Download

1 / 11

130 likes | 294 Views

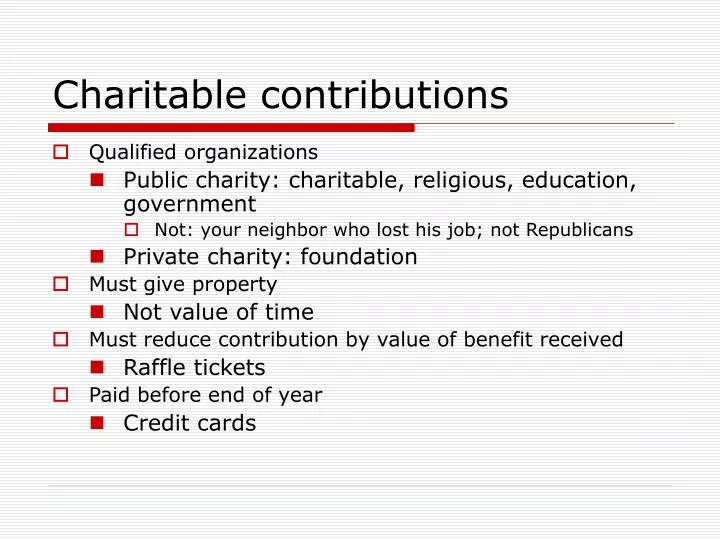

Charitable contributions. Qualified organizations Public charity: charitable, religious, education, government Not: your neighbor who lost his job; not Republicans Private charity: foundation Must give property Not value of time Must reduce contribution by value of benefit received

E N D

Charitable contributions • Qualified organizations • Public charity: charitable, religious, education, government • Not: your neighbor who lost his job; not Republicans • Private charity: foundation • Must give property • Not value of time • Must reduce contribution by value of benefit received • Raffle tickets • Paid before end of year • Credit cards

Amount deductible • Chart on Page 126 • Cash • 50%: public charity • Carryover for five years • Capital gain property: deduct FMV • 30%: public charity • Carryover for five years • Elect 50% limit if use cost instead of FMV

Amount deductible • Tangible personal property • Related use: deduct FMV • 30%: public charity • Carryover for five years • Elect 50% limit if use cost instead of FMV • Unrelated use: deduct cost • 50%: public charity • Carryover for five years • Ordinary income property: deduct cost • 50% • Carryover for five years

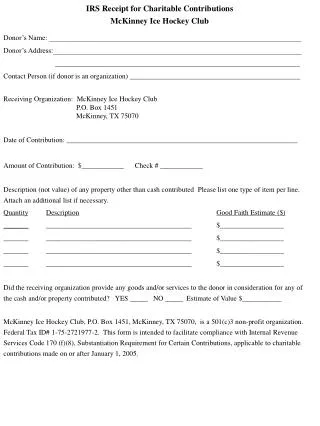

Substantiation • Must have: • a bank record (check) for contribution or • documentation from charity • No deduction for: • Cash contributions to • Salvation Army • Church? • They generally will provide documentation

Substantiation • Noncash contributions • Over $500: attach Form 8283 including description • No deduction for used underwear

IRA Contributions • Must be over 70 ½ • Can contribute up to $100,000 per person in 2007 • Why do this? • Income tax savings • RMD • AGI limits • Estate tax savings

Charitable Trusts • Contribute appreciated property to trust • No income tax on capital gain • Receive income for life • Get a charitable deduction for value of remainder interest • Value of gift – PV annuity payments • Old person: value of remainder is large

Charitable Trusts • Donor is happy • No tax on gain • Charitable deduction for remainder interest • Income for life • Asset is removed from estate • Charity is happy • Heirs are sad • Buy life insurance in ILIT to replace value of asset transferred to charity

Trusts • CRAT • Pays fixed amount or percentage of initial value to noncharitable benficiary • Must be at least 5% • Similar to a bond • Remainder goes to charity • Versus lead trust • Value of remainder interest • Must be at least 10% of value of assets transferred to trust

Trusts • CRUT • Pays fixed amount or percentage of annual value to noncharitable benficiary • Must be at least 5% of annualvalue • Equity interest • Remainder goes to charity • Versus lead trust • Value of remainder interest • Can add assets to a CRUT; not CRAT

Pooled income fund • Combined with contributions of other individuals • Donor retains life interest • Receive annual income based on performance of fund • Remainder goes to charity • Value of remainder interest