Download

1 / 10

110 likes | 513 Views

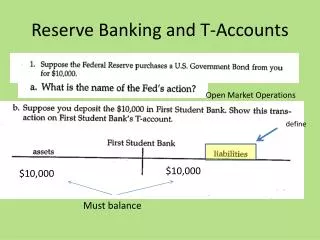

Reserve Banking Bank reserves - assets held by a bank to fulfill its deposit obligations, or, deposits that banks have received but have not loaned out. 100% reserve banking vs. fractional reserve banking

E N D

Reserve Banking • Bank reserves - assets held by a bank to fulfill its deposit obligations, or, deposits that banks have received but have not loaned out. • 100% reserve banking vs. fractional reserve banking • Fractional reserve banking - a banking system in which banks hold only a fraction of deposits as reserves. • Bank reserves are only a fraction of total deposits. • Reserve ratio = bank reserves / total deposits • Profits are made from loaning out deposits. However a bank will close its doors if it cannot meet the demands of its depositors. So the bank must balance the demands for depositors with the drive for profit.

Creating Money • Numerical example. • Joe deposits $1500. • Mo requests loan of $1000, which is deposited in Mo’s checking account. • Bank now has $1000 in loans, and $2500 in deposits. • When a bank makes a loan, the money supply is increased. Why? The debtor now has more money and no one else has any less.

The Money Multiplier • The Money Multiplier - the number of deposit (loan) dollars that the banking system can create from $1 of excess reserves. • Example: • $100 is deposited in a Bank A, with 10% reserves • Loan is made for $90, which finds its way to Bank B • Bank B now has $81 in excess reserves which it loans out • Bank C acquires a deposit of $81, which translates into excess reserves of $73.90. Etc. • Money multiplier = 1 / required reserve ratio • If the required reserve ratio = 10%; So, the money multiplier is 10 • Example • Banking system has $10 million in total deposits. • So, $1 million must be in reserve and $9 million is excess reserves. • Potential deposit creation = excess reserves * money multiplier • Bank can create 90 million in potential deposits.

Constraints on Money Creation • Constraints on deposit creation • deposits: people have to be willing to substitute checks for cash. • borrowers: people have to be willing to borrow money. • regulation: the federal reserves places limits on bank lending.

Measures of Money TODAY Components of M2 Components of M1 Money market mutual funds (15%) Currency (54%) Savings deposits (51%) M1 (19%) M1 (28%) Checking accounts (45%) Small-denomination time deposits (15%) Traveler’s checks (1%)

State Bank Notes • When a person took out a loan from a bank, the bank paid out state bank notes. These notes circulated as money. Hence states, who according to the Constitution could not issue paper currency, chartered banks that were able to serve this function.

Gresham’s Law • “bad money drives good money out of circulation” • http://eh.net/encyclopedia/article/selgin.gresham.law • The expression "Gresham's Law" dates back only to 1858, when British economist Henry Dunning Macleod (1858, p. 476-8) decided to name the tendency for bad money to drive good money out of circulation after Sir Thomas Gresham (1519-1579). • Gresham's Law can hold… where both good and bad coins enjoy similar legal-tender status and where non-trivial sanctions can be applied to persons who insist upon discriminating against bad coin and in favor of good coin. In such cases all coins must be accepted…Buyers, knowing that sellers must accept either good and bad coins at their official face value, offer inferior coins, while hoarding, exporting, or reducing better ones; sellers, anticipating buyers' dominant strategy, price their wares accordingly (Selgin 1996).

Regulation of State Banks: Suffolk System • Suffolk System (1820s) • People hoard the notes of the Suffolk Bank of Boston and spend country bank notes. (Gresham’s Law) • Suffolk bank began presenting the notes of country banks for redemption in specie. To prevent this, country banks agree to hold reserves at the Suffolk bank against their own note issue. • What is the purpose of the Suffolk system?

New York Regulation • Double liability - bank stock owners were liable for twice the face value of bank stocks. This was imposed by New York in 1827 to encourage bank conservatism. • New York Safety Fund (1829-1839) - banks are required to pay 3% of capital into insurance fund. The bank panic of 1837 caused so many banks to close that the fund was completely drained. This in turn caused the New York tax payers to suffer since the state of New York had guaranteed the bank deposits.

Chartering of State Banks • Only banks were chartered by the states, federal government did not charter or regulate existing banks. • Advent of free banking era: 712 state banks each with its own currency and discount rate. • Charter’s originally specified: • Interest rate (loans and deposits) • Reserve ratio: reserve-deposit ratio (how much of deposits are loaned) • Capital ratio