Download

1 / 22

240 likes | 257 Views

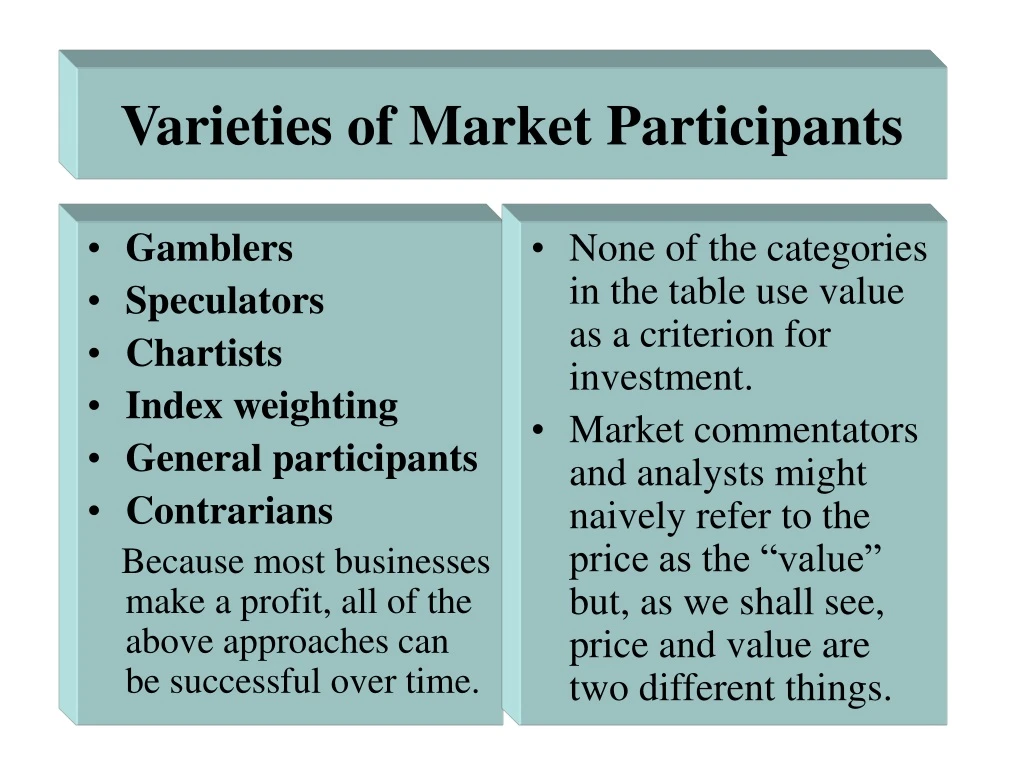

Gamblers Speculators Chartists Index weighting General participants Contrarians Because most businesses make a profit, all of the above approaches can be successful over time. None of the categories in the table use value as a criterion for investment.

E N D

Gamblers Speculators Chartists Index weighting General participants Contrarians Because most businesses make a profit, all of the above approaches can be successful over time. None of the categories in the table use value as a criterion for investment. Market commentators and analysts might naively refer to the price as the “value” but, as we shall see, price and value are two different things. Varieties of Market Participants

Value Investing • The business performance creates the value. The price creates the opportunity. • Warren Buffett puts it another way: “Price is what you pay; value is what you get.” • By determining the value of a share of the business, ‘Value Investors’ know when the price is at a discount or premium to the value and are able to benefit from price movements caused by fear, greed, stupidity and irrational market sentiment.

Assuming that the net profit of a business that distributes all of its profit is $100,000 and our RR (Required Rate of Return) for that business is 20%, our valuation might be: Profit/RR = Value = $100,000/20%=$500,000 We are able to acquire a half interest for $200,000. The price we pay does not change the value. Providing the value does not change, what is a good outcome? Either: A: Our partner offers to buy our share for $250,000, or B: Our partner offers to sell us his share for $150,000. Buying into a small business

We value a share of a business at $2.50 and buy the stock for $2. Buying a share of a business at a bargain price does not reduce its value. Buying a share of a business at a premium to its value, does not increase its value. Providing the the business performance does not change and the value remains stable, what is a the better outcome? A: The price increases to $2.50; or B: The price declines to $1.50? Buying a small share of a large business

A life lived in fear is a life not worth living • Value investors have no concern for the irrational market sentiment that drives stock prices. • Their only concern is the performance of the business in which they are part owners. • If you have no idea of the value of your stocks and they decline in price, you have good reason to be concerned. • If you have no idea of the value of a business, why would you risk buying into it?

Measuring the Business Performance Declared profit only tells part of the story - hence the truism: “A business can go broke declaring a profit.” • StockVal uses BE (Beneficial Earnings) to determine shareholder benefits. BE = Amortization of goodwill + Grossed up dividends + Retained profits + Changes in reserves. • BE is adjusted for allowable abnormals from both the Profit & Loss account and changes in reserves to calculate BROE: Beneficial Return On Equity. = BE/Equity

Basis of Valuation • While BROE is determined for each year of the review period, the IRR measures the BROE over the full review period of 5 years. • When the BROE or IRR is less than RR, the value will only equal the nominal value if all profits are distributed as dividends, where: • Nominal value = E*(BROE or IRR)/RR • E.g.: Equity= $1; (BROE or IRR)= 10%; RR = 15% • I.e. Nominal value = $1 * 10% / 15% = 67 cents. • When the BROE or IRR is less than the RR, the nominal value will decline in proportion to the lower dividend payout.

