Download

1 / 15

150 likes | 297 Views

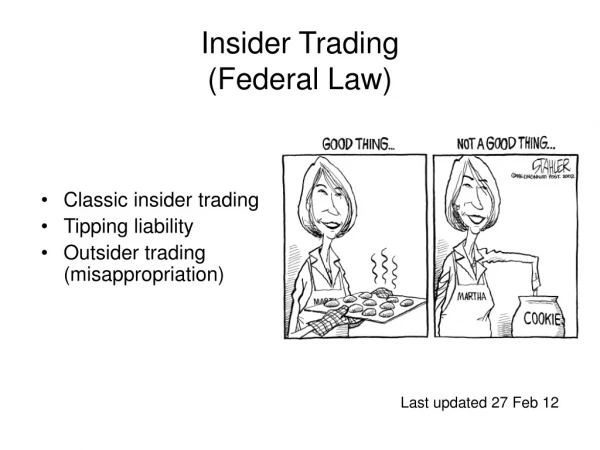

Product Market Competition, Insider Trading Regulation, and Optimal Managerial Contracts. Chyi-Mei Chen Chien-Shan Han. Background. Optimal managerial Compensation Scheme. Risk averse. Information advantage. Risk neutral. Entrepreneur. Manager/ insider. profit. New entrant.

E N D

Product Market Competition, Insider Trading Regulation, and Optimal Managerial Contracts Chyi-Mei Chen Chien-Shan Han

Background Optimal managerial Compensation Scheme Risk averse Information advantage Risk neutral Entrepreneur Manager/ insider profit New entrant Stock Market Product Market Insider trading Shareholder Rival Firm Regulation? incumbent

Model 1 • I (incumbent firm) and E (entrant) produce a homogeneous good and engage in a quantity competition. • The unit cost for firm E is random, a low unit cost 1-a high unit cost • The unit cost for firm I is fixed at • Demand Curve Risk-averse manager • Linear compensation scheme

Model 1 Stock market open, market makers post bid and ask prices. M can submit orders. Liquidity trader prob b buy l share prob s sell l share prob 1-b-s no trade Firms and managers learn about whether there are insider trading restrictions Given (qI,A,B), M choose qE Firm I choose qI Firm E offer a scheme (A,B) M observe the realized cost of firm E Stock market close, profit realized

Results If the firm’s profit is negative correlated with the trading gain, Optimal Scheme is B>0 Optimal Scheme is B=0 Risk averse Information advantage Risk neutral Higher firm value Entrepreneur Manager/ insider Expand output Larger profit profit New entrant No insider trading Insidertrading Stock Market Product Market shrink output Fewer profit Lower firm value Shareholder Rival Firm incumbent

Results • When the manager is not too risk averse, insider trading can be value-enhancing even if the shareholders of the entrant firm must bear all the trading loss caused by insider trading. • In the absence of insider trading regulation a following firm that suffer from the adverse selection problem resulting from cost uncertainty may have a higher market value. • Allowing insider trading tends to raise the power of the managerial compensation scheme (B>0).

Model 1—Hedging Policy Heging is costly Given (qI,A,B), M choose qE M choose by promising to pay the insurer in low cost state, and get a re-imbursement in high cost state. Firms E offer a scheme (A,B) M observe the realized cost

Results • When insider trading is allowed, if B>0 then after making its output decision , firm E hedges more in the bear market (a<0.5)than in the bull market. (a>0.5)

Intuition Bear market a<0.5 1-a>0.5 Bad state Good state Less information advantage more information advantage Higher trading profit Lower trading profit Higher salary Lower salary Positive Correlated salary Trading gain Hedging more

Intuition Bull market a>0.5 1-a<0.5 more information advantage Less information advantage lower trading gain Higher trading gain Higher salary Lower salary Negative Correlated salary Trading gain Hedging less

Model 2 • Consider both firms facing with cost uncertainty and their shares are traded in the stock market after their managers simultaneously make output decisions and privately receive cost information. • One firm indulging insider trading creates a negative externality on its rival firms, leading to a big reduction in the value of the rival firm. • Allowing insider trading is always the firm’s best strategy.

A1 B A2 firm 1 stock Index basket Firm 2 stock Insider trading Insider trading D Firm 2 Firm 1 Compensation Scheme Compensation Scheme Output market Entrepreneur Entrepreneur consumer

Prisoner’s Dilemma Allowing insider trading may results in a prisoner’s dilemma, the shareholders of both firm would be made worse off.

Implications • This provides a rationale for insider trading regulation. • The value of index Trading • Reasons: Insiders possessing security-specific private information loses much of their information advantage if they are forced to trade the basket, which implies insider’s incentive to over-expand output is mitigated, the firm value is enhanced

Thank you for listening The End