Download

1 / 101

1.01k likes | 1.17k Views

Meltdown. Economic Crisis and Government Response. I. Causes: Competing Explanations. Trigger: Most agree that housing bubble triggers the crisis, because bubbles encourage risk taking (and use of leverage) and because investment in housing (through mortgages) spread throughout economy.

E N D

Meltdown Economic Crisis and Government Response

I. Causes: Competing Explanations • Trigger: Most agree that housing bubble triggers the crisis, because bubbles encourage risk taking (and use of leverage) and because investment in housing (through mortgages) spread throughout economy. Video overview

B. What caused the bubble? • Easy Money (consensus): Very low interest rates encourage bubbles. Why were interest rates low?

2. Government Housing Incentives (Controversial) a. Home mortgage interest deduction • Argument: Subsidizes larger mortgages • Objection: Has existed since creation of income tax (all interest deductible until 1986)

b. Housing Loan Agencies • Argument: Government encourages risky lending • FHA: Insures mortgages (reduces risk to lenders) • Fannie Mae and Freddie Mac: Buy mortgages allows banks to clear balance sheets and issue new loans (amplifies credit available for mortgages) • Objection: FHA/Fannie Mae established during Depression to increase mortgage lending, long before current crisis

c. HUD regulations of housing agencies • Argument: In 1996 HUD gave Fannie/Freddie a target -- 42% of mortgage financing had to go to borrowers with income below the median in their area increased to 50% in 2000 and 52% in 2005. • Objections • Between 2004 and 2006, Fannie and Freddie went from holding 48 percent of the subprime loans that were sold into the secondary market to holding about 24 percent • Why? Possible reason: Fannie and Freddie were subject to tougher standards than the unregulated players in the private sector

3. Community Reinvestment Act (Controversial) a. Purpose: Passed in 1977 to prevent “redlining” – refusing to issue mortgages or loans in high-crime areas, regardless of credit-worthiness of borrower • Example: Banks might lend to low-income residents of blue neighborhoods (i.e. whites) but refuse a loan for high-income residents of red neighborhoods (i.e. African Americans)

b. Amendments • Original CRA: required use of same lending criteria in all communities – largely self-enforced • 1989: Added public data on CRA compliance created by federal agencies • 1995: Compliance to be measured by outcomes (lending in communities) rather than process (procedures for evaluating loans) • 1994 and 1999: Conditioned bank expansions & mergers on CRA compliance • 2005 and 2007: CRA weakened for large banks (allowed to count lending in place of banking services or investment in communities)

c. Effects of CRA/Amendments • Argument: CRA requires banks to make risky loans, so helped fuel subprime lending created homeowners out of people who traditionally could not own homes

2008 1995: CRA Strengthened 1977: CRA Established

ii. Objections to Blaming CRA • CRA preceded crisis by decades • CRA applies only to banks and thrifts that are federally insured – not independent mortgage companies (e.g. Countrywide) which made half of all subprime loans • Non-CRA institutions made subprime loans at more than twice the rate of CRA institutions

4. Irrational Exuberance? (moderate consensus) a. Shiller’s feedback model: • Asset price rise occurs, leading to profits • Profits attract less sophisticated investors • Problem: Investors have incentives to promote “new era” theories of why “this is no bubble” – but investors get their information from each other • People speculate – i.e. pay any price to resell at higher price tomorrow • Any dip in prices doubts about the “new era” theory some investors exit • Exits further price declines further exits until underlying economic value of asset reached • Problem: Price declines extrapolated into future = unduly pessimistic assessment of underlying value Summary: Extrapolation from current trends undue optimism undue pessimism

Example: “Housing-bubble theory full of hot air” – Sept 2003 article • “Ever since the NASDAQ meltdown some folks have been waiting for the next big bad equity story. Since most equity is found in peoples' homes, that's where pundits have been focusing. They face disappointment however as they watch and wait for the "house-price bubble" to burst. It's not going to happen -- there isn't one…. • “Housing supply in the United States is growing slower than housing demand. That means prices will rise… Supply is growing more slowly because it is constrained by local growth control ordinances, increased environmental cost, time requirements for land development… Demand will grow faster because demographic factors like population growth, household formation rates, immigration, employment growth and income growth are all going to push demand forward more rapidly…. there were 11 million immigrants to the United States over the past decade that will create 4 million new home buyers over the next two decades. Recent gains in the economy's rate of productivity mean that income growth will be strong for probably the next decade. When placed in the context of conservative supply growth, this is a recipe for real price increases, not collapse.”