When a business has the ability to reinvest profits at a rate which exceeds the RR, the Value will exceed the Nominal Value. • If a perpetual bond paid $20 p.a. in interest and our RR happened to be 10%, its value would be: $20/10% = $200. (I.e. $100*20%/10%) • If the bond accrued 20% interest on an issue price of $100 and only paid interest once every 10 or 20 years, its value would be greater than $200 because it is reinvesting our accumulated interest at a rate that is double our RR of 10%.

POSITIVES. The ability of the business to reinvest profits at a continuing high ROE. Directors who are prepared to eat their own cooking. Integrity of management. The owners are entitled to hear both the good and bad news, and the course of action for remediation, not excuses or justification. NEGATIVES. Empire building. Misleading or false profit declarations. Misleading use of abnormals, and lack of recognition of asset values. Payment of unfranked dividends at a time when the business is seeking additional capital. Owner Wealth Creationand Destruction

Number 1 Attribute ofOwner Wealth Creation • The ability of the business to reinvest profits at a continuing high ROE. • Buffett’s Berkshire Hathaway has never paid a dividend. The ability of the business to reinvest profits at a high ROE has enabled the share price to climb to about $60,000 today. • Had the business distributed all profits and gains as dividends, shareholders would have received about $1.20 each year in dividends, and the stock would be worth about $10 to $15 today.

Dividends • Receiving dividends from a business that has the capacity to reinvest profits at 20% is like transferring your money from a savings account earning 20% to one that pays a much lower rate of interest. • If cash flow is important, it is best achieved by selling a few shares at their enhanced value, or investing in trusts that distribute all income.

Owner Wealth Destruction Empire Building. • Usually the worst news that shareholders can hear is that their employees (directors) have a war chest and are on the acquisition trail with your money. • Takeovers normally require a price to be paid that far exceeds the value. Hence, in the absence of significant synergy, the ROE will decline. In such event the value per share will also decline. • The winners are nearly always the sellers of the target company.

Equity $100m;$1share BE $20m. BROE 20% If Divs. 2/3rds, i.e. 15c Value @ 15% RR = $1.33 ($1*20%/15%) The company buys another business for $100m with BE of $10m. => BROE 10% Company now has equity of $200m, with BE of $30m. Hence the BROE has declined to 15% Value @ 15% RR = $1 ($1*15%/15%) In order for the owners to be as well off as previously, BE must increase by $10m. Example of negative Empire Building

Misleading or False Profit Declarations Example: AGL Interim Report. Quote in large type face: “The profit attributable to Proprietors for the half year ended 31 December 1999 was $181.7 million, up 55.8% from $116.6 million for the December 1998 half year.” ------------------------------------ No P&L or Balance Sheet, but the true position was as follows: Declared profit $181.7m Future tax benefits (Ralph) $40.7m Negative change in reserves $34.4m Beneficial Earnings $106.6m(ex imp. credits) DOWN 8.6% ON THE DECEMBER 1998 HALF YEAR!

Misleading use of Abnormals • Mining companies, in particular, will capitalize tax deductible operating costs to the Balance Sheet as an asset, thereby enhancing declared profits. • This is fine if such costs are a true asset, but what inevitably occurs is that they are subsequently written off as an abnormal loss or negative revaluation in the 5 yearly “spring clean”. • This means that profit declarations in previous years were clearly and deceptively overstated. • A note in the accounts to such effect should be mandatory.

Rationalization and Restructuring costs • In order to increase the pre-abnormal profit, companies often maximize negative abnormals. • Often so-called abnormals are part of the normal risk, or operating costs, of the business and are often due to inadequate provisioning in prior years, or managerial negligence or incompetence. • Companies which “declare” that they are poorly structured or mismanaged by allocating abnormal expenses for restructuring and rationalization on a regular basis are best avoided.

Lack of recognition of true asset values • A substantial write-off or revaluation in a single year is normally due to a lack of recognition by your employees (directors) of true (lower) asset values in previous years. • When this occurs, you must decide if your employees are guilty of either negligence or misrepresentation, and decide if you feel comfortable leaving your savings under the custodianship of such fools or rogues.

Payment of unfranked dividends at a time when the business needs new capital • The implication of a business transferring its tax liabilities to the owners by paying unfranked dividends, is that it is unable to gainfully employ the funds. • When a business does this in the same year that it passes the hat around for additional capital, you know that the business is run by fools who think they need to encumber the owners with tax liabilities in order to support the share price.

Integrity of Management • Your employees (directors) should not be the ones to decide if the owners have the right to consider a takeover offer. • Imagine if you owned a small business and, in your absence, an attractive offer to buy the business was made to your manager, who decided not to inform you for fear of losing his or her job under new ownership. • What would your reaction be?

Recent Examples of Such Arrogance • NAB offer to Chairman of AMP of $21 a share. In StockVal’s opinion, at least three times the value of the stock. • Undisclosed offers to Directors of HIH Insurance: • Suncorp-Metway’s offer of $1.70 in mid April. • Liberty Mutual’s offer of $2.40 two years ago. - Both offers where subject to due diligence.Were the Directors concerned that, by opening up the books to due diligence, the owners would discover the truth? Or were they just protecting their jobs?

All Shareholders Should Have Equal Rights • Because shareholders of Holyman were not initially advised of the approach by Lang Corp. and Adsteam, many sold at less than 50% of the takeover price. • Those with insider knowledge benefited from information not available to all shareholders. • Directors should be required to advise the ASX within 24 hours of any formal approach, and the stock suspended from trading until all shareholders have been notified in writing.

Corporate Governance Remedies • Directors of listed companies must be made more accountable for their actions. • Your President, Ray Bricknell, intends that the AIA will become increasingly proactive in seeking legislative changes that will better protect shareholders’ interests. • It is important that we lend Ray our full support. • For particulars of a proposal regarding the appointment of an independent “Corporate Governance Director” visit www.stockval.com.au