Download

1 / 31

310 likes | 440 Views

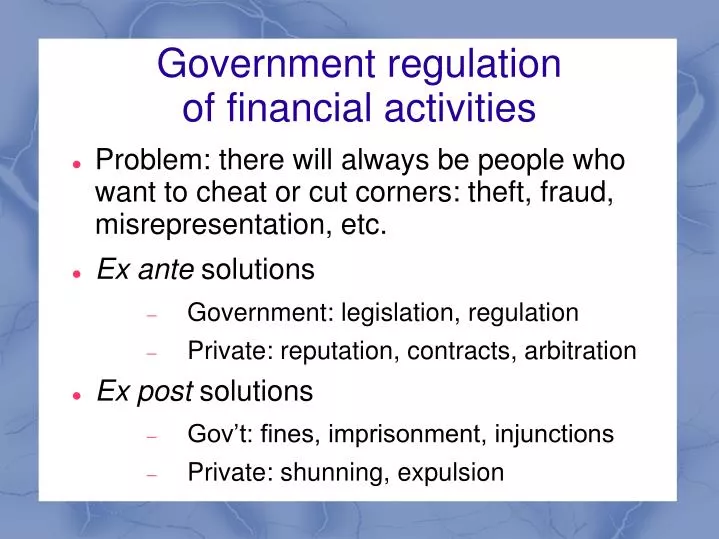

Government regulation of financial activities. Problem: there will always be people who want to cheat or cut corners: theft, fraud, misrepresentation, etc. Ex ante solutions Government: legislation, regulation Private: reputation, contracts, arbitration Ex post solutions

E N D

Government regulationof financial activities Problem: there will always be people who want to cheat or cut corners: theft, fraud, misrepresentation, etc. Ex ante solutions Government: legislation, regulation Private: reputation, contracts, arbitration Ex post solutions Gov’t: fines, imprisonment, injunctions Private: shunning, expulsion

Financial services Broad classes of financial services Intermediation Brokerage Investment banking Many firms offer some or all of these services

Financial intermediation Match savers with borrowers (businesses and households) Primary example: deposit banking Accept deposits from savers Loan money to businesses and households Interest rate spread is the primary income source

Deposit banking Commercial banks are the primary providers of deposit banking Also Savings and Loan (emphasize mortgage lending) And Credit Unions (non-profit) Deposit forms Demand deposits (checking accounts) Savings accounts Currently pay essentially zero interest

Deposit banking Loan forms Households Home mortgages Automobile loans Personal loans Businesses General purpose loans Factoring – purchase of accounts receivable

Deposit banking Problems that can arise when loans go bad insolvency: liabilities exceed assets a serious problem that can lead to closure illiquidity: not enough cash to meet liabilities usually easy to remedy by borrowing from other banks or from the Fed

Deposit banking Deposit banks are inherently illiquid Only a small fraction of deposit liabilities are backed by reserves (currency and accounts at the Fed) Most deposits can be withdrawn on demand Most loans cannot be called on short notice Possibility of a “bank run” if too many depositors want their money simultaneously

Deposit Insurance Almost all banks carry deposit insurance Provided by the Federal Deposit Insurance Corporation (FDIC) Banks pay insurance premium based on risk – a small fraction of insured deposits FDIC typically arranges mergers of failed banks FDIC has failed to maintain reserves equal to 1.15% of insured deposits

Bank Subsidies and Protections Deposit insurance may be under-priced Potential competitors are barred from the marketplace (e.g., WalMart) Banks were bailed out during the 2008 financial crisis. “Too big to fail” Implicit bailout protection encourages risky behavior (“moral hazard”)

Bank Regulation Deposit banks are regulated by a confusing array of Federal and State agencies Federal Reserve FDIC Comptroller of the Currency State bank regulatory agencies Main requirements 10% reserves on deposit liabilities Minimum levels of shareholder capital

FDIC insurance engendersmoral hazard Encourages bank managers to take more risk Discourages depositors from paying attention to how banks manage their deposits Leads people to believe that deposit risk has been eliminated when in fact it has been socialized

FDIC vs. Private Insurance FDIC is governed by politics, not the marketplace Coverage limits set by Congress Premium rates limited by statutes Private insurance companies manage moral hazard with risk assessment Private insurance companies face competition and must engage in price discovery

Brokerage Brokers match buyers with sellers Real estate brokers Stock brokers Insurance brokers Marriage brokers (?) Income mostly from commissions Real estate: about 6% Stock brokers: very low commissions

