Download

1 / 41

410 likes | 568 Views

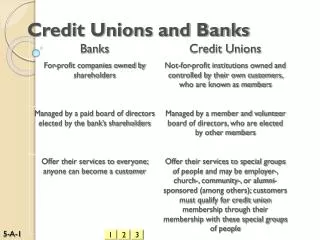

Preparing for Rising Interest Rates Webcast Sponsored by the Division of Credit Unions and the Washington Credit Union League. Facilitated by James L. This, PhD The Paragon Consulting Group, LLC. What’s the Big Deal?. Don’t rising interest rates mean that credit unions will thrive?.

E N D

Preparing for Rising Interest RatesWebcast Sponsored by the Division of Credit Unions and the Washington Credit Union League Facilitated by James L. This, PhD The Paragon Consulting Group, LLC

What’s the Big Deal? • Don’t rising interest rates mean that credit unions will thrive?

Echoes of the PastReflections on the S & L Debacle “S&L’s found themselves stuck with asset portfolios principally invested in long-term mortgages whose returns were substantially less than the prevailing market interest rates thrifts had to pay to maintain depositors. Many weak thrifts were unable to manage such interest rate exposure.” Source: The S&L Crisis – Putting Things in Perspective, Walter M. Primoff, December 1989 The CPA Journal Online

S&L Trends 1980-1984 Source: The Savings and Loan Crisis and Its Relationship to Banking, FDIC.GOV

Categories of Risk • Liquidity • Loan funding demands and deposit withdrawals exceed the availability of liquid assets • Interest rate • Changes in the market interest rates reduce net income

Areas of ConcernInterest Rates Can Rise Quickly Fed Funds Rates

Areas of ConcernCU Margins Are Already Low Source: CUNA Research and NCUA

Areas of ConcernCU’s Have Been Relying on Low Savings Rates to Bolster Spread

Areas of ConcernCU’s Have Added Long-Term Assets to Their Loan Portfolios Especially Mortgages

30 20 10 0 Areas of ConcernSome CU’s Are Already Having Earnings Problems Percent Small Credit Unions with Negative Earnings Source: CUNA Economics & Statistics

Concerns Voiced by DCUSource: DCU Bulletin B-04-06 • Held-to-maturity and available-for-sale securities account for half the investment portfolio. • Longer term investments (terms over one year) increased more than 28% during a falling interest rate environment • Liquidity decreased by almost 6%

Concerns About LiquidityCredit UnionDeposit Portfolios Have a Lot of Rate Sensitive Deposits

When you change share, checking or MMA rates When you change loan rates So What Are the Dangers?Cost of Deposits Rise Faster Than Loan Income

Simplified ExampleCost of Deposits Rise Faster Than Loan Income • CU has $50,000,000 in assets (loans) balanced with $50,000,000 in liabilities (regular shares) • They increase the rate by 1% on each

Look at What HappensCost of Deposits Rise Faster Than Loan Income

So What Are the Dangers?Others Increase Deposit Rates and You Do Not—Funds May Leave • Possible Scenarios • You have to sell investments (at a loss) to handle cash flows • You have to borrow to cover liquidity needs • You have to restrict lending due to liquidity problems

And Just for Fun • What if the equity markets become attractive again?

Planning Questions for Leadership • How much of our deposits are at risk? • How much are we willing to lose? • What are we able to pay to stem the flow? • How will we off-set the higher cost of deposits?

So What Do We Do About It? • Create strong ALM policies and an ALCO Committee • Assess the risk • Make decisions and take action using the research • Track results • Make adjustments

Basic Principles of Asset-Liability Management (ALM) • Diversify the mix of assets and liabilities to minimize fluctuations in interest rates • Price assets and liabilities to ensure positive net income • Balance assets and liabilities in terms of maturities and returns

Roles in ALM Management • DCU and NCUA • Regulate • Examine • But not validate

Asset-Liability CommitteeSource: DCU Bulletin B-04-06 • ALCO Committee in Place • Does your credit union have a Board-appointed ALCO? • Qualified People On the Committee • By position, who sits on the committee and what background do they have in managing IRR? Strong Policies

Asset-Liability CommitteeSource: DCU Bulletin B-04-06 • Regular Testing and Reporting • How often does your ALCO meet and report its decisions and discussions to the Board? • Integrity of ALM Models • Please explain how the ALCO’s work is periodically audited or the IRR model output verified. Strong Policies

Guidelines for MeasurementSource: DCU Bulletin B-04-06 • What methods or model does your credit union use to measure IRR?. • What IRR measurements does your credit union use? • What are your Board approved policy IRR limits? • Who is the primary operator of your IRR system or model? Assess the Risk

Guidelines for MeasurementSource: DCU Bulletin B-04-06 • Describe the training the operators have been provided on your system or model? • What were the results of your most recent model or IRR evaluation? • Is your model used for testing various product (loans and shares) pricing options before implementing the option? Assess the Risk

ALM Procedures for Interest Rate Risk • DCU Bulletin No. B-04-10 • August 30, 2004 • Topic for discussion after webcast Assess the Risk

Common ALM Models • Impact of interest rates on net income • Gap Analysis • Net Income Simulation • Impact of interest rates on net worth • Net Economic Value (NEV) Assess the Risk

Results of ALM Tests Effect on Net Worth Net Income At Risk Assess the Risk Source: CUNA VAP Module V415

A Sampling of Models • Model Management • CUNA Mutual • CUPRO • CUNA Mutual • IPS Sendero • Profitstar • Banc Ware • CU/ALM-ware • Brick and Associates • Mark Smith • C. Myers • Palm Software • NW Corporate CU Assess the Risk

A Model is Only Good If It Is Used in Making Decisions • Use ALM process when making decisions • Pricing • Terms • Marketing • Products and services

Set Guidelines on TolerancesExample Only Scenario: A rate increase or decrease of 300 basis points applied to the current quarter end financial statements. Strong Policies

Possible Actions When Trigger is PulledExample Only • Adjust dividends on shares • Adjust interest rates on loans • Adjust maturities of share and loan products • Sell investments and re-invest • Put variable rates on more products • Adjust indexes for variable rate share and loan products Strong Policies

Possible Actions When Trigger is PulledExample Only • Adjust re-pricing intervals for variable rate share and loan products • Adjust periodic or lifetime rate caps or floors for variable rate share and loan products • Impose early withdrawal options or penalties for share certificate products • Charge fees, including but not limited to minimum balance fees Strong Policies

Things to Avoid Crumbling to conversational pressure Take Action

Things to Avoid Pricing only to the marketplace Take Action

Things to Avoid Waiting too long to change Take Action

Things to Avoid Waiting for the return of the good old days Take Action

Things to Avoid Offering a rate that is too good

Where to Get Help • CU facilitators here tonight • DCU staff here tonight • WCUL • Paragon Group • Jim This

Follow-upDCU Website • FAQ’s from discussions • Video copies of studio workshop • Copy of PowerPoint presentation on the web site • Link to Paragon Planner®

And Now….For Something Completely Different It’s all yours, facilitators!!