Download

1 / 76

860 likes | 1.22k Views

Chapter 14 - Raising Capital in the Financial Markets. Chapter 15 – Analysis and Impact of Leverage. Tujuan Pembelajaran 1. Mahasiswa Mampu untuk : Memahami sumber dana internal dan eksternal Memahami bauran pembiayaan yang cenderung digunakan perusahaan

E N D

Chapter 14 - Raising Capital in the Financial Markets Chapter 15 – Analysis and Impact of Leverage

TujuanPembelajaran 1 • MahasiswaMampuuntuk: • Memahamisumberdanainternal dan eksternal • Memahamibauranpembiayaan yang cenderungdigunakanperusahaan • Menjelaskanmengapa pasar keuangantimbul • Menjelaskankomponensistem pasar keuangan • Memahamiperanbankirinvestasidalamperolehan modal • Membedakanantarapenawaranterbatasdanpenawaranumum

PokokBahasan 1 • Sumberdanainternal dan eksternal • Bauransekuritasperusahaan yang dijual di pasar modal • Mengapa pasar keuanganmuncul • Pembiayaanperusahaan • Komponensistem pasar keuangan • Bankirinvestasi • PenawaranterbatasdanPenawaranumum

TujuanPembelajaran 2 • Mahasiswamampuuntuk: • Memahamiperbedaan antara risikokeuangan dan risikobisnis • Menggunakanteknikanalisistitikimpasuntukberbagaijenisanalisis • Membedakankonsepkeuangandari leverage operasi, leverage keuangan, danleveragegabungan • Menghitungdegree of operatingleverage, financialleverage, dan combinedleverage

PokokBahasan 2 • Risikobisnis dan keuangan • Analisistitikimpas • Operatingleverage • Financialleverage • Kombinasioperatingleverage dan financialleverage

Q: What are SECURITIES? A: Financial Assets that Investors purchase hoping to earn a high rate of return.

Types of Securities • Treasury Bills and Treasury Bonds • Municipal Bonds • Corporate Bonds • Preferred Stocks • Common Stocks Which of these are RISKY? Which promise HIGH RETURNS? Is there a relationship betweenRISK and RETURN?

Corporate FinancingSources From 1999 through 2001, capital has been raised through the following sources: • Corporate Bonds and Notes 76.9% • Equities 23.1%

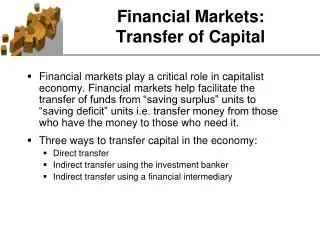

cash saver securities Movement of Savings • Direct Transfer of Funds firm

funds funds saver investment banker firm securities securities Movement of Savings • Indirect Transfer using Investment Banker

funds funds financial intermediary saver firm intermediary securities firm securities Movement of Savings • Indirect Transfer using a Financial Intermediary

Financial Market Components Public Offering • Firm issues securities, which are made available to both individual and institutional investors. Private Placement • Securities are offered and sold to a limited number of investors.

Financial Market Components Primary Market • Market in which new issues of a security are sold to initial buyers. Secondary Market • Market in which previously issued securities are traded.

Financial Market Components Money Market • Market for short-term debt instruments (maturity periods of one year or less). Capital Market • Market for long-term securities (maturity greater than one year).

Financial Market Components Organized Exchanges • Buyers and sellers meet in one central location to conduct trades. Over-the-Counter (OTC) • Securities dealers operate at many different locations across the country. • Connected by Nasdaq system (National Association of Securities Dealers Automated Quotation system).

Investment Banking How do investment bankers help firms issue securities? • Underwriting the issue. • Distributing the issue. • Advising the firm.

Distribution Methods Negotiated Purchase • Issuing firm selects an investment banker to underwrite the issue. • The firm and the investment banker negotiate the terms of the offer. Competitive Bid • Several investment bankers bid for the right to underwrite the firm’s issue. • The firm selects the banker offering the highest price.

Distribution Methods Best Efforts • Issue is not underwritten. • Investment bank attempts to sell the issue for a commission. Privileged Subscription • Investment banker helps market the new issue to a select group of investors. • Usually targeted to current stockholders, employees, or customers.

Distribution Methods Direct Sale • Issuing firm sells the securities directly to the investing public. • No investment banker is involved.

