Download

1 / 11

120 likes | 215 Views

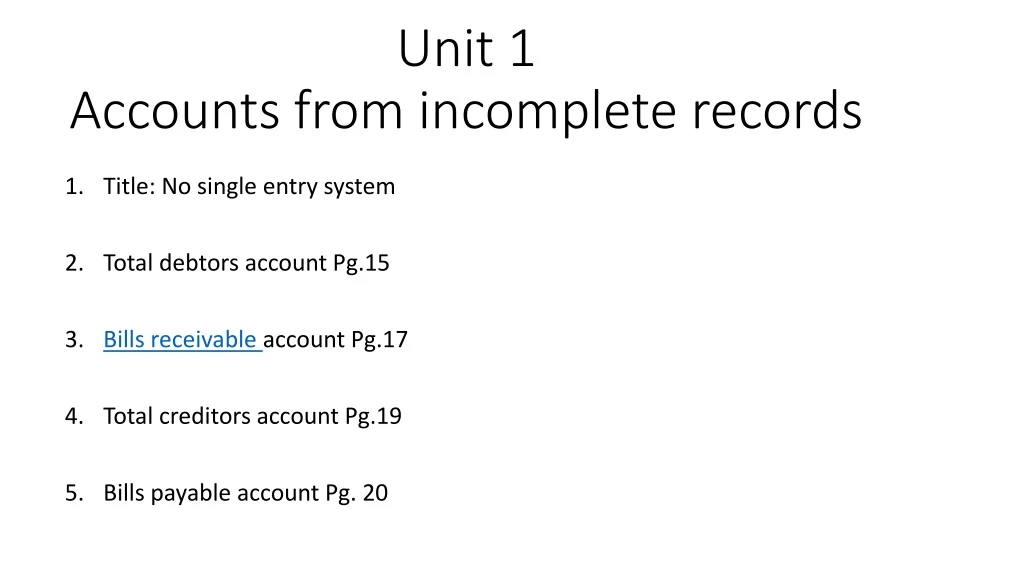

Unit 1 Accounts from incomplete records. Title: No single entry system Total debtors account Pg.15 Bills receivable account Pg.17 Total creditors account Pg.19 Bills payable account Pg. 20. Unit - 2 Not-for-Profit organisation. NPO registered under the Indian Companies Act is excluded

E N D

Unit 1 Accounts from incomplete records Title: No single entry system Total debtors account Pg.15 Bills receivable account Pg.17 Total creditors account Pg.19 Bills payable account Pg. 20

Unit - 2 Not-for-Profit organisation NPO registered under the Indian Companies Act is excluded Items peculiar to NPO Treated as revenue or capital receipt

Unit - 3 Accounts of partnership firms - Fundamentals Provisions of Partnership Act, 1932 Interest on capital Interest on drawings Salary and commission to partners Interest on loan

Unit - 4 Goodwill in partnership accounts Self-generated goodwill Acquired goodwill Interest on drawings Profit after adjustment

Unit – 5Admission of a partner • Sacrificing ratio and new profit sharing ratio • Entry for adjustment for goodwill • Memorandum revaluation A/c

Unit -6Retirement and death of a partner • Current year’s profit upto the date of retirement • Profit and loss suspense account • Settlement of account due to the retiring partner / deceased partner • Life policy

Unit – 7Company Accounts • Minimum subscription – as specified in the prospectus • Application money – Co. Act : Not less than 5% of the nominal value of the share or as specified by SEBI – SEBI : Not less than 25% of the issued price • Call money – Table F: Not more than 25% of the face value of the share

Preference shares : Not dealt with • Issue of shares at discount : Not dealt with

Unit – 8Financial Statement Analysis • Schedule III of the Companies Act, 2013 • PART II - STATEMENT OF PROFIT AND LOSS • PART I - BALANCE SHEET

Comparative statement • Common-size statement • Trend analysis

Unit – 9 Ratio Analysis • Terms used as per Companies Act, 2013 • Revenue from operations = Sales (net) • Cost of revenue from operations = Cost of goods sold