Download

1 / 18

180 likes | 311 Views

PPA 723: Managerial Economics. Lecture 13: Competition in the Long Run. Managerial Economics, Lecture 13: Competition in Long Run. Outline Profit Maximization in the Long Run The Long-Run Supply Curve Characteristics of Long-Run Equilibrium in a Competitive Market.

E N D

PPA 723: Managerial Economics Lecture 13: Competition in the Long Run

Managerial Economics, Lecture 13: Competition in Long Run Outline • Profit Maximization in the Long Run • The Long-Run Supply Curve • Characteristics of Long-Run Equilibrium in a Competitive Market

Managerial Economics, Lecture 13: Competition in Long Run LR Competitive Profit Maximization • In competitive markets, firms are still price takers in the long run. • So the long-run output decision is to set output at the q* where • p = LRMC(q*)

Managerial Economics, Lecture 13: Competition in Long Run Long-Run Shut-Down Decision • In the long run, a firm operates only if revenue variable cost. • All costs are variable in the long run, so the shut-down rule in the long run is to • operate only if revenue cost • i.e., if p minimum of AC curve.

Managerial Economics, Lecture 13: Competition in Long Run Short Run vs. Long Run • In the short run, a firm compares its revenue only to its avoidable (variable) cost, It ignores sunk fixed costs. • In the long run, all costs are avoidable. • A firm can eliminate them by shutting down. • So a firm shuts down if LR profit is negative: i.e., if < 0

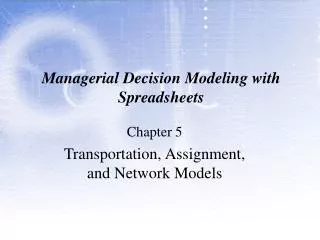

Managerial Economics, Lecture 13: Competition in Long Run Long-Run Firm Supply Curve • Because all costs are variable in the long run, the long-run firm supply curve equals the long-run MC curve above the minimum of the long-run AC curve. • A firm chooses its capital in the long-run, so the long-run supply curve may differ from the short-run supply curve.

Managerial Economics, Lecture 13: Competition in Long Run Figure 8.11 The Short-Run and Long-Run Supply Curves p , $ per unit SR S LR S LRAC SRAC SRAVC p 35 B A 28 25 24 20 LRMC SRMC 0 50 110 q , Units per year

Managerial Economics, Lecture 13: Competition in Long Run LR Market Supply Curve • The market supply curve = the horizontal sum of firms' supply curves in both the long-run and the short-run. • The market supply curve differs in the long-run and the short-run because of differences in number of firms and, perhaps, in input prices.

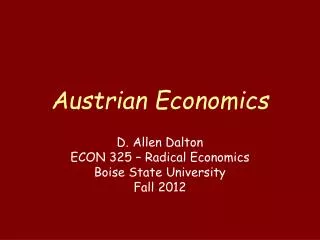

Managerial Economics, Lecture 13: Competition in Long Run Number of Firms • In the short run, each firm can produce more or less, but the number of firms, n, is fixed. • In the long run, firms can produce more or less and firms can enter or exit the market. • Firms enter a market in response to profits and exit in response to losses.

Managerial Economics, Lecture 13: Competition in Long Run (a) Firm (b) Market p, $ per unit p p, $ per unit Long-run market supply before entry 1 S S1 Profit S2 Entry LRAC p1 p1 10 10 LRMC D 0 150 0 Q , Hundred metric tons of oil per year q , Hundred metric tons of oil per year

Managerial Economics, Lecture 13: Competition in Long Run Long-Run Market Supply • The long-run market supply curve is flat at the minimum long-run average cost if • There is free entry and exit. • An unlimited number of firms have identical costs. • Input prices are constant as the number of firms changes.

Managerial Economics, Lecture 13: Competition in Long Run (a) Firm (b) Market p, $ per unit p p, $ per unit 1 S LRAC Long-run market supply curve with entry 10 10 LRMC 0 150 0 Q , Hundred metric tons of oil per year q , Hundred metric tons of oil per year

Managerial Economics, Lecture 13: Competition in Long Run Why Long-Run Market Supply Curve Sometimes Slopes • Factors that lead to a long-run supply curve that is not flat include • Barriers to entry • Variation in costs across firms • Input prices that vary with market output.

Managerial Economics, Lecture 13: Competition in Long Run Figure 8.13 Long-Run Market Supply in an Increasing- Input-Cost Market (b) Market (a) Firm p , $ per unit p , $ per unit 2 MC 1 MC 2 AC S 1 AC e E 2 2 p 2 e E 1 1 p 1 q q q , Units per year Q = n q Q = n q Q , Units per year 1 2 1 1 1 2 2 2

Managerial Economics, Lecture 13: Competition in Long Run Figure 8.14 Long-Run Market Supply in an Decreasing- Input-Cost Market (b) Market (a) Firm p , $ per unit p , $ per unit 1 MC 2 MC 1 AC 2 AC e E 1 1 p 1 e E 2 2 p 2 S q q q , Units per year Q = n q Q = n q Q , Units per year 1 2 1 1 1 2 2 2

Managerial Economics, Lecture 13: Competition in Long Run Long-Run Competitive Equilibrium • The intersection of the long-run market supply and demand curves determines long-run competitive equilibrium • With identical firms, constant input prices, and free entry and exit, • The long-run market supply curve is horizontal at minimum long-run AC • The equilibrium price = minimum long-run AC • A shift in the demand curve affects only equilibrium quantity and not equilibrium price.

Managerial Economics, Lecture 13: Competition in Long Run Figure 8.15 The Short-Run and Long-Run Equilibria for Vegetable Oil (a) Firm (b) Market p , $ per ton p , $ per ton 1 2 D D MC AC SR S F f AVC 2 2 11 11 E LR S 2 10 10 e E F f 1 1 1 7 7 0 100 150 165 0 1,500 2,000 3,300 3,600 q , Hundred metric tons Q , Hundred metric tons of oil per year of oil per year

Managerial Economics, Lecture 13: Competition in Long Run Characteristics of Long-Run Competitive Equilibrium • All firms earn zero economic profit (which means they earn the same business profit they could earn elsewhere). • All firms in market operate at minimum long-run AC; i.e, they produce the equilibrium quantity using the minimum possible resources.