Download

1 / 16

180 likes | 222 Views

Learn about profit, functions, nature, and structure of Profit and Loss Accounts. Know how to calculate Gross Profit, Net Profit, and their significance in assessing business performance.

E N D

Profit and Loss Account Understanding the structure of the Profit and Loss Account

Nature of Profit Profit has a number of functions: • Motivates people to set up in business, without profit there would be little incentive for individuals to commit their time and personal resources. Economists often refer to Normal Profit. This is the minimum reward an entrepreneur must receive to maintain an interest in the business. • Profit also helps resource allocation in market economies. Businesses that make profit are able to purchase more raw materials and labour in order to expand production. • Investors are attracted to those businesses that are likely to give the greater financial reward. Economists refer to this as Abnormal Profit – the amount by which total profit is greater than normal profit.

The amount of profit that a business makes is a measure of how well it is performing. However there are other factors which affect the performance of a business such as the competition a business faces. • From an accountant’s point of view, profit is the amount of money left over in a particular trading period when all business expenses have been met. Profit can then be - • Retained • Used to pay tax • Distributed to the owners of the company

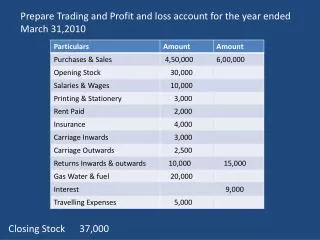

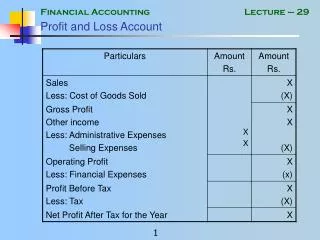

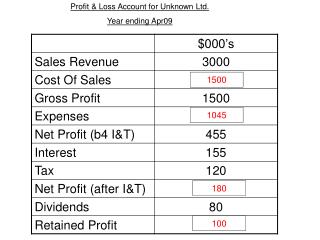

The Profit and Loss Account Businesses measure their profit by compiling a Profit and Loss Account. This is a summary of all business transactions and shows the flow of expenditure and income in a trading period (12 month period). The Trading account shows the revenue earned from selling products (the turnover) and the cost of those sales. Subtracting one from the other gives Gross Profit. Profit and Loss account for Frying Tonite

Turnover/Sales Revenue/Income The turnover or sales revenue figure shows the income from selling goods or services for the specified year. The turnover figure may have to be adjusted for a number of reasons: Businesses must exclude indirect taxes such as VAT. VAT is added to the sale price of goods, it is paid by the consumer to businesses which then hand it to the government Sale of goods which are returned because they are faulty or unwanted, this must be removed from the turnover figure Errors that occur in Invoices – an error which overstates the value of sale will result in adjustment in the turnover (credit notes sent to accommodate the overcharge Customers who have bought goods on credit is unable to pay for them. The turnover figure is usually left unchanged. However businesses do record the value of an unpaid sale as a business expense in the profit and loss.

Cost of Sales Purchases - This refers to all costs of production. It will include direct costs such as raw materials. The opening stock - stock that the business has at the beginning of the year. Closing stock ( stock that is left over at the end of the year) will need to be taken away from the total of Purchases and opening stock. Gross Profit Gross profit is an indicator of how well a firm is making and selling its products. Gross profit on its own does not assist in judging the firms level of efficiency. The important point is that you understand how well the firm is at managing its cost of sales and how to calculate Gross Profit.

Expenses Expenses are the indirect costs that the business incurs. They are costs directly linked to producing goods or services that the firm sells. Total expenses are taken from Gross Profit to find the Net Profit. Net Profit Is an indicator of how efficient the firm is overall as it includes the firms revenues and expenses. However Net Profit on its own does not judge the level of efficiency. Similarly to Gross Profit it is important that you recognise how efficient the firm is at managing its costs and how to calculate the Net Profit.