Stock brokerage Firms that traditionally or primarily engage in brokerage typically do other things as well: Bank subsidiaries (e.g., Schwab Bank) Hold securities for their own account, thereby acting as dealers

Insurance for brokerage customers Provided by Securities Investor Protection Corporation (SIPC) Created by legislation but operates as a private, non-profit, self-funded corporation Customer assets must be segregated Provides insurance against certain kinds of malfeasance such as misappropriation of funds or unauthorized trading Does not insure against market declines

Problems and solutions Voluntary solutions Reputation Arbitration Industry associations New York Diamond Dealers, 47th St. NYC All Hasidic Jews Disputes settled by private arbitration Anyone failing to abide by arbitrators’ decisions is subject to shunning and adverse publicity

The “Public Choice” approach to analysis of government Applies economic tools to the analysis of politicians, bureaucrats and voters Contrasts with the “public interest” viewpoint which assumes selfless dedication to the public welfare Politicians motivated by re-election Bureaucrats want to keep their jobs Voters exhibit rational ignorance

Regulatory capture Regulated industries have huge incentives to influence the agencies that regulate them The general public has little or no knowledge of the regulation Industry people know their business better than regulators Regulators with the best of intentions may find their mission subtly shifted

Limited resources; revolving door Regulator agencies have limited staff and budget Often cannot possibly exercise detailed supervision over many large firms Regulatory staff often work a few years in a regulatory agency then take jobs in one of the industries they regulated

Turf wars The domains of regulatory agencies often overlap, leading to inter-agency “turf wars.” Example: who should regulate futures contracts on stocks? CFTC said all futures were in its domain SEC said anything involving stocks was in its domain Promotes a “race to the bottom” as in the case of the late Office of Thrift Supervision

False confidence Government regulation can lead the public to believe they shouldn’t worry Example: some Madoff investors told themselves securities markets are heavily regulated – nothing could go wrong Hummel’s law of failure: Perceived market failure always leads to calls for more government Perceived government failure always leads to calls for more government

Sarbanes-Oxley The collapse of Enron Corp. was a major scandal in 2001. It concealed off-balance-sheet operations Ken Lay died in prison Jeffrey Skilling still in prison Enron’s auditor, the venerable Arthur Anderson, was disbanded Also MCI, which engaged in fraudulent accounting

Sarbanes-Oxley Sarbanes-Oxley was a regulator reform bill passed in response to Enron & MCI scandals CEOs must personally certify the accuracy of financial information New bureaucracy established to oversee independent auditors Additional disclosures required in financial statements Criminal penalties for some offenses

Sarbanes-Oxley Outcomes May have increased accuracy and thoroughness of financial reports Compliance costs hit small firms harder than larger firms Some foreign firms dropped NYSE listings to avoid Sarbanes-Oxley May have reduced IPOs

Dodd-Frank Passed in response to the financial crisis of 2008 Bailouts of large financial institutions Bailouts of GM and Chrysler Stock market crash (since recovered) Massive deficits Official titles always reflect hoped-for results: “The Wall Street Reform and Consumer Protection Act”

Dodd-Frank No one person understands its 2300 pages. Contains many references to other laws. Despite its length, it left a great deal of rule-writing to bureaucracies. Although it passed in 2010, many of the rules are incomplete. Uncertainty hinders business recovery.

Dodd-Frank and the Volcker Rule Prohibits banks from buying and selling securities for their own account, supposedly to lessen the prospect of future bailouts. Four federal agencies share the responsibility for writing rules that implement the Volker rule. Turf wars! Interested parties have been hard at work trying to influence the rules

Dodd-Frank and the Volcker Rule Proprietary trading turns out not to be so easy to define. So exemptions have been carved out Trading on behalf of customers Hedging Underwriting and market-making. Trading of their own securities

Crony capitalism Adam Smith: business people hate competition and are eager to use government to suppress it Government intrusion into the economy opens the door for businesses to seek advantages Lobbying Campaign contributions Personal friendships

Crony capitalism Laws governing complex economic activities are necessarily vague and incomplete. Interpretation is left to the bureaucracy The door is open to business lobbying The “military-industrial complex” is the granddaddy of them all Close ties among defense contractors, military officials, employees and their dependents

Hummel’s law of failure Perceived market failures always lead to calls for more government Perceived government policies always lead to calls for more government