Download

1 / 34

460 likes | 782 Views

EMPIRICAL TESTS OF THE CAPITAL ASSET PRICING MODEL. THE BLACK, JENSEN, AND SCHOLES TEST (1972). We know that if the market portfolio is efficient, it follows automatically that a linear, positively sloped relationship exists between betas and expected rates of return.

E N D

THE BLACK, JENSEN, AND SCHOLES TEST (1972) • We know that if the market portfolio is efficient, it follows automatically that a linear, positively sloped relationship exists between betas and expected rates of return. • If investors can borrow and lend at a risk-free rate, it also follows that a zero beta stock or portfolio can be expected to produce a return equal to the risk-free rate. • The empirical test of BLACK, JENSEN, AND SCHOLES (BJS) is designed to test these properties of the security market line

Sample: • All stocks traded on the New York Stock Exchange during the period 1926 through 1965. • Methodology • They started their study with the sub-period 1926-1930. • They calculated beta for all stocks during the sub-period (Market index = an equally weighted portfolio of all stocks on the NYSE). • They then ranked the stocks on the basis of beta and form 10 portfolios.

The 10 percent of the stocks with the highest betas go into portfolio 1 and so on, through portfolio 10. • Portfolio 1: 10 percent of the stocks with the highest betas • Portfolio 2: 10 percent of the stocks with the second highest betas • Portfolio 3: 10 percent of the stocks with the third highest betas • . • . • . • . • . • . • Portfolio 10: 10 percent of the stocks with the lowest betas

They now computed the rates of return to each of the portfolios in each of the 12 months of 1931 www.pptmart.com

At the end of the year 1931 they again calculated beta for all stocks during the sub-period (1927-1931). • They then ranked the stocks on the basis of beta and form 10 portfolios. • The 10 percent of the stocks with the highest betas go into portfolio 1 and so on, through portfolio 10.

They now compute the rates of return to each of the portfolios in each of the 12 months of 1932 www.pptmart.com

BJS repeated this process in each of the years 1931 through 1965 (total 35 years).Obtained a series of 35 x 12= 420 monthly rates of returns for each of 10 portfolios. www.pptmart.com

They now attempted to estimate the expected rates of return and beta factors. • The sample estimate of the expected value is the A.M. rate of return. • They estimate the beta of each portfolio by relating the portfolio returns to their market index.

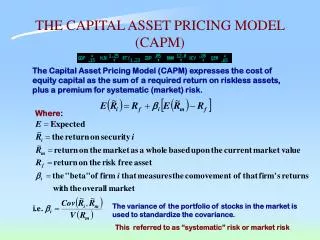

The relationship they find between beta and average rate of return is depicted in the following figure Average monthlyreturn • .00513Slope = 0.01081 • Beta

The slope of the BJS estimated security market line is .01081, reflecting a market risk premium of 1.081 percent per month or 12.972 percent per year. • The intercept of the estimated security market line is .00519, reflecting a rate of return of .519 percent per month or 6.228 percent per year. • This number is significantly greater than the average interest rate on riskless bonds during the overall period. • BJS concluded that their results are consistent with the form of the CAPM that allows for riskless lending but precludes riskless borrowing.

THE FAMA-MACBETH (FM)STUDY (1974) • Like BJS, the finding of FM is again consistent with the form of the CAPM where lending at the risk-free rate is permitted but borrowing is precluded. • The results of both these tests are comforting. In fact, the CAPM gained much support among academics as well as professionals after their publication. However, the honeymoon was short-lived as we shall see in the next studies.

Different studies with their findings www.pptmart.com

Different studies with their findings www.pptmart.com

Different studies with their findings www.pptmart.com

Fama and French (1992) • Their bottom line results are • (a) beta does not seem to help explain the cross-section of average stock returns • (b) the combination of size and book-to-market equity seems to absorb the roles of leverage and E/P in average stock returns, at least during their 1963-1990 sample period

The Fama-French Three-Factor Model • Ri-Rf = ai + bi(RM –Rf) + siSMB + hiHML + εi • Return is explained by three factors: • Market factor (marker index) • Size factor (market capitalization) • Book- to-market ratio (Book Equity/Market Equity)

The additional factors are empirically motivated by the observations that historical-average returns on stocks of small firms and on stocks with high ratios of book equity to market equity (B/) are higher than predicted by the security market line of the CAPM.

