Download

1 / 19

190 likes | 248 Views

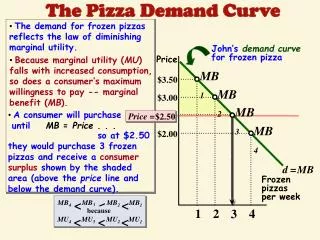

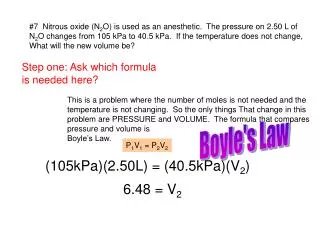

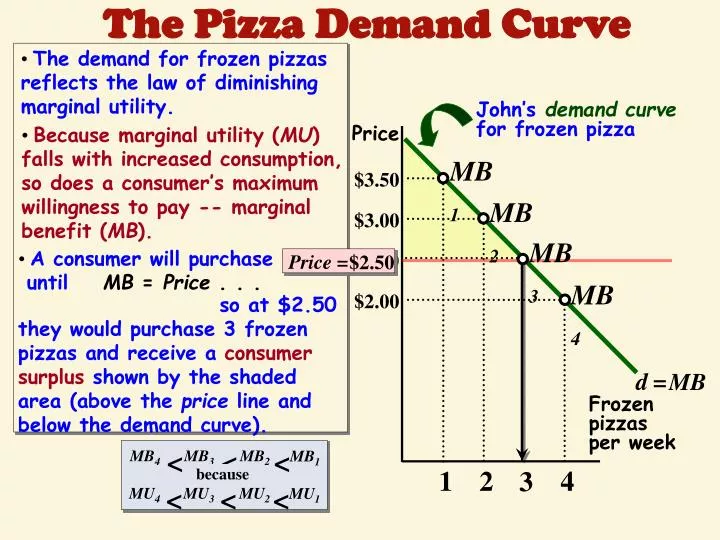

John’s demand curve for frozen pizza. MB 1. MB 2. MB 3. Price =. $2.50. MB 4. d. =. MB. <. <. <. MB 4. MB 3. MB 2. MB 1. because. <. <. <. MU 4. MU 3. MU 2. MU 1. The Pizza Demand Curve. The demand for frozen pizzas reflects the law of diminishing marginal utility.

E N D

John’sdemand curvefor frozen pizza MB1 MB2 MB3 Price = $2.50 MB4 d = MB < < < MB4 MB3 MB2 MB1 because < < < MU4 MU3 MU2 MU1 The Pizza Demand Curve • The demand for frozen pizzas reflects the law of diminishing marginal utility. • Because marginal utility (MU) falls with increased consumption, so does a consumer’s maximum willingness to pay -- marginal benefit (MB). Price $3.50 $3.00 • A consumer will purchase • untilMB = Price . . . $2.50 $2.00 so at $2.50 they would purchase 3 frozen pizzas and receive a consumer surplus shown by the shaded area (above the price line and below the demand curve). Frozen pizzasper week 1 2 4 3

Consumer Surplus The total difference between what a consumer is willing to pay and how much they actually have to pay. Producer Surplus The total difference between what a supplier is willing to provide a good or service and how much they actually get for it.

Producer and Consumer Surplus P Consumer surplus = area of red triangle = ½($5)(5) = $12.5 $10 9 8 7 6 5 4 3 2 1 S Producer surplus = area of green triangle = ½($5)(5) = $12.5 CS PS The combination of producer and consumer surplus is maximized at market equilibrium D Q 0 1 2 3 4 5 6 7 8 8-3

Consumer Surplus • Price Quantity • 1 • 2 • 3 • 4 • 5 • If the selling price is 3, the consumer surplus for the 1st item is 5-3=2, plus 4-3=1 for the 2nd and 3-3=0 for the 3rd, or 3

The Burden of a Tax Tax Incidence • Who pays a tax is called the incidence. Buyer Seller

Splus tax $1000 tax Impact of a Tax Imposed on Sellers Price • If in the used car market a price of $7,000 would bring the quantity of used cars demanded into balance with the quantity supplied. S • When a $1,000 tax is imposed on sellers of used cars, the supply curve shifts vertically by the amount of the tax. $7,400 $7,000 • The new price for used cars is $7,400 … sellers netting $6,400 ($7,400 - $1000 tax). $6,400 D • Consumers end up paying $7,400 instead of $7,000 and bear $400 of the tax burden. • Sellers end up receiving $6,400 (after taxes) instead of $7000 and bear $600 of the tax burden. # of used carsper month(in thousands) 500 750