Uses of Profit and Loss Accounts • Business owners are keen to see how much profit they have made at the end of the trading year. The size of the profit may be a guide to the performance of the business. • A comparison is also possible because a profit and loss account will show the previous year’s figures. It is possible to calculate the gross profit margin and the net profit margin from the profit and loss account. • The ratio of gross profit to sales turnover is known as the Gross Profit Margin: Gross Profit x 100 Turnover • A rise in the gross profit margin may be because turnover has increased relative to cost of sales • A fall may be because costs of sales have risen relative to turnover.

Uses of Profit and Loss Accounts • Gross profit does not take into account the general overheads of the business. So a business may be more interested in the ratio of the t profit to turnover or the Net Profit Margin. This can be calculated by, Net Profit x 100 Turnover • To see how well a business has controlled its overheads. If the gross profit is far larger than the net profit this would suggest that the company’s overheads are quite high. • To help measure its growth. A guide to a businesses growth may be the value of its turnover compared with the previous year’s. • The earnings per share is also shown on the profit and loss account for limited companies. This shows shareholders how much each share has earned over the year. However this is not necessarily the amount of money which they receive from the company. This is the dividends per share.

Limitations of Profit and Loss Accounts • Business accounts cannot be used to show what is going to happen in the future. The Profit and Loss account uses historical information. The account shows what has happened in the past. However it may be possible to identify future trends by looking at the accounts for a longer period of time say 4-5 years . • Stakeholders who are interested in the accounts must be aware that it is possible to disguise or manipulate financial information in the accounts.

The Balance Sheet The balance sheet is a picture of the financial position of a business at a particular point in time. The balance sheet contains information about the assets, the liabilities and the capital of the business

Sections within the Balance Sheet • ASSETS – are the resources that a business owns and uses. They are divided into Fixed and Current. Fixed assets such as machinery are used again and again over a period of time. Current assets are used up in production such as stock and raw materials. • LIABILITIES – are the debts of the business,, i.e. what it owes to other businesses, individuals and institutions. Liabilities are a sources of funds for a business. They might be short term, such as an overdraft, or long term such as a mortgage or bank loan. • CAPITAL– is the money introduced by the owners of the business, for example when they buy shares. Frying Tonite Balance Sheet

In all balance sheets the value of assets will equal the value of liabilities and capital. • Any increase in total assets must be funded by an equal increase in capital or liabilities, i.e a business wanting to buy extra machinery (assets) may need a bank loan (a liability). Alternatively a reduction in credit from suppliers (a liability) may mean a reduction in stocks that can be bought (an asset) So, Assets = capital + liabilities

Presenting the Balance Sheet Balance sheets are presented in a vertical format , one advantage of presenting the sheet in this format is that it is easy to see the amount of working capital (current assets – current liabilities) that a business has. This will show if the business is able to pay its day to day bills. The net assets (Total assets – current liabilities – long term liabilities) of the business are also clearly shown.

Uses of Balance Sheets • Provides a summary of and valuation of all business assets, capital and liabilities – this is a legal requirement laid down by law and by the accounting bodies. • Be used to analyse the asset structure of a business. It can show the money raised by the business has been spent on different types of asset. • Be used to analyse the capital structure of a business. A business can raise funds from many different sources such as shareholders’ capital, retained profit and long term and short term sources (i.e. loans, investors). • Looking at the value of the working capital (current assets (fixed +current) ) can indicate whether a firm is able to pay its everyday expenses or is likely to have problems. • Is a guide to a firm’s value.

Limitations of the Balance Sheet • The value of many assets listed in the balance sheet may not reflect the amount of money the business would receive if it were sold, i.e. fixed assets are listed at cost less depreciation, however depreciation allowance is estimated by accountants. • Many balance sheets do not include intangible assets such as goodwill, brand names, and skills of workforce may be excluded because they are difficult to value or could change suddenly. If such assets are excluded the value of the business may be understated. • A balance sheet is a static statement. Many of the value for assets, capital, and liabilities are listed in the statement are only valid for the day the balance sheet was published. After another day’s trading many of the figures will have changed. • Many argues that the balance sheet lacks detail as they only include totals and are not broken down further.