To create portfolios that track the firm size and book-to-market factors, Davis, Fama, and French (2000) sorted firms annually by size (market capitalization) and by book-to-market (B/M) ratio. • The small-firm group (S) :all firms with 33% lowest market capitalization. • Medium firm group (M) :all firm with next 34%. • Big-firm group (B):all firm with 33% highest market capitalization

Similarly, firms are annually sorted into groups based on (B/M) ratio. • A low-ratio group (L) with 33% lowest B/M ratio • A medium-ratio group (M) with next 34% • A high ratio group (H) with 33% highest B/M ratio. • A high ratio firm is called value firm and the low ratio firm is called growth firm.

The intersections of the three size groups with three ratio groups results in nine group of firms. www.pptmart.com

Nine such portfolios were constructed each year throughout the period from July 1929 to June 1997 and the monthly returns of each were recorded. • This procedure generated nine time series of 816 monthly returns for the period.

For each year, the size premium (SMB) is constructed as the difference in returns between small and large firms. • Monthly SMS (small minus big) is calculated from the monthly returns of the six portfolios as • SMS = 1/3(S/L +S/M + S/H) – 1/3 (B/L + B/M +B/M)

Similarly, the book-to-market effect is calculated from the difference in returns between high B/M ratio and low B/M ratio firms. • The monthly values of HML were calculated from the monthly returns on the low and high B/M portfolios as • HML = 1/3(S/H +M/H + B/H)-1/3(S/L +M/L+B/L)

The monthly returns on the market portfolio were calculated from the value-weighted portfolio of all firms listed on the NYSE, AMEX, and NASDAQ. • The risk-free rate was the return on 1-month T/bills. • Regression equations of the three factor models for nine portfolios were run.

Three-Factor Regressions for Portfolios Formed from Independent Sorts on Size and BE/ME(July 1929 – June 1997) www.pptmart.com

Interpretation of the results • The findings: • Small firms have higher average returns than large firm. • Firms with high ratios of book value to market value of common equity have higher average returns than firms with low book-to-market ratios. • Since the CAPM does not explain this pattern in average returns, it is typically called anomaly.

How should we interpret these results? • One argument is that size and relative value (as measured by the B/M ratio) proxy for risk is not captured by the CAPM beta alone. • Another explanation attributes these premium to irrational investors preferences for large size or low B/M firms (growth firms). This evidence may be more relevant for the B/M or “value” factor in light of the evidence that size premium has largely vanished in recent years.

The irrational investor preference for value premium explanation says it is due to investor overreaction to firm performance. High BE/ME stocks tend to be firms that are weak on fundamentals like earnings and sales, while low BE/ME stocks tend to have strong fundamentals. Investors overreact to performance and assign irrationally low values to weak firms and irrationally high values to strong firms. When the overreaction is corrected, weak firms have high stock returns and strong firms have low returns.

Indian experiences • Connor and Sehgal (May 2001) test for multi-factor Fama and French model in India using a sample of 364 companies and monthly returns data (from June 1989 to March 1999), the authors find evidence of Fama and French model in India. • Mohanty, P.(April 2001) test the model and finds the significant market risk premium and size effect but insignificant value premium. • What is your conclusion?

Fama and French (2004) • Comments • Fama and French (1992) confirm the evidence that the relation between average return and beta for common stocks is even flatter after the sample periods used in the early empirical works on the CAPM. • If betas do not suffice to explain expected returns, the market portfolio is not efficient, and the CAPM is dead in its tracks.

Some researchers try to criticize the above comments as follows: • One possibility is that the CAPM’s problems are spurious, the result of data dredging – publication-hungry researchers scouring the data and unearthing contradictions that occur in specific samples as a results of chance.

Fama and French (2004) have responded as follows: • Chan, Hamao and Lakonishok (1991) find a strong relation between book-to-market equity (B/M) and average return for Japanese stocks. • Capaul, Rowley and Sharpe (1993) observe a similar B/M effect in four European stock markets and in Japan. • Fama and French (1998) find that the price ratios that produce problems for the CAPM in U.S. data show up in the same way in the stock returns of twelve non-U.S. major markets, and they are present in emerging market returns. • The above evidence suggests that the contradictions of the CAPM associated with price ratios are not sample specific.

Do visit • www.pptmart.com