$1000 tax Dminus tax Impact of a Tax Imposed on Buyers Price • In the same used car market: • When a $1,000 tax is imposed on buyers of used cars, the demand curve shifts vertically by the amount of the tax. S $7,400 $7,000 • The new price for used cars is $6,400 … buyers then pay taxes of $1000 making the total $7,400. $6,400 • Consumers end up paying $7,400 (after taxes) instead of $7,000 and bear $400 of the tax burden. D • Sellers end up receiving $6,400 instead of $7000 and bear $600 of the tax burden. # of used carsper month(in thousands) 500 750

The actual burden of a tax depends on the elasticity of supply and demand. Elasticity and Incidence of a Tax • As supply becomes more inelastic, then more of the burden will fall on sellers. • As demand becomes more inelastic, then more of the burden will fall on buyers. ED ES ED + ES ED + ES

S plus tax S plus tax Tax Burden and Elasticity • Consider the market for Gasolineand Luxury Boatsindividually. Price Gasolinemarket $1.65 • We begin in equilibrium. S $1.60 • If we impose a $.20 tax on gasoline suppliers, the supply curve moves vertically the amount of the tax. Price goes up $.15 and output falls by 6 million gallons per week. $1.55 $1.50 $1.45 D Quantity(millions of gallons) • If we impose a $25K tax on Luxury Boat suppliers, the supply curve moves vertically the amount of the tax. Price goes up by $5K and output falls by 5 thousand units. 194 200 Price(thousand $) Luxury boatmarket S 110 • In the gasmarket, the demand isrelatively more inelasticthan its supply; hence, buyers bear a larger share of the burden of the tax. 100 90 D • In the luxury boatsmarket, thesupply curve is relatively more inelasticthan its demand; hence, sellers bear a larger share of the tax burden. 80 Quantity(thousands of boats) 5 10 15 20

Government Intervention as Implicit Taxation • Government intervention in the form of price controls can be viewed as a combination tax and subsidy

An effective price ceiling is a government set price below the market equilibrium price • It acts as an implicit tax on producers and an implicit subsidy to consumers that causes a welfare loss identical to the loss from taxation P A price ceiling transfers surplus from producers to consumers, generates deadweight loss, and reduces equilibrium quantity S P0 P1 Price ceiling Shortage D Q Q1 Q0

An effective price floor is a government set price above the market equilibrium • It acts as a tax on consumers and a subsidy for producers that transfers consumer surplus to producers P S Surplus P1 Price floor P0 A price floor transfers surplus from consumers to producers, generates deadweight loss, and reduces equilibrium quantity D Q Q1 Q0

The Difference Between Taxes and Price Controls • Price ceilings create shortages and taxes do not • Taxes leave people free to choose how much to supply and consume as long as they pay the tax • Shortages may also create black markets

Rent Seeking, Politics, and Elasticities • The possibility of transferring surplus from one set of individuals to another causes people to spend time and resources on doing so. • Lobbying for price controls, which transfer surplus from one group to another, is an example of rent-seeking behavior • Individuals spend money and use resources to lobby governments to institute policies that increase their own surplus • Public choice economists argue that when all rent seeking and tax consequences are netted out, there is often not a net gain to the public

Inelastic Demand and Incentives to Restrict Supply Revenue gained P When demand is relatively inelastic, suppliers have incentive to restrict quantity to increase total revenue S1 S0 P1 C P0 Revenue lost A B D Q Q1 Q0

Inelastic Supplies and Incentives to Restrict Prices • When supply is inelastic, consumers have incentives to restrict prices • When supply is inelastic and demand increases, prices increase causing consumers to lobby for price controls • Rent control in New York City is an example

Application: Price Floors and Elasticity The surplus created by a price floor is larger if demand and supply are elastic P P S Surplus Surplus S Price floor P1 P1 P0 P0 D D Q Q Q1 Q0 Q1 Q0

Long-Run and Short-Run Effects on Price Control P Higher long-run elasticity of supply results in smaller price increases when demand increases Sshort-run PSR Slong-run PLR P0 D1 D0 Q Q0 QSR QLR