Download

1 / 6

60 likes | 207 Views

Now, using Sample Company information, record the following additional issues of common and preferred stock: Issued 100 shares of PS at $102 per share: Cash (100x $102) 10,200 PS (100x $100 par) 10,000 APIC - PS (plug) 200 Issued 500 shares of CS at $5 per share:

E N D

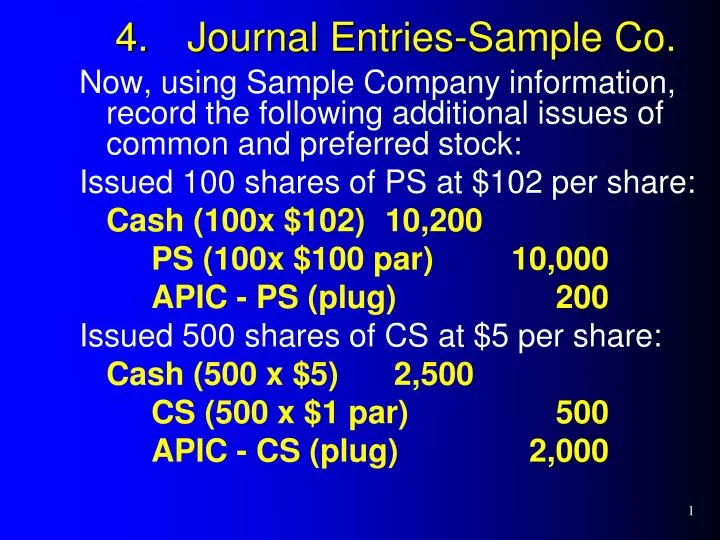

Now, using Sample Company information, record the following additional issues of common and preferred stock: Issued 100 shares of PS at $102 per share: Cash (100x $102) 10,200 PS (100x $100 par) 10,000 APIC - PS (plug) 200 Issued 500 shares of CS at $5 per share: Cash (500 x $5) 2,500 CS (500 x $1 par) 500 APIC - CS (plug) 2,000 4. Journal Entries-Sample Co.

TT Corporation has 100,000 shares of $1 par value stock authorized, issued and outstanding at January 1, 2008. The stock had been issued at an average market price of $5 per share, and there have been no treasury stock transactions to this point. Assume that, in February of 2008, TT Corp. repurchases 10,000 shares of its own stock at $7 per share. In July of 2008, TT Corp. reissues 2,000 shares of the treasury stock for $8 per share. In December of 2008, TT Corp. reissues the remaining 8,000 shares for $6 per share. Prepare the journal entries for 2008 regarding the treasury stock. 5. TS - Example Problem

Feb: repurchase 10,000 sh. @ $7 = $70,000. July: reissue 2,000 sh @ $ 8 = $16,000 (cost = 2,000 @ $7 = 14,000) 5. TS Example -Journal Entries TS 70,000 Cash 70,000 Cash 16,000 TS 14,000 APIC - TS 2,000

Dec: reissue 8,000 sh. @ $ 6 = $48,000 (cost = 8,000 sh.@ $7 = 56,000) Now we need to debit one or more accounts to compensate for the difference. (1) debit APIC-TS (but lower limit is to -0-). (2) debit RE if necessary for any remaining balance (this is only necessary when we are decreasing equity). 5. TS Example -Journal Entries Cash 48,000 APIC-TS (1) 2,000 RE (2) 6,000 TS 56,000

Pref. Div? 8% of par of 200,000 = $16,000 per year 1. Noncumulative- No pref. div. in 2006 and 2007 - not owed. Declare $100,000 div. in 2008; first $16,000 to pref., balance to common 2. Journal entries 7/1 RE (Pref. Div.) 16,000 RE (Common Div.) 84,000 Dividends Payable 100,000 8/1 Dividends Payable 100,000 Cash 100,000 Exercise 11-8

Pref. Div? 8% of par of 200,000 = $16,000 per year 3. Cumulative- No pref. div. in 2006 and 2007 - but must catch up before div. to common Declare $100,000 div. in 2008 - First $16,000 x 2 = $32,000 to preferred, for prior years. - Next $16,000 to preferred for 2008 - Balance of $52,000 to common Exercise 11-8