Stock Issue Example: Our firm needs to raise approximately $100 million for expansion. Our stock price is $20. We Select Merrill Lynch to underwrite the issue for a 2% underwriting spread. • What type of issue is this? • It’s a negotiated purchase.

Stock Issue Example: Our firm needs to raise approximately $100 million for expansion. Our stock price is $20. We Select Merrill Lynch to underwrite the issue for a 2% underwriting spread. • How many shares will be sold? • $100,000,000 / $20 = 5 million new shares of common stock.

Stock Issue Example: Our firm needs to raise approximately $100 million for expansion. Our stock price is $20. We Select Merrill Lynch to underwrite the issue for a 2% underwriting spread. • What are the flotation costs? • Underwriting spread: 2% of $100 million = $2 million. • Issuing costs: printing and engraving costs; legal, accounting, and trustee fees.

Stock Issue Example: Our firm needs to raise approximately $100 million for expansion. Our stock price is $20. We Select Merrill Lynch to underwrite the issue for a 2% underwriting spread. • What are the risks? • The investment bank accepts the risk of being able to sell the new stock issue for $20 per share. If the stock price falls, the investment bank could lose money.

Regulations:The Primary Market The Securities Act of 1933 • Firms register with the Securities Exchange Commission (SEC). • SEC has 20 days to review. • SEC may ask for more information. • The firm cannot solicit buyers during the review period but can advertise.

Regulations:The Secondary Market The Securities Exchange Act of 1934 • Established the SEC. • Exchanges must register with SEC. • Company information must be available to the public. • Insider trading is regulated.

Regulations:Recent Developments Securities Acts Amendments of 1975 • Created National Market System. • Eliminated fixed brokerage commissions. SEC Rule 415 • Allows Shelf Registration

Chapter 15 – Analysis and Impact of Leverage • Operating Leverage • Financial Leverage

Two concepts that enhance our understanding of risk... 1) Operating Leverage - affects a firm’s business risk. 2) Financial Leverage - affects a firm’s financial risk.

Business Risk • The variability or uncertainty of a firm’s operating income (EBIT).

Stock- holders FIRM EPS EBIT Business Risk • The variability or uncertainty of a firm’s operating income (EBIT).

Business Risk Affected by: • Sales volume variability • Competition • Product diversification • Operating leverage • Growth prospects • Size

Operating Leverage • The use of fixed operating costs as opposed to variable operating costs. • A firm with relatively high fixed operating costs will experience more variable operating income if sales change.

EBIT Operating Leverage

Financial Risk • The variability or uncertainty of a firm’s earnings per share (EPS) and the increased probability of insolvency that arises when a firm uses financial leverage.

Stock- holders FIRM EPS EBIT Financial Risk • The variability or uncertainty of a firm’s earnings per share (EPS) and the increased probability of insolvency that arises when a firm uses financial leverage.

Financial Leverage • The use of fixed-cost sources of financing (debt, preferred stock) rather than variable-cost sources (common stock).

EPS Financial Leverage

Breakeven Analysis • Illustrates the effects of operating leverage. • Useful for forecasting the profitability of a firm, division, or product line. • Useful for analyzing the impact of changes in fixed costs, variable costs, and sales price.

Total Revenue $ Quantity

Costs Suppose the firm has both fixed operating costs (administrative salaries, insurance, rent, property tax) and variable operating costs (materials, labor, energy, packaging, sales commissions).

Total Revenue Total Cost $ } EBIT + - { FC Quantity Q1

} EBIT Total Revenue Total Cost $ + - { FC Quantity Q1 Break-even point

Operating Leverage What happens if the firm increases its fixed operating costs and reduces (or eliminates) its variable costs?

Total Revenue } $ EBIT + { Total Cost = Fixed - FC Quantity Q1 Break-even point

With high operating leverage, an increase in salesproduces a relatively larger increase in operating income.

Total Revenue } $ EBIT + { Total Cost = Fixed - FC Q1 Quantity Break- even point

Total Revenue } $ EBIT + { Total Cost = Fixed - FC Q1 Quantity Break- even point Trade-off: the firm has a higher breakeven point. If sales are not high enough, the firm will not meet its fixed expenses!

F P - V QB = Breakeven Calculations Breakeven point (units of output) • QB = breakeven level of Q. • F = total anticipated fixed costs. • P = sales price per unit. • V = variable cost per unit.