Download

1 / 22

220 likes | 379 Views

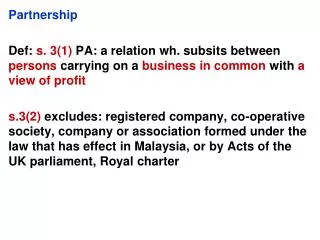

1 Partnership. Tutor: Marie O’Callaghan . Partnerships. Professionals such as doctors , lawyers ,dentists, vets, accountants are not allowed to form companies.

E N D

1 Partnership Tutor: Marie O’Callaghan

Partnerships • Professionals such as doctors, lawyers ,dentists, vets, accountants are not allowed to form companies. • There are advantages to partnerships over forming a company from the point of view of tax, accounting and disclosure requirements. • Partnerships do not go through a registration process to form. • Partnership is not a separate legal identity = partners have unlimited liability, unlike directors or shareholders in companies. • The downside is that each partner is liable for the losses of his co-partner in carrying on the partnership business, even where the other partner has defrauded clients of the business.

Partnership Act 1890 - Amended 1907 • Partnership Act 1890 defines a partnership and essentially states that where 2 or more people carry on business with a common view of profit, then a partnership exists. • A written partnership agreement is not necessary. • The act applies where no partnership agreement is in place.

The Main Provisions • P&L must be shared equally • No interest paid on capital • No remuneration • Differences settled by majority • Change of business requires consent of all • No right to expella partner • No right to retire • All Partners have the right: • Take part • Prevent entry of another partner • Examine the books • Receive interest 5%PA on loans/advances ex capital • Dissolve the partnership • does not prevent a former partner from competing after leaving • Partnership dissolves automatically on • death of partner • bankruptcy of partner • Illegal activity of partnership

Written Agreement Written partnership agreement is crucial to set out: • Function of the partnership • Capital each partner will invest • The profit sharing ratio • The role of each partner • Drawings – remuneration • Expulsion • New partners • non compete agreement • Dissolution • etc. Written Partnership agreement overrides the terms of the act

Partnership Accounting

Capital A/C • Records the original monies invested • Usually remains fixed unless • More capital introduced • Non-current assets re-valued • Goodwill crystallised and recognised • Credit balance • Credit the giving: partners giving capital to the business

1 ABC Opening credit balances2 B introduces additional capital3 C withdraws capital4 ABC Capital upward adjustment for recognition of goodwill and positive re-valuation of assets

Current A/C • Short term element of each partners capital • Record for each partner • Share of profit/loss • Drawings • Interest on loans given to partnership • Interest on credit capital • Corresponding entry in appropriation

Partner A Debit Credit Interest on Credit balance – interest on investment held in the current account Interest on Capital – interest earned on original investment Loan Interest – interest due (not yet paid) for a loan given to the partnership Share Profits – divide of profit • Drawings – withdraw from cash instead of salary • Interest on drawings – charge for overdraw

Partner B Debit Credit Salary – reward for taking extra responsibility or work • Interest on Debit balance – money take out of the partnership/loan from business – interest charged

Partner C Debit Credit Capital – partner introduced more capital to the business.

Appropriation A/C • In a partnership, the profits earned are due to the various partners in their profit sharing ration and are apportioned to them in the appropriation section on the Statement of Comprehensive Income • 3 Sections • Distributable income (Profit for year) • Balance of Net Profit • Share of Profit (as per PSR)

Statement of Financial Position • Equity Section • List of the closing balances from the partners capital and current accounts.