Download

1 / 14

160 likes | 404 Views

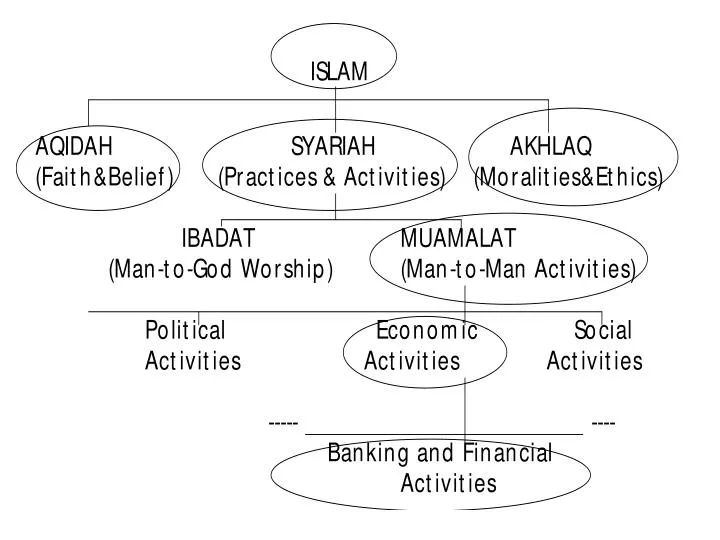

Therefore…. Banking and financial activities being part and parcel of Islamic Muamalat, these are therefore subject to the Syariah laws on Muamalat. Prohibition of Interest. 1. Al Quran “Allah has permitted trade and forbidden usury” Al Baqarah:275. Definisi faedah, usury dan riba.

E N D

Therefore… • Banking and financial activities being part and parcel of Islamic Muamalat, these are therefore subject to the Syariah laws on Muamalat.

Prohibition of Interest • 1. Al Quran • “Allah has permitted trade and forbidden usury” Al Baqarah:275

Definisi faedah, usury dan riba • Riba is an Arab word which means ‘menambah’(al-ziyada), ‘mengembang’(al-numuw) , ‘meningkat dan membesar’(al-irtifa dan al-uluw). • The core meaning of riba is ‘bertambah’, therefore, riba in relation to money is any value added onto the money(principal) . • Before Islam , Arabs perceived riba as an increment in the form of money resulting from delayed payment of debt. • From the Islamic perspective, any interest(faedah) charged on all kinds of bank loans is considered riba, whether the loan is for personal use or productive use . • Prohibited by Quran(the main source of reference for Muslims) as elaborated in verse ar-Ruum 30-39; an-Nisaa 161, al-Imran 130-132 and al-Baqarah 275-281.

Qur’anic Verses dealing with Riba • “And whatever riba you give so that it may increase in the wealth of the people, it does not increase with Allah”. (Ar-Rum 30:39) • “Those who take interest will not stand but as stands whom the demon has driven crazy by his touch. That is because they have said: ‘Trading is but like riba’. And Allah has permitted trading and prohibited riba. • So, whoever receives and advice from his Lord and stops, he allowed what has passed, and his matter is up to Allah. And the ones who revert back, those are the people of fire. They remain forever……. • (Al-Baqarah 2:275-281)

Compliance with the scheme of shariah laws • Islam imposes its ‘ahkam’(laws,norms) on its believers. • These laws or value are not man-made; instead they are derived from the sources of Syariah. • There are two primary sources: • a). Al-Quran • b). Al-Hadith(Sunnah) -the traditions of prophet Muhammad-peace be upon him c).Al Ijma’ ( consensus of opinion among jurists of Islamic law) • d)Al Qiyas ( analogical deduction)

These laws as derived from the above sources are arranged into the following scheme of 5 levels: 1. Fard or Wajib • An obligatory duty, the omission is punishable 2. Mandub or Mustahab • An action which is rewarded, but the omission is not punishable. 3. Jaiz or Mubah • An action which is permitted, and the law is indifferent 4. Makruh • An action which is disliked yet not punishable, but the omission is rewarded. 5. Haram • An action which absolutely forbidden and punishable.

Islamic Economic and Finance Pre-requisites: • Products must be approved by Islamic Syariah. • Give benefits not harm • Does not involve riba • Do not make too much profit till harm customers. But Islam does not limit.

Problem and Limitation: • Confident crisis • Lack of promotion • Government support • Lack of knowledge

Bank Islam – Customers Relationship • Mudharaba and Musyaraka: • Profit sharing between partners and between investor and entrepreneur • Mudaraba – savings¤t deposit, general and specific investment deposit, Islamic Negotiable Instrument of deposit,share financing, unit trust financing, project financing, Cagamas • Musyaraka – share financing, unit trust financing, bridging finance, syndicated financing, bonds, letters of credit

Bank Islam – Customers Relationship • Al-Ujr: • Fee, charges, commission between bank and its customers • Stockbroking services, funds transfer, travellers’ cheques, standing instruction, atm service, foreign exchange, forward rate agreements • BBA – Negotiable Islamic Deposit Certificate, share & unit trust financing, project financing, bonds, syndicated financing, revolving financing, bridging finance, house & commercial property financing • Murabaha – overdraft, working capital financing, revolving financing, commercial papers, sell & buy-back agreements, letters of credit, Islamic accepted bills, export credit financing

Bank Islam – Customers Relationship • Qardhul Hasan – charge card, bonds, government investment issues • Ijarah – syndicated financing, bonds, leasing • Al-Ijara wa Iqtina – house financing, Cagamas • Al-Ijara Thumma Al-Bai (AITAB) – hire purchase, industrial hire purchase • Bai’ Al-Dayn – factoring, Islamic accepted bills, export credit financing • Istisna’ – bridging financing, bonds, project financing, syndicated financing • 11. Wakalah & Kafalah – trade financing