ability to meet its objectives such as: • Positive Public Image • Providing Excellent CustomerService • Reducing Overdrafts

Control Activities • Control Activities • Policies and procedures that help ensure management directives are carried out and necessary actions are taken to address risks

Control Activities - Specific Examples • Segregation of Duties • Transaction Reviews • Reconciliations

Control Activities – Specific Examples • Financial Performance Reviews • Systems Controls • Physical Controls • Case Study

Information and Communication The information system must provide data that is: • Relative to established objectives • Accurate and in sufficient detail • Understandable and in a usable form This information must be provided to the right people in time to allow appropriate action

Information and Communication Communication • Up and down the organization • Across organizational lines Communication Examples • Employee duties and control responsibilities should be clearly communicated • Ability to report suspected problems, without fear of repercussions

Monitoring Monitoring • A process that assesses the quality of an internal control system’s performance over time

Monitoring Monitoring Activity Examples • Management • Review of actual expenditures vs. budgeted • Comparison of various reports with physical assets • Separate evaluations • Assessment of internal controls by Audit and Advisory Services • External auditors reviews

Internal Controls • Why are They Important? • Who is Responsible for Internal Controls?

Internal Controls and SAS 112 • SAS 112: Statement of Accounting Standards • Auditors will be reviewing not only the transactions and ensuring the numbers are correct, but also the controls in place to ensure those numbers are correct. • Controls must be documented – or they are not considered controls.