4. Irrational Exuberance? (moderate consensus) a. Shiller’s feedback model: • Asset price rise occurs, leading to profits • Profits attract less sophisticated investors • Problem: Investors have incentives to promote “new era” theories of why “this is no bubble” – but investors get their information from each other • People speculate – i.e. pay any price to resell at higher price tomorrow • Any dip in prices doubts about the “new era” theory some investors exit • Exits further price declines further exits until underlying economic value of asset reached • Problem: Price declines extrapolated into future = unduly pessimistic assessment of underlying value Summary: Extrapolation from current trends undue optimism undue pessimism

b. Who was irrational? • Homebuyers? Took risks to get better homes • Speculators? Took higher risks to get bigger profits • Mortgage Brokers? Would be irrational to refuse to broker risky loans when everyone else does it! No risk for the broker. • Mortgage Lenders? Would be irrational to refuse to make risky loans when everyone else does it! Why? • Creates lower short-term return for shareholders than other companies • Also creates lower yields for depositors • Executive compensation based on short-term returns (i.e. a given year) and often shields executives from risks (golden parachutes)

Who was irrational? (cont) v. Shareholders: Why do they insist on short-term profits? • Popularity of employee stock compensation – options generally vest quickly, giving employees an incentive to focus on short-term gains • Long-term investors require information which is held by companies themselves – who hire their own auditors ( long-term investment strategy may not reduce risk if company has other incentives to focus on short term) vi. Mortgage Backers and Investment Banks: Able to construct MBS to manage risk, passing it on to investors and focusing on short-term profits (the lowest tranch) for similar reasons as banks

Who was irrational? (cont) vii. Investors in MBS: Relied on ratings and insurance to determine risk Hedge funds and other large investors driven by short-term profits for familiar reasons viii. Raters: Paid by investment banks (possible conflict of interest) Not subject to real risk Oligopoly: limited number of players means reputation hits have limited impact (three government-approved ratings agencies until recently – now four) Bond ratings protected by First Amendment – cannot challenge in court Used automated systems (formulas) to rate that were “gamed” by investment banks during the bubble (MBS complexity made/makes accurate valuation difficult)

One hedge fund manager’s story: • “I didn’t understand how they were turning all this garbage into gold” • He brought some of the bond people from (investment banks) Goldman Sachs, Lehman Brothers, and UBS over for a visit. • “We always asked the same question. Where are the rating agencies in all of this? And I’d always get the same reaction. It was a smirk.” • He called Standard & Poor’s and asked what would happen to default rates if real estate prices fell. The man at S&P couldn’t say; its model for home prices had no ability to accept a negative number. • “They were just assuming home prices would keep going up… I cannot f*** believe this is allowed—I must have said that a thousand times in the past two years.” Source: Condé Nast Portfolio.com, Dec 2008

Who was irrational? (cont) ix. Insurers: • Partly relied on ratings, but mainly focused on short-term profits (securities more profitable to insure than individuals shift to booming MBS market) • Use of Credit Default Swaps (CDFs) to hedge risk – no underlying collateral required!

c. Are CDSes irrational? • Invented in 1997 • Type of derivative (value tied to some other security or quantity) • Buyers make payments to sellers but receive payoff if underlying security defaults • Market expands 10x from 2003-2007 • Current value = about $15 trillion of the CDS market tied to MDSes but… • Defaults are rare – about .2% of companies default, so most payments are simple “premiums”

d. Summary: Risk and Rationality • Risk-taking can be quite rational, yet generate catastrophe • Four key features of decision-making in the bubble: • Underestimation of risk: can correct formulas for this, but uncertainty will always remain • Moral hazard (incentives to do the wrong thing): CFOs do not require “insurable interest” allows one to “short” stocks, inducing pessimism and creating default, then benefit from the default. This is why we don’t let people buy fire insurance on homes they don’t own or take out life insurance on their enemies. • Focus on short term returns: Created by…

iv. The Principal-Agent Problem • Principal: Someone who represents others • Agents: Those who are represented • The Problem: • Principals are self-interested but charged with looking out for agent’s interests • Principals have more information than the agents, creating opportunities to profit at expense of agents

Examples: • Managers represent stockholders • Leaders represent citizens • Brokers represent mortgage banks • Executives represent companies • Solving the problem requires tying principal’s interests to those of agents

5. Deregulation (controversial) a. Commodity Futures Modernization Act (2000): Made CDS deregulation explicit.

CDS Deregulation (Cont) • Argument: CDSes allowed businesses to leverage themselves without restraint (no reserves required, CDSes can become the basis of a new CDO in a never-ending cycle) Small number of bad loans = huge losses • Objection: CDSes allow risk to be spread around, which reduces chances of collapse

