Download

1 / 11

160 likes | 410 Views

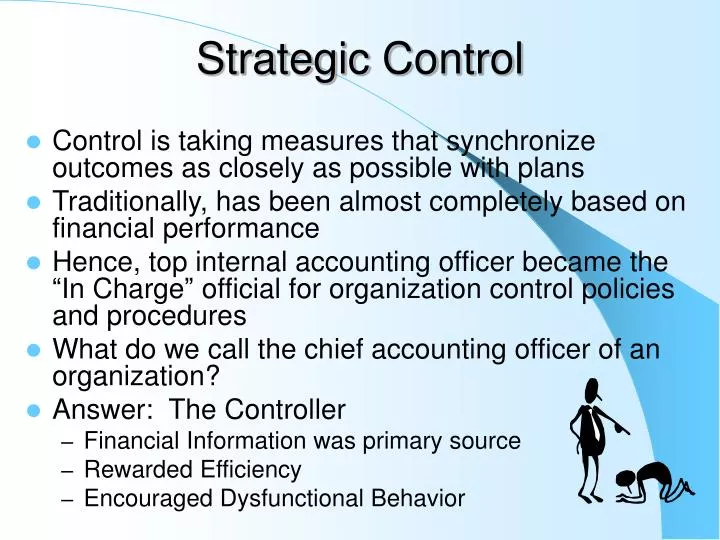

Strategic Control. Control is taking measures that synchronize outcomes as closely as possible with plans Traditionally, has been almost completely based on financial performance

E N D

Strategic Control • Control is taking measures that synchronize outcomes as closely as possible with plans • Traditionally, has been almost completely based on financial performance • Hence, top internal accounting officer became the “In Charge” official for organization control policies and procedures • What do we call the chief accounting officer of an organization? • Answer: The Controller • Financial Information was primary source • Rewarded Efficiency • Encouraged Dysfunctional Behavior

Strategic Control • Strategic Control Methods • Integrates Quantitative & Qualitative Measures • Uses Financial and Non-financial information • Customer (External) focus • Rewards based upon relative contributions to organization success • Encourages desired organizational behavior Implementing Planning Control Cycle Measuring Adjusting

1990’s thru 21st Century Traditional Strategic Control and Control Systems Should motivate people toward desired organizational behavior rather than promote dysfunctional behavior Customer Satisfaction New Product Development Rates Outcomes Quantitative & Qualitative Performance Meeting Budget Production Efficiency Inputs Quantitative Performance(Mostly Financial) What is Measured?

1990’s thru 21st Century Traditional Who is evaluated? Individuals Functions Responsibility Centers Individuals Teams (Groups) Cross-Functional People

1990’s thru 21st Century Traditional Basis of Rewards control Systems Efficiency Profits ROI Quality Innovation Creativity Overall Company Performance

1990’s thru 21st Century Traditional Focus of Contemporary Control Systems Internal Macro Environment Industry Environment Internal

Capacity Management Capacity is the potential or capability, of a set of resources to do work of some type to create value for the customer. Importance of capacity management (control) of organizations Huge initial outlays Sunk costs Inflexible Long-run costs Mostly Fixed Costs Goal of capacity management is to manage fixed costs (plant assets) in a manner that spreads costs over the largest possible volume A very difficult area of management because it involves long-range planning

Strategic Control of Capacity • Must have right amount of capacity to produce to customer demands *If there is excess capacity fixed costs must be spread over fewer units thereby making the units cost more *If there is insufficient capacity the company must incur additional costs to generate more capacity

Company A Company B A Capacity Management Example Company A and Company B each manufacture one product that is very similar in nature. Company A recently invested in modern machinery (new technology) that reduces its manufacturing labor cost. Company B continues to be labor intensive using its older machinery. Accordingly, Company A has much more fixed factory overhead annually than Company B ($ 1,500,000 compared to $ 600,000). The respective selling price and variable costs per unit are as follows: Selling Price $20.00 $20.00 Direct Mat. $2.00 $2.00 Direct Labor $1.00 $6.00 Var. Overhead $1.00 $1.00 Required: Compute the gross margins on the product of each company. Assume an annual volume of production and sales of 100,000 units; then 200,000 units.

Solution: Fixed Cost/Unit 15.00 6.00 (100,000 Units) Company A Company B Cost: Variable Costs/Unit $4.00 $9.00 Total Cost/Unit $19.00 $15.00 Selling Price $20.00 $20.00 Total Gross Margin $100,000 $500,000 (200,000 Units) The only Change is Fixed costs per unit $7.50 $3.00 Total Gross Margin $1,700,000 $1,600,000

Cost-Volume-Profit Analysis Contribution Margin Profit Area Revenue Line Break Even Point $ Fixed Costs & Total Costs Line Loss Area Variable Cost Line Activity Level