Download

1 / 10

130 likes | 1.24k Views

Adjusting Entries: Matching Accounting & Timing Certain end-of-period adjustments must be made when you close your books. Adjusting entries are made at the end of an accounting period to account for items that don't get recorded in your daily transactions.

E N D

Adjusting Entries:Matching Accounting & Timing • Certain end-of-period adjustments must be made when you close your books. • Adjusting entries are made at the end of an accounting period to account for items that don't get recorded in your daily transactions. • In a traditional accounting system, adjusting entries are made in a general journal. • Some adjusting entries are straightforward. • Others require judgment and some accounting knowledge.

Adjusting Entries:Matching Accounting & Timing • Some adjusting entries must be made because there is a journal entry that “drives” it. • Some adjusting entries must be made because of the passage of time: there is no “driver”. • Adjusting entries are used to insure that revenues are reported when earned and expenses are reported when incurred.

Adjusting Entries:Matching Accounting & Timing • Adjustments are necessary because applicable things have occurred during the period but have not been recorded. • Any adjusting entry always increases either a revenue or an expense (not both in the same entry). • Either a revenue will be receiving a credit or an expense will be receiving a debit. • The only question for the journal entry then becomes: What gets the debit (if the adjustment is to increase revenue) or what gets the credit (if the adjustment is to increase an expense)?

Adjusting Entries:Matching Accounting & Timing • Adjusting entries to increase revenues are required either because someone paid you before you did any work (unearned revenue) or you did work before you billed or were paid for it (accounts or interest receivable). • This tells you your debit entry if the adjustment is to increase revenue: debit unearned revenue or debit accounts (interest, etc.) receivable; credit revenue (of some type). • Remember: a prepaid expense is an asset, NOT an expense. • Remember: an unearned revenue is a liability, NOT a revenue.

Adjusting Entries:Matching Accounting & Timing • Adjusting entries to increase expenses are required either because you already paid for them before using them (prepaid expenses such as insurance, rent, supplies) or you used them before being billed or paying for them (accrued wages payable, accrued interest payable, etc.). • This tells you your credit entry if the adjustment is to increase an expense. • Debit the expense; credit prepaid insurance, supplies or wages payable, etc.

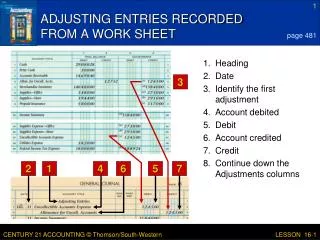

Closing Entries: Out With The Old, In With The New • After financial statements are prepared, you are ready to get your books ready for the next accounting period by clearing out the income and expense accounts in the general ledger and transferring the net income (or loss) to your owner's equity account. • Closing entries are needed to clear out your revenue and expense accounts as you start the beginning of a new accounting period.

Closing Entries: Out With The Old, In With The New • Note the distinction between adjusting entries and closing entries. • Adjusting entries are required to update certain accounts in your general ledger at the end of an accounting period. • Adjusting entries must be done before you can prepare your financial statements and income tax return. • Closing entries are done after the financial statement is constructed.

Closing Entries: Out With The Old, In With The New • Preparing your closing entries is a very simple, mechanical process. Follow these steps: • Close the revenue accounts. Prepare one journal entry that debits all the revenue accounts. (These accounts will have a credit balance in the general ledger prior to the closing entry.) Credit an account called "income summary" for the total. • Close the expense accounts. Prepare one journal entry that credits all the expense accounts. (These accounts will have a debit balance in the general ledger prior to the closing entry.) Debit the income summary account for the total.

Closing Entries: Out With The Old, In With The New • Transfer the income summary balance to a capital account. Prepare a journal entry that clears out the income summary account. This entry effectively transfers the net income (or loss) of the business to the owner's equity account. • Close the dividend account. If your business is a sole proprietorship or partnership, close the dividend accounts (if any) by preparing a journal entry that credits the dividend account and debits the owner's equity account.

Closing Entries: Out With The Old, In With The New • After all closing entries are made, post the entry totals to the general ledger. • All revenue and expense accounts should have a zero balance.