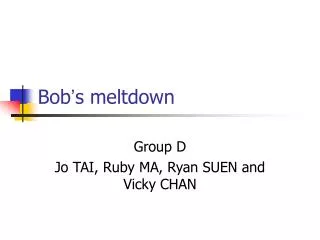

The mortgage-securitization sausage-grinderHow well does Investor 1 on the right understand the risk of Mortgage 1 on the left? Mortgage 1 CDO Investor 1 Securitiza- tion trust Mortgage 2 CDO CDO2 Investor 2 Mortgage 3 CDO Investor 3 Mortgage 4 Investor 4 Collateralized debt obligation (CDO) Securitiza- tion trust Mortgage 5 CDO2 Investor 5 Mortgage 6 Investor 6 Mortgage 7 CDO Investor 7 Securitiza- tion trust Mortgage 8 CDO CDO2 Investor 8 Mortgage 9 CDO Investor 9

CDS Deregulation (Cont) • Argument: CDSes allowed businesses to leverage themselves without restraint (no reserves required, CDSes can become the basis of a new CDO in a never-ending cycle) Small number of bad loans = huge losses

b. Amalgamation of banks and fragmentation of regulation i. Argument: “Too big to fail and too big to regulate” • Amalgamation: 1994 and 1999 laws allowed banks to spread across state lines and into all sectors at once (investment banking, insurance, commercial banking)

Fragmentation • Banks now permitted to choose state or federal regulation, AND • Banks allowed to choose BETWEEN federal regulators – and agency funding is tied to banks’ choice of regulator, AND • Different sectors of banks can be overseen by different regulators, allowing assets to be shifted into least-regulated sectors and preventing any one agency from evaluating the overall soundness of the bank

ii. Objections • Traditional investment banks (those which did not take advantage of the ability to enter other sectors) did worse than other banks (no large ones left). • Deregulation allowed US banks to better compete against foreign banks • Deregulation made banks more profitable, and hence better able to withstand shocks

c. Federal Pre-Emption • Argument: Federal regulatory authority was used to “pre-empt” (render null and void) anti-usury laws of states, allowing expansion of subprime loans (some interest rates as high as 22%!) • Objections: • Impossible to know what states would have done absent federal pre-emption • Pre-emption (Depository Institutions Deregulation and Monetary Control Act) occurred in 1980, decades before the crisis

6. Market failures and the absence of regulation (some controversy) • Securitization: As new derivatives were invented, few people actually understood them inability to price them properly when risks begin to rise • SIVs: Allow banks to move actual loans off balance sheets, then guarantee the loans anyway to sell MBSes – move made purely to avoid regulations on maintaining reserves

6. Market failures and the absence of regulation (some controversy) • Securitization: As new derivatives were invented, few people actually understood them inability to price them properly when risks begin to rise • SIVs: Allow banks to move actual loans off balance sheets, then guarantee the loans anyway to sell MBSes – move made purely to avoid regulations on maintaining reserves

c. Unregulated principals • Brokers: Unregulated and paid by commission – and banks are permitted to pay them higher fees for steering borrowers to more lucrative subprime loans • Executives: Compensation not tied to long-run performance • Corporate governance: Boards are supposed to oversee executives but often fail to do so (insulated from shareholders)

7. Long-term causes (highly speculative) • Low net national savings rate • NS = S – BD • Implication: budget deficits reduce savings. Large deficits normal since 1970s • Why do we care? Investment (spending on new capital equipment) must come from savings or borrowing from abroad

b. Current Account Deficits • How investment is financed when savings are low • Problem: finance occurs through asset sell-off (i.e. mortgages)

iii. Causes of Current Account Deficit • Low national savings rate • Attractiveness of US securitization – draws in foreign capital (which otherwise might have been invested in developing countries) • Economic growth in developing nations – especially China and oil exporters

c. Business Cycles • Is this recession unusual?

d. Income inequality? • Income inequality correlates with asset bubbles. But which causes which? • Perhaps it contributes to the surplus of investment capital since rich people consume less than poor • Perhaps bubbles produce a handful of very, very rich people • Note: Middle-class consumption increased this decade, financed by borrowing (much of it against home values)

8. Exacerbating factor: accounting rules • Old rules: Asset value was based on purchase price (allowed losses to be masked by keeping toxic assets around instead of selling them for a loss) • New rules (1990s): Asset value based on current market value “Mark to market” • Problem: What if market value is unknown because no one has bought or sold this CDO? Suddenly, banks and firms look under-capitalized, with many liabilities and few marketable assets exacerbates credit crunch

II. Consequences and Predictions • Continued Asset Deflation? 1. Home ownership rates still